How can life insurance become a powerful financial tool for high-net-worth Canadians? This guide lists strategies for tax efficiency, estate planning, and legacy protection

Life insurance carries several unique features that many high-net-worth families can use to manage and protect their wealth. This makes it an attractive asset for many wealthy Canadians.

In this guide, Wealth Professional discusses the role life insurance plays in helping the country’s affluent grow, manage, and preserve their wealth. We also talked to an industry expert who explained how life insurance for high-net-worth individuals works, with tips on how to find the right coverage.

Do wealthy people need life insurance?

Some high-net-worth Canadians find life insurance an appealing asset because of the tax-free savings and investment opportunities that such policies provide. Life insurance plans can also allow them to keep their wealth in their families.

"Life insurance provides protection, grows wealth, assists in estate planning, and can safeguard businesses, making it crucial for high-net-worth individuals," says Greg Rozdeba, licensed life insurance advisor and CEO of digital insurance brokerage Dundas Life.

"Life insurance isn’t just about protection – it’s an essential wealth management and estate planning tool. For high-net-worth individuals, life insurance protects family assets, covers estate taxes, and ensures wealth transfers seamlessly to future generations.”

Rozdeba adds that life insurance can serve as an effective legal tool for wealthy Canadians.

“Life insurance can shield assets from creditors, preserving family wealth from potential legal challenges,” he explains. “It's also a strategic way to provide liquidity, balancing estates and ensuring heirs receive their fair share without forced asset liquidation.”

Regardless of net worth, there are certain types of individuals who can benefit the most from taking out life insurance. These include:

- breadwinners

- married couples with children

- those who have dependants with special needs

- those who owe co-signed debts, including mortgage and student loans

- parties to a divorce

- business owners and their partners

Contrary to popular belief, life insurance doesn’t only suit high-net-worth families. This article busts the common misconceptions about life insurance policies.

How high-net-worth Canadians use life insurance to grow and protect wealth

As a person’s wealth grows, so does their need for lifestyle, business, and estate planning. This is where life insurance comes into play. If used well, this type of financial instrument can play an important role in helping rich individuals maximize and protect their wealth.

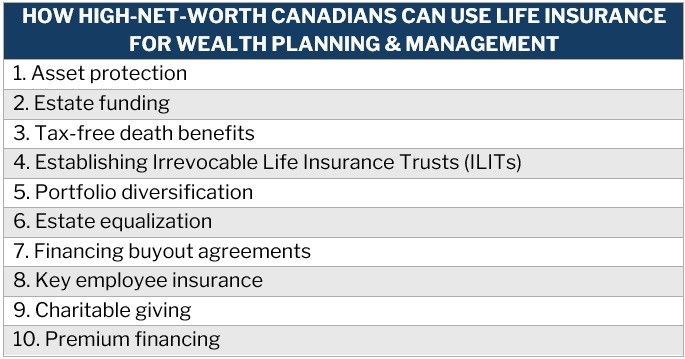

Here are some of the ways high-net-worth Canadians can use life insurance to build and preserve their financial capital:

1. Asset protection

Because life insurance is designed to benefit the policyholder’s family, policies generally receive legislative protection from creditor claims when they are structured as such.

“Policies offer creditor protection,” Rozdeba explains. “Death benefits and cash value are typically exempt from claims, except when estate is named beneficiary.”

Note that if the life insurance policy has a preferred beneficiary or irrevocable designation, it is often beyond the reach of creditors during the policyholder’s lifetime.

2. Estate tax funding

At the time of death, a person is presumed to have disposed of all their assets. An executor or liquidator is expected to pay the associated tax before distributing the estate. These include:

- the total value of a registered retirement savings plan (RRSP)

- the total value of a registered retirement income fund (RRIF)

- capital gains realized on non-registered investments

And because of the substantial wealth involved in these assets, they are also often subjected to the highest tax rates. This leads to the legacy being significantly smaller than the original assets. A life insurance policy can help pay these taxes to preserve the asset’s value.

“Probate fees and estate taxes can significantly reduce inheritances; insurance mitigates this risk,” Rozdeba says.

3. Tax-free death benefit

Death benefit payouts from a life insurance policy are not taxable. This means the beneficiaries will receive the whole amount that the policyholder has left them. In addition, permanent life insurance plans allow the insured to potentially grow the money their loved ones are set to inherit, which is also exempt from taxes.

4. Establishing an Irrevocable Life Insurance Trust

Another way for high-net-worth Canadians to keep life insurance proceeds out their taxable estate is by establishing an irrevocable life insurance trust (ILIT). This legal entity is designed to hold and manage a life insurance policy.

“Wealth can be structured through trusts (like ILITs) to further shield it from estate taxes,” Rozdeba says.

When a person owns the policy, the death benefit may end up being included in their taxable estate. This makes it potentially subject to federal estate taxes. Transferring ownership to a trust takes out the death benefit from the taxable estate. This strategy reduces tax liability and allows the beneficiaries to get the full benefit amount.

Through an ILIT, the policyholder, also referred to as the grantor, appoints a trustee to manage the life insurance policy. The policyholder also specifies how the assets will be distributed to the beneficiaries. This ensures that wealth is passed according to their wishes.

But as the name suggests, once established, ILITs are irrevocable and cannot be altered. This is why careful planning and preparation are needed before establishing one. An experienced financial advisor, like our Rising Stars awardees, or an estate planning attorney can help ensure that the trust is structured appropriately.

5. Portfolio diversification

Permanent life insurance is considered as a “non-correlated asset.” This means its value is not affected by market fluctuations, unlike other asset classes, including bonds, stocks, and gold. This allows high-net-worth individuals to invest in an asset that reacts differently to market conditions.

For whole life plans, the cash value is guaranteed and may even increase, depending on how the policy performs.

6. Estate equalization

For high-net-worth business-owner families, life insurance can be used if they want to pass along a business with multiple beneficiaries to a single family member. This also allows them to bequeath the entire business to one family member while still leaving something for their other dependents.

According to brokerage firm Life Insurance Canada, estate equalization operates this way: “The business owner takes out a life insurance policy worth the value of the business and names the other dependent (who isn’t inheriting the business) as beneficiary.

“If there are more children, additional life insurance policies worth the same amount can be purchased. This life insurance strategy also generates more wealth for the next generations, doubling or tripling the business owner’s estate value when they die.”

7. Financing buyout agreements

A buy-sell life insurance agreement is designed to protect a business in the event a co-owner dies. In such an agreement, the death benefit is used to fund buy-sell transactions.

Typically, the benefit amount depends on a relative portion of the company’s value. If there are two co-owners, for example, the death benefit will be 50 percent of the business’ worth. The money is then given to the late owner’s family, while their stake goes to the surviving partner.

A buyout agreement often happens when the remaining owners are not interested in having the deceased’s family stay involved in the business. The family likewise shows no interest in doing so.

There are several ways a buy-sell transaction goes. These include using the proceeds to redeem shares or paying a capital dividend to fund a personal purchase of shares from the deceased’s estate.

To avoid confusion and potential conflict later, the buyout process – including the intended use of the life insurance benefits and the capital dividend account – should be documented in the co-owner's agreement.

8. Key employee insurance

This type of protection is essentially a life insurance policy that covers a vital team member. It provides financial benefit to the company at the time of the employee’s death. It is useful for businesses that rely on specific workers for critical tasks.

The payout is intended to provide monetary support as the company goes through a transition period to find and train a replacement.

9. Charitable giving

Many high-net-worth individuals use life insurance to make a significant charitable donation in two ways:

-

Gifting insurance proceeds to charity by designating a charity as the beneficiary of a policy, and receiving a charitable receipt for the year of death to reduce estate tax liabilities

-

Gifting an insurance policy to charity and obtaining a receipt for the annual premium payments to reduce ongoing tax liabilities

Either way, the charitable institution will receive a substantial amount at the time of the policyholder’s death.

10. Premium financing

High-net-worth individuals can borrow funds from third-party lenders to pay for their life insurance premiums. Under this approach, the policy’s cash value and death benefit serve as collateral for the loan. One benefit of this strategy is that it allows the policyholder to maintain liquidity for other expenses, investments, or business opportunities.

But it also comes with risks. Interest rates may increase, and the policy’s cash value may go down. These situations can push the need for additional collateral or out-of-pocket premium payments.

Here’s a recap of the different ways high-net-worth individuals can use life insurance to grow, manage, and protect their wealth.

How does life insurance work in Canada?

Life insurance comes in several variations, with each type offering different levels of protection and wealth accumulation opportunities. But before high-net-worth individuals can make the most out of these investment opportunities, they must first understand how each policy works.

Life insurance plans work by providing a tax-free lump-sum payment to the policyholder’s family after they die. Coverage generally falls into two categories:

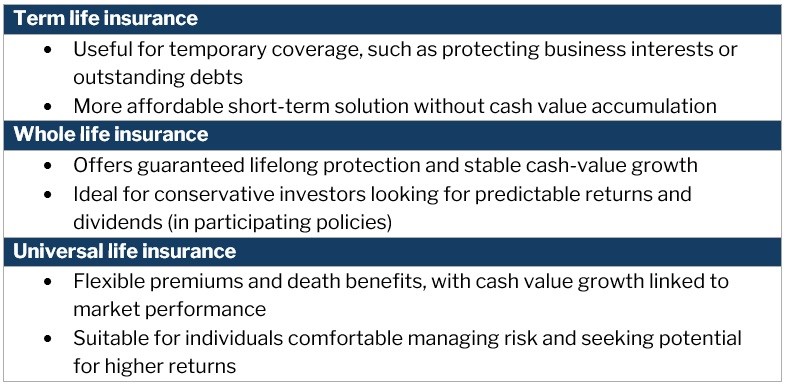

1. Term life insurance

As the name suggests, this type of policy covers the policyholder for a set term. It pays out a death benefit if the insured dies within a specified period. This means they can only access the payment in the years when the plan is active.

Once the term expires, the policyholder has three options:

- renew the policy for another term

- convert the policy to permanent coverage

- terminate the policy

Term life insurance premiums typically increase every time the policy is renewed, often in five, 10, or 20-year “steps,” according to the Canadian Life and Health Insurance Association (CLHIA). If the policyholder chooses to turn their plan into permanent coverage, they can do so without the need for further underwriting but only if it is with the same insurer. This allows them to adjust coverage features to address their long-term needs.

Unlike permanent plans, however, term life policies do not accumulate cash value. This means the insured cannot borrow against their policies or get any cash value back if they cancel.

2. Permanent life insurance

Permanent life insurance plans provide guaranteed lifetime coverage and a cash value element that builds up over time. This value can also be used as collateral if the policyholder decides to borrow. If the policy is voluntarily terminated before maturity or death, the insurance company pays the policyholder the cash surrender value.

Permanent life insurance plans often play a key part in estate planning, allowing businesses to accumulate value long-term and cover estate taxes.

Coverage comes in two main types, with each combining the death benefit with a savings component. These are:

Whole life insurance

This type of policy offers coverage for the entire lifetime of the insured and the savings can grow at a guaranteed rate. Whole life plans can be non-participating or participating.

-

Non-participating whole life insurance: Provides a tax-free death benefit with lifetime coverage and accumulates a guaranteed cash value that policyholders can borrow against

-

Participating whole life insurance: In addition to the guaranteed death benefit, this can generate dividends, depending on how the insurer performs; these dividends are typically issued to the policyholder annually

Universal life insurance

This type of policy uses different premium structures, with the earnings based on how the market performs. Policyholders also have some flexibility in where the funds are invested in, which makes it a riskier option.

Here’s a summary of what high-net-worth individuals should take note of when it comes to these life insurance policies, according to Rozdeba:

“A mix often works best,” Rozdeba adds. “[Individuals can get] permanent policies for long-term wealth management and term policies to cover short-term financial obligations.”

Who can be the beneficiaries of a life insurance policy?

Life insurance policyholders are required to designate a person who will receive the death benefit, also referred to as the beneficiary. This can be:

- the insured’s spouse

- immediate family

- other relatives

- friends

- business partners

- a charitable organization

Policyholders are also allowed to name several beneficiaries for their life insurance plans and assign how much benefit each person or group will receive.

There are two types of beneficiaries:

-

Revocable beneficiaries: Those who the policyholder can replace at any time without needing to inform them

-

Irrevocable beneficiaries: Those who the policyholder cannot replace unless they secure written permission from the beneficiaries

Check out this guide from our sister publication Insurance Business on the basics of life insurance in Canada.

How to find the right life insurance for high-net-worth Canadians

To find the policies that align with their financial goals and desired tax benefits, there are several key steps that wealthy Canadians can take. Here is some advice from Rozdeba:

-

Clearly define your financial and estate planning goals first – this will determine the best type of policy for your needs.

-

Regularly review and update your insurance policies as your life circumstances and financial goals evolve.

-

Consider establishing trusts (like ILITs) to optimize tax efficiency and ensure control over wealth distribution.

-

View life insurance as an integrated component of your broader financial and estate strategy rather than a standalone product.

Finally, Rozdeba emphasizes the value of getting guidance from an industry expert.

“Consult with experienced advisors (life insurance advisor, lawyer, accountant, etc.) who understand tax laws, estate planning nuances, and complex wealth transfer strategies.”

If you’re a high-net-worth Canadian looking for an advisor, our Best in Wealth Special Reports page is the place to go. The companies and professionals featured in our special reports are recognized for their exceptional work in the industry. By partnering with these experts, you can be sure that you’re getting the best guidance when it comes to managing your wealth.