Self-described “perma bull” argues that US earnings & GDP growth point to continued market strength this decade, and potentially beyond

Ahead of today’s SpaceX IPO, Ed Yardeni got a call from his broker asking him if he wanted to buy any. The economist and President of Yardeni Research believes that the IPO is essentially “rigged for success,” because the company will very rapidly be folded into some of the world’s most important market indexes, forcing ETFs to buy it. While much has been made about the $1.75 trillion valuation the company is targeting, Yardeni argues that the IPO is only raising about four per cent of that total capitalization. He asked his broker for 1,000 shares.

The anecdote, shared during a presentation made with Hamilton ETFs in Toronto last week, fits into Yardeni’s broader self-described stance as a “perma bull.” He explained why he remains bullish on US markets, even as more bearish outlooks grow in volume. He compared the current moment on markets to the 1920s, when other technological innovations, improvements in productivity, and growing demand created a historically high stock market. He argues that the “roaring 2020s” doesn’t have to end like its 20th century predecessor and that the underlying forces that drove US market growth for much of this decade so far should remain in place.

“So we had this amazing bull market in the 1920s and then everybody says, ‘if you’re making the analogies to the 1920s and comparing the current decade, that ended badly back then. So that’s not a very happy story.’ My comeback is, let’s make a lot of money during the roaring 2020s,” Yardeni says. “I’d rather be a perma bull than a perma bear. Now, the perma bears are very smart. They’ll give you all kinds of reasons to get out at the top. And sometimes they will get you out at the top, but that’s because it also gets you out in the middle and the bottom. You’ll never be in the market if you listen to the perma bears.”

The metrics backing a bull view

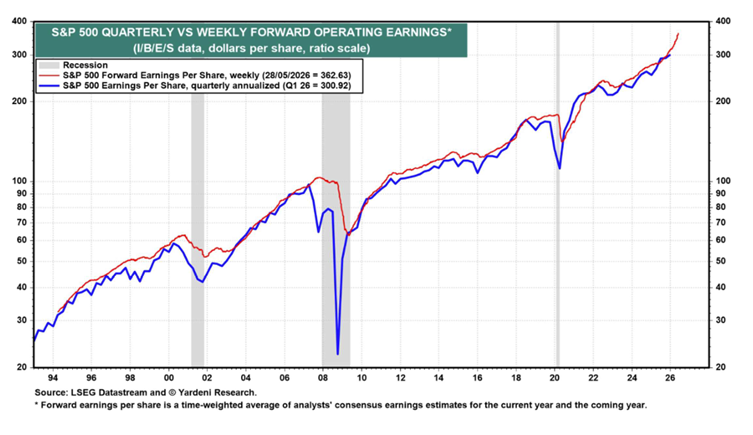

Where his outlook is especially helpful, Yardeni says, is in calling market bottoms. He argues that pullbacks need to be seen as buying opportunities and not reasons for panic, especially when bear-bull ratios imply widespread panic among investors. He believes this because of a broad trend since the 1990s of US corporate revenues, GDP growth, and stock performance all correlating positively with one another. Forward earnings expectations, he says, are still positive and even increasing their pace. Yardeni notes that some alarm bells have been raised about the circular financing arrangements behind some of the AI capital expenditure trend, but he believes revenues are a useful metric to see past that.

Courtesy of Hamilton ETFs

Yardeni argues that recent history supports a perma bull stance. The early 2020s, he said, saw the most widely anticipated recession that didn’t happen. The pandemic, lockdowns, supply chain disruptions, historic fiscal stimulus, surging inflation, the Russian invasion of Ukraine. All of that manifested in a 7-month bear market in 2022 and a ‘rolling recession’ in the US economy that never actually turned into a full-blown recession. Calling back to history, Yardeni notes that the crash that began in October of 1929 had largely stabilized by early 1930, and only the introduction of the Smoot-Hawley tariffs in mid-1930 prompted a lost decade on the US stock market. In the roaring 2020s, markets have already recovered from this century’s great tariff scare.

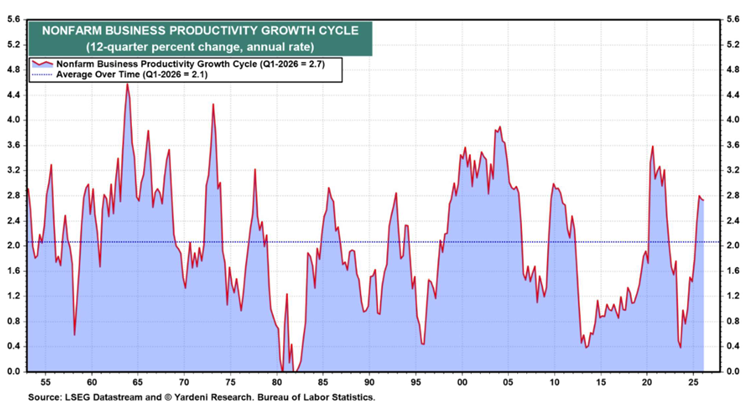

Productivity also underpins Yardeni’s view. He notes that while productivity in the United States has been volatile on a quarter over quarter basis, the three-year average for labour productivity is now sitting just below three per cent, according to the bureau of labour statistics, above the two per cent historical average. Labour inflation, he notes, has also slowed significantly making the marginal cost of productivity growth that much lower in the Untied States.

Courtesy of Hamilton ETFs

Risks and adjustments in a bull market

For all his bullishness, Yardeni does see some risks that advisors and investors should consider. He notes, though, that some of the most discussed risks on the market don’t rate as highly in his estimation. Earnings multiples, he says, are high but not astronomical. He argues that US economic resilience should continue to support earnings growth. He believes the K-shaped economy and the wealth gap between baby boomers and younger generations should be offset by retirements, decumulation, and passing on of that baby boomer wealth to younger generations and the broader US economy.

In the near-term, Yardeni sees the risk of a market swoon in June as investors consolidate from the gains they’ve made since March. Energy inventories are still bone dry and surging oil prices could derail a lot of global economic growth. He also notes that the United States now represents over 65 per cent of the MSCI world index. For all his bullish views on that market, he believes there is some merit in a slight underweight to the United States, making room for emerging markets in portfolios. Despite those risks, he argues that the metrics that imply a looming bear market aren’t worthwhile.

“I don’t think Case-Shiller’s ever been a good trading tool. Hasn’t really been great at calling tops because it’s kind of like a perma bear. It’ll always tell you things are too expensive. I think even the Buffet ratio is so far working even though it’s been going into kind of record high way above what we’ve had in, in the past,” Yardeni says. “I’d rather just kind of stick with the old fashioned forward PE.”