Markets might not correct on valuations, but their current highs could imply a long, painful trough ahead

There is one phrase that makes Thane Stenner wary about investment sentiment: ‘this time it’s different.’ When the Senior Portfolio Manager and Senior Wealth Advisor at Stenner Wealth Partners+ of CG Wealth Management, hears that phrase he’s brought right back to the dot com crash, to the peak of the NASDAQ in March of 2000. While he is not predicting when a correction will come, he says that today’s valuations imply a correction that could be as steep and as long-lasting as the dot com crash.

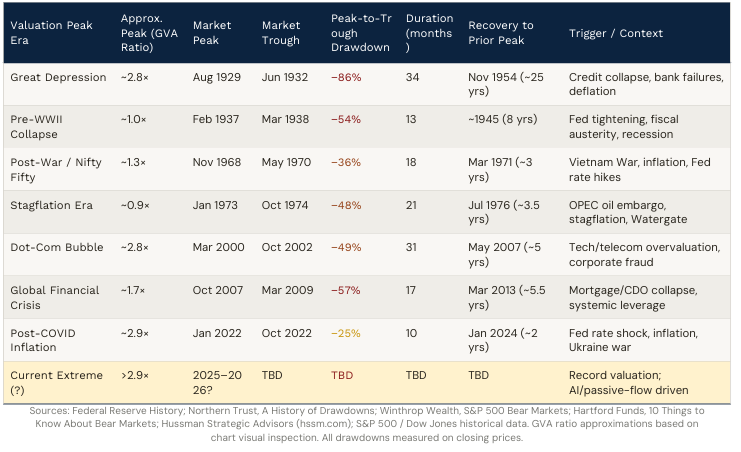

To test his concerns around the extreme positivity and bullish sentiment on markets now, Stenner conducted a review of US equity markets based on their Hussman ratio: the ratio of U.S. nonfinancial market capitalization to gross value-added (GVA). The ratio is maintained and tracked by Hussman Strategic Advisors and pulls data from as early as 1928. As of May 29, 2026, the Hussman ratio has exceeded its peak ahead of the dot-com crash and now sits at 2.9x, higher than the Hussman ratio was before Black Thursday, 1929.

“Valuations give you a snapshot of where we’re at, but it doesn’t tell you exactly when things are going to break,” Stenner says. “I find it fascinating that this is happening right when SpaceX is also in the stratosphere… , there’s always markers when valuations confirm that things are extremely stretched. That’s not an overstatement. And we’re getting three IPOs now, SpaceX, Anthropic, and OpenAI, they’re also queued up to go out. And these are markers that tell me that we’re in thin air right now.”

While the high Hussman ratio isn’t going to tell us when markets will fall, it can be instructive as to how steep and long the pullback is. As the below table shows, market drawdowns anticipated by a high Hussman ratio have tended to last for over two years, with peak to trough drawdowns in excess of negative forty per cent. It has in more than half of the examples cited by Stenner, it took over five years for markets to recover to their pre-correction peaks. Where Hussman ratios have been very accurate predictors, Stenner says, is in calculating forward expected returns on US markets. Right now, the Hussman ratio implies negative six per cent annualized returns on the S&P 500 for the next twelve years.

Stenner isn’t waiting for a crash to reallocate. His client base is entirely in the high net worth and ultra high net worth segments, and he’s making sure that he will be able to raise significant cash for those clients when they need it. He’s putting in portfolio hedges, too, to protect against the downside and he’s allocating more outside the US where he sees valuations at far more reasonable levels. He’s talking to clients, too, to address the bull arguments in this market.

One of the primary arguments that he’s seen clients make for a bull case has been that since the great financial crisis the “Fed put” has been an implied backdrop in markets. Policymakers, the thesis goes, will not let a sustained market drawdown happen and will provide liquidity needed to prevent a meaningful downturn. Stenner argues, though, that while the Fed can prevent a liquidity crunch, they can’t prevent a re-rating of prices by investors. Even after the Fed threw “boatloads” of cash at the market in the wake of the Great Financial Crisis, stocks still fell for 17 months and took five and a half years to fully recover.

The other argument that Stenner hears is one that circles back to that phrase that set off his worry in the first place. Bulls are arguing now that the productivity promises of artificial intelligence are enough to break markets out of their cycle and to justify capitalization in excess of their gross value-added. That argument, Stenner says, amounts to saying “this time it’s different.” It’s an advisor's job, he believes, to reallocate and protect clients, communicating the risks in the market to them while avoiding any cause for panic.

“This is where behavioural coaching comes into play, and this is actually what we get paid to really do for clients,” Stenner says. “Even great investors feel this centrifugal force, this feeling that we can’t miss out. It just takes a lot of discipline at the end of the day. You have to try to be the voice of reason, and you have to try to protect clients from themselves sometimes, and this is one of those times.”