Are IPOs really a winning strategy for everyday investors? Jason Lemire breaks down the data behind first-day pops, retail access, and the long-term performance of newly listed companies

It's plastered all over the news: SpaceX, OpenAI, Anthropic, Databricks, and other massive IPOs are coming our way later this year, beginning with SpaceX on June 12th. However, there’s not much information out there that addresses the complex world of IPOs in sufficient detail, so this article will try to fill that gap.

IPOs: The Empirical Evidence

We are very lucky to have a ton of data and research on IPOs in the US. Indeed, some research articles were published on the topic as early as 1975! But one name consistently stands out as the leading voice on IPOs: Jay Ritter from the University of Florida's Warrington College of Business. Some call him "Mr. IPO"; anyone interested in IPOs should take note of his research.

Sifting through the research, though, it is clear that investors need to partition the evidence into two very distinct phases of the IPO cycle: the Before and the After.

The Before: Here, I mean before the shares start trading on the open market. The investment bank(s) leading the offering market the IPO to institutional investors to gauge demand, using that feedback to set a listing price for the company's shares ("book-building"). Shares are then allocated to participating investors at that fixed price, typically the day before trading officially begins.

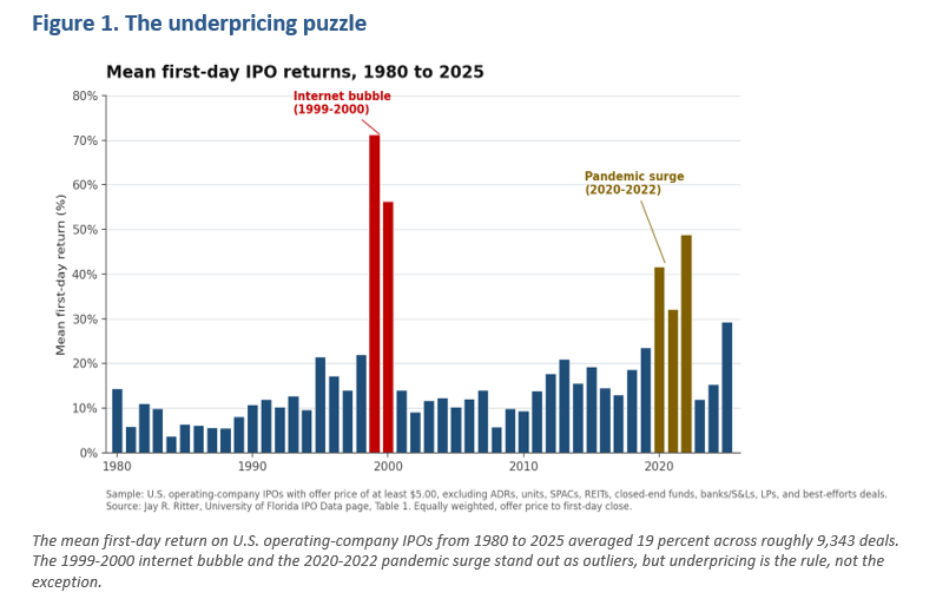

The empirical evidence on this IPO pricing process is quite clear: They are consistently significantly underpriced, meaning they have offered great risk-adjusted returns for investors participating in them.

Over the last 45 years or so, IPOs have generated a mean first-day return of 19%, across close to 10,000 deals! That has created about a quarter of a trillion dollars of value for investors1.

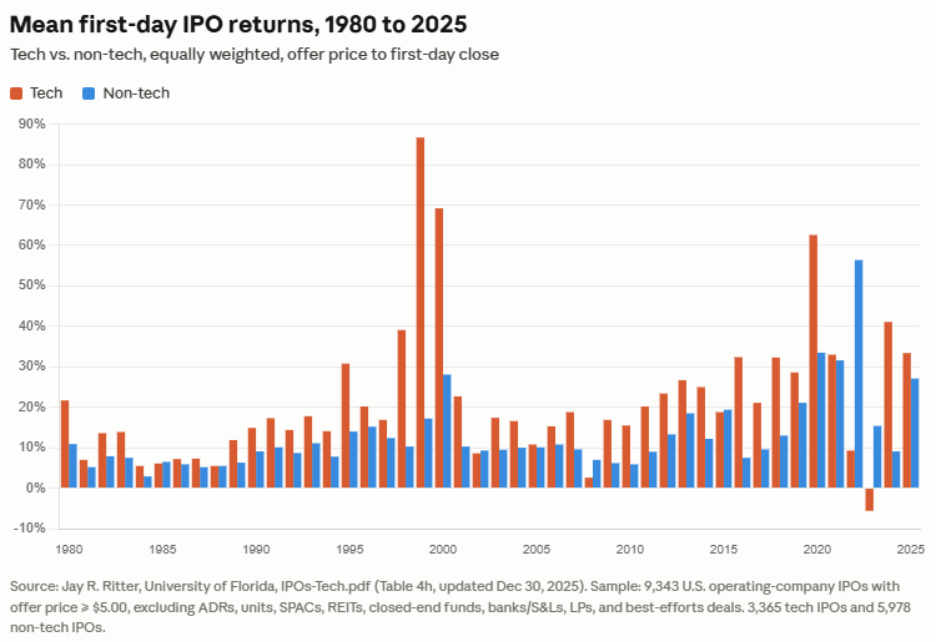

If we segment these numbers between Tech and non-Tech, we see another interesting conclusion: Tech IPOs have performed much better: Mean first-day return of 31% vs. 12% for non-tech IPOs. The last few years, marked by the "AI craze", Tech IPOs have averaged 41% (2024) and 33% (2025), far outpacing once again their non-tech counterparts2.

The conclusion from an asset allocator standpoint seems straightforward, right? Invest as much as possible in these IPOs, and sell after the shares hit the market.

However, it's not that simple. (Almost) everyone knows that IPOs are underpriced, so demand for them is huge. And everyday investors are normally left out entirely of this IPO process. Large, well-connected institutional investors are normally best positioned to get allocations to these IPOs. Put bluntly, the value accrues to them. (note, here: pre-IPO investment strategies where funds acquire pre-IPO stakes in companies and sell them as a pre-packaged product to investors do exist. However, there are complexities and limitations with those products as well.)

So, what is the "normal" way for regular investors to access these "hot" IPOs? It's buying them once they hit the open market. And that's where the empirical evidence is much less in the investors' favor.

The After: Here, I mean once the IPO has started officially trading on the stock market (empirical evidence normally uses the first-day close price as the starting point). Here, we need to be very careful with our conclusions, because the data is very nuanced.

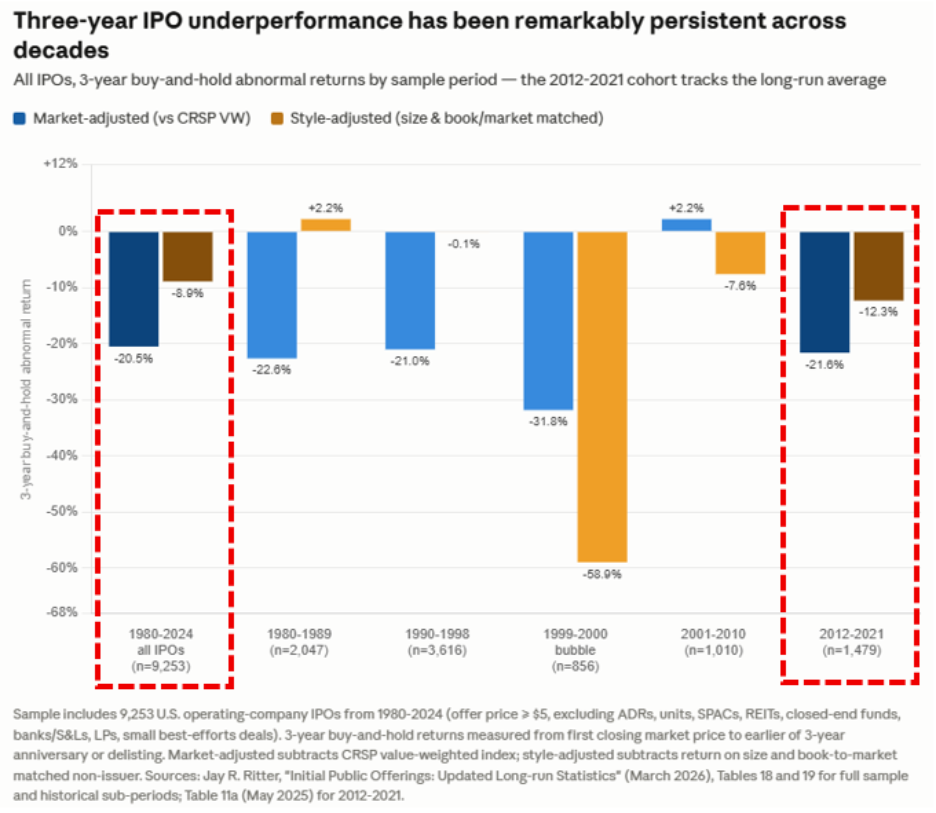

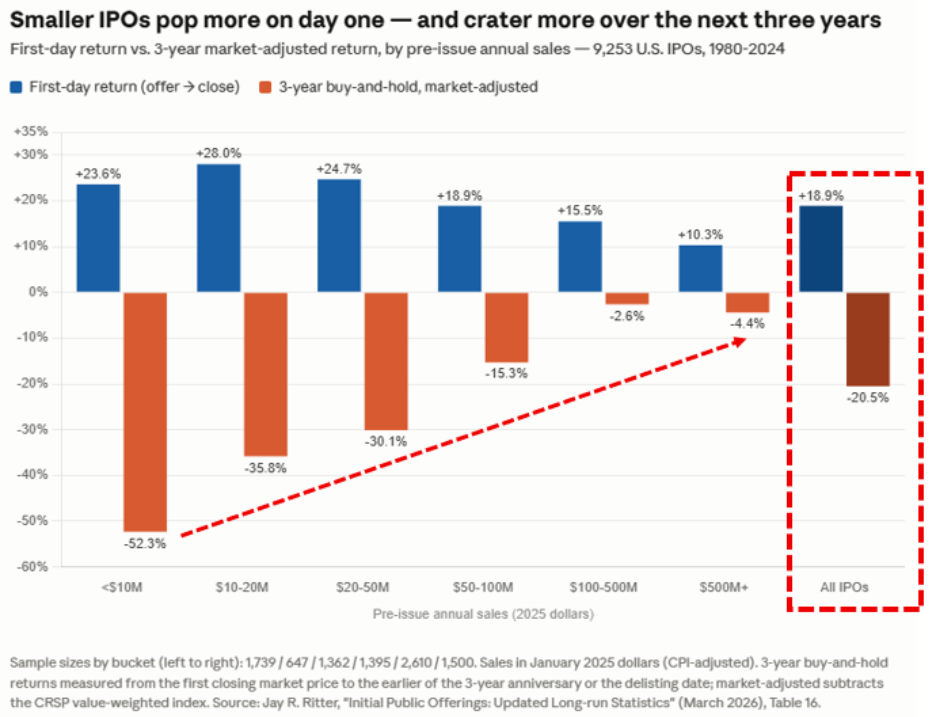

First, when we look at the data globally, we see that IPOs tend to underperform the market in a significant and consistent way over the subsequent three-year period3:

However, when we dig deeper into the numbers, we see that the underperformance is inversely proportional to size. i.e. the smaller companies tend to underperform the most. Larger companies (defined as 500M$ in 2025 dollars, a number SpaceX, Anthropic, and OpenAI easily surpass) have underperformed slightly, but not enough to draw any strong conclusions4:

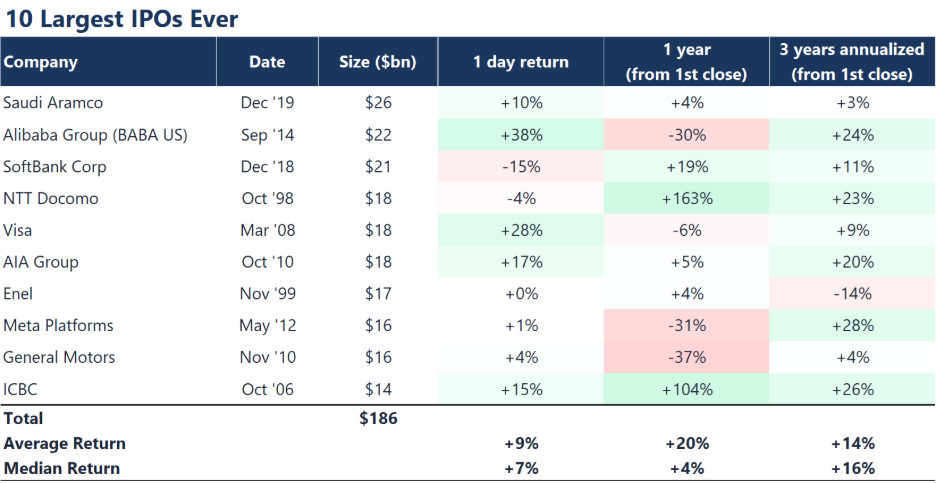

Further, if we look at the 10 largest IPOs ever (SpaceX, OpenAI, and Anthropic should all be larger than even Saudi Aramco), the data does not show evident underperformance... Quite the opposite. But regardless, the sample size would be too small to draw conclusions anyways:

Generated by Jason Lemire (using Bloomberg returns data)

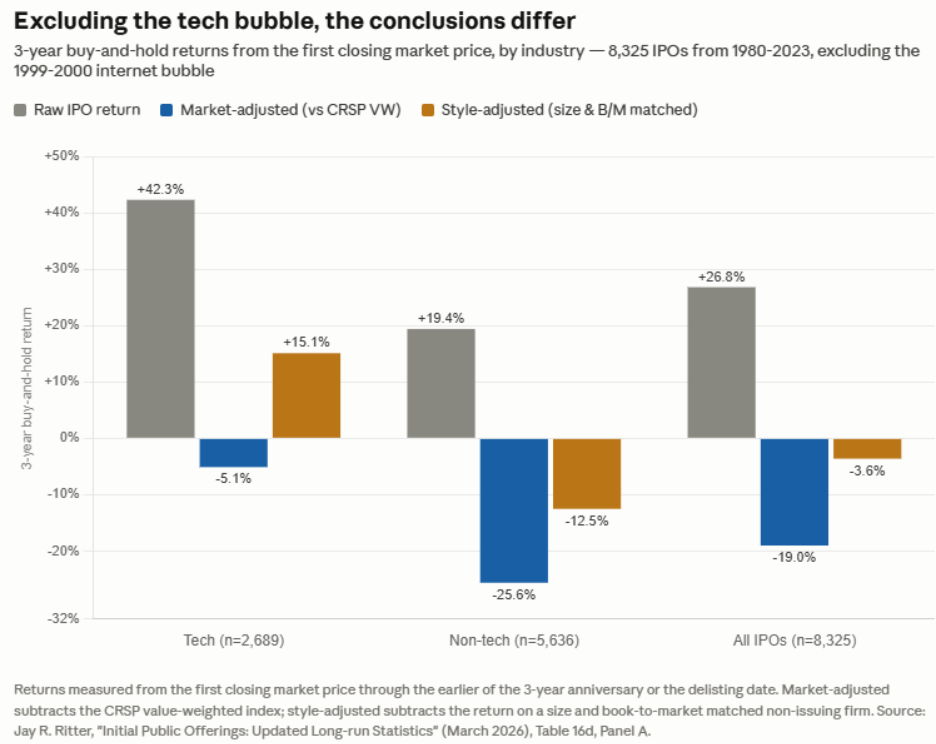

We also need to note that the Tech Bubble of the early aughts had a significant impact on the IPO empirical data. If we were to exclude 1999 and 2000 IPOs (not a good practice, but I'm doing it nonetheless to show the sensitivity of the data), style-adjusted returns are actually positive, and quite good within the Tech sector5:

So, from the data presented, we can see three clean takeaways.

-

First-day pop is real, but accrues mostly to well-connected institutional investors. Retail investors who buy at the open systematically miss it.

-

Long-run returns from IPO buy-and-hold strategies have historically been much weaker than size and style-matched benchmarks, especially for small, low-profitability issuers. A general strategy of buying IPOs near the first-day close and holding for three years has empirically generated poor outcomes. However, the data is much more nuanced, here, as size, profitability, and general market environment all have an important impact on the data.

-

The data does not yield clean conclusions for large cap issuers, so a more detailed, issuer-specific analysis is warranted.

By Jason Lemire, Head of Trading and Portfolio Management at Boldwealth

[1] Source : Jay Ritter IPO databse : https://site.warrington.ufl.edu/ritter/ipo-data/

[2] Source : Jay Ritter IPO databse : https://site.warrington.ufl.edu/ritter/ipo-data/

[3] Source : Jay Ritter IPO databse : https://site.warrington.ufl.edu/ritter/ipo-data/

[4] Source : Jay Ritter IPO databse : https://site.warrington.ufl.edu/ritter/ipo-data/

[5] Source : Jay Ritter IPO databse : https://site.warrington.ufl.edu/ritter/ipo-data/

Disclaimer

The views and opinions expressed in this article are those of the author, a Portfolio Manager at Bold Wealth Partners Inc. (“Bold Wealth”), and are provided for general informational purposes only. They do not constitute investment advice, financial planning guidance, or a recommendation to buy or sell any securities or financial instruments.

Bold Wealth is registered as a Portfolio Manager and Investment Fund Manager in applicable Canadian jurisdictions. The information presented is based on sources believed to be reliable; however, no representation or warranty, express or implied, is made as to its accuracy or completeness. All opinions reflect the author’s judgment as of the date of publication and are subject to change without notice.

This content is not intended to provide personalized investment advice. Readers should consult their own financial advisor or other qualified professional to assess the suitability of any investment strategy in light of their individual financial circumstances, objectives, and risk tolerance.

Past performance is not indicative of future results. Investing involves risk, including the potential loss of principal.

The author and/or Bold Wealth may hold positions in the securities or sectors mentioned and may engage in transactions that are inconsistent with the views expressed herein.

Source : Jay Ritter IPO database : https://site.warrington.ufl.edu/ritter/ipo-data/