Concentration has defined this bull run, and it could be the reason it ends

Ben Jang is Portfolio Manager and Head of Fixed Income at Nicola Wealth.

The U.S. equity market has given investors a lot to feel good about. Earnings have been resilient; artificial intelligence is changing how companies think about growth and productivity, and many of the largest businesses in the world continue to generate substantial cash flow.

The risk is not that the AI story is overstated. In many ways, the opposite is true. The technology is real, the capital being spent is real, and many of the companies at the centre of the theme are not speculative start-ups with no revenue. The more practical risk for investors is this: portfolios that appear diversified may now be driven by a much narrower set of outcomes than they were in the past.

That is the throughline of this article: diversification by holdings is not the same as diversification by sources of return. A portfolio can have hundreds of securities, several sector labels and a familiar benchmark name, yet still be heavily reliant on a small group of companies and one market narrative to keep working.

Five hundred names, fewer drivers

The S&P 500 is often treated as shorthand for the U.S. stock market. That makes sense: S&P Dow Jones Indices describes it as a broad gauge of large-cap U.S. equities, with 500 leading companies that cover approximately 80% of available U.S. market capitalization.

But the index is not built to give every company the same importance. It is market-cap weighted, meaning each company’s size in the market sets its size in the index. As companies increase in value, they become a larger part of the index. When leadership is broad, that structure can still feel very diversified. When leadership narrows, the index can become much more dependent on a small group of very large companies.

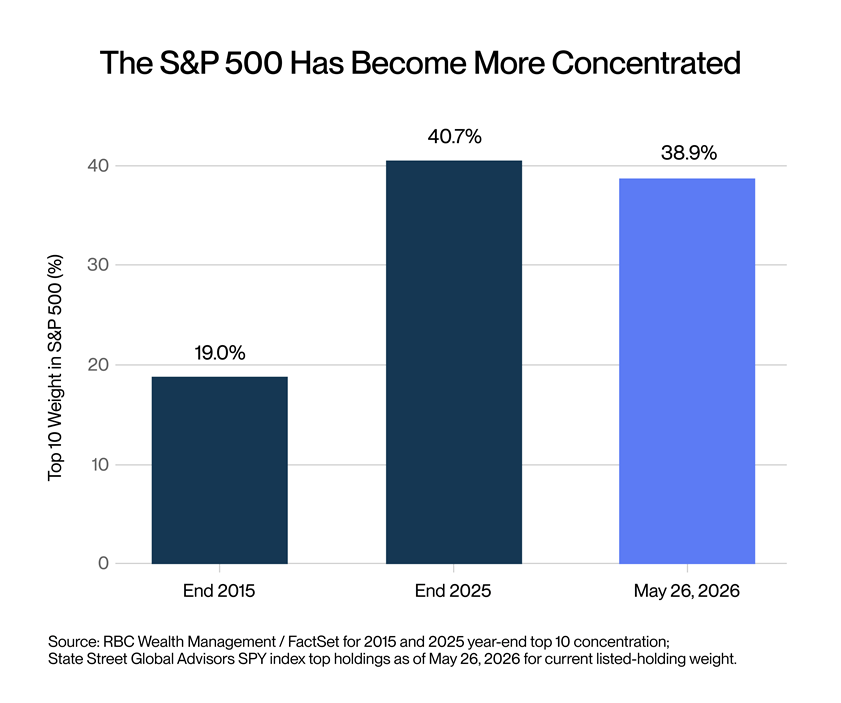

That is where we are today. According to RBC, the 10 largest S&P 500 companies were about 19% of the index at the end of 2015 and 40.7% at the end of 2025. State Street’s SPY index holdings show the top 10 listed holdings at roughly 38.9% as of May 26, 2026. While the exact weight moves with the markets, the direction is clear: a much larger share of the market is now sitting in fewer hands.

This is not a flaw in the S&P 500. It is how the index is designed. The winners become larger, and the index follows them. That can be a strength when the winners keep winning. It can also create a hidden vulnerability when investors believe they have broad diversification simply because the index has 500 names.

A simple way to think about this is a swimming pool. If someone tells you a pool is four feet deep on average, that number is useful, but it does not tell you where a child can safely stand. The same is true in portfolios: averages can mask where the real risk sits. A statement may show hundreds of holdings across several sectors, but if risk is concentrated in one “deep end”, in this case, AI-linked mega-cap growth, the overall picture can feel safer than it actually is.

Sector labels can make the same theme look different

The second layer of concentration is more subtle. Investors often look at sector exposure to understand whether they are diversified. That is helpful, but it can be incomplete. Sector labels tell us where a company sits in an index classification system, but they do not always reflect what is driving investor behaviour.

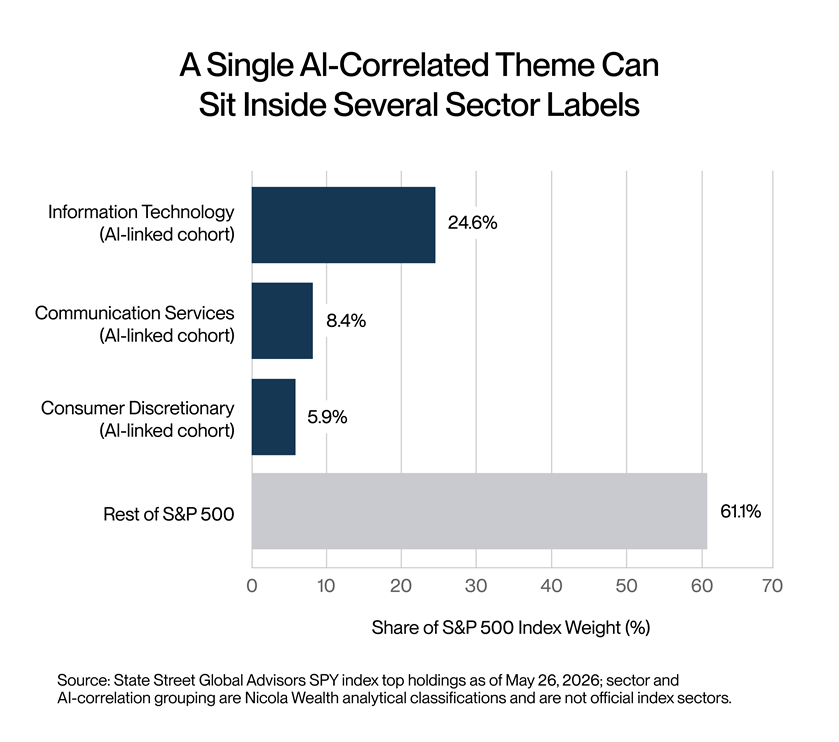

Consider the largest AI-correlated companies in the S&P 500. NVIDIA, Microsoft, Apple, Broadcom and Micron sit in Information Technology. Alphabet and Meta sit in Communication Services. Amazon and Tesla sit within Consumer Discretionary. On a sector pie chart, these appear as three distinct parts of the market. In practice, a meaningful part of their current market narrative is tied to the same set of questions: how much will AI shape the economy, how much capital will be required to support it, and how much of the profit pool will accrue to today’s leaders?

For investors, this matters because portfolio risk is increasingly being defined by themes, not sectors.

Concentration is not the same as being wrong

It is important to be balanced here. Concentration risk is not a prediction that the largest companies must fall. Many of these businesses are large and well established. They have scale, profitability, balance sheet strength, and strategic importance. In some cases, they are building or supplying the infrastructure that may power the next decade of computing.

The question is not whether these are strong companies. It is how much of a portfolio depends on them continuing to deliver the same outcome.

That distinction matters. A business can be excellent and still become a large portfolio risk if too much return depends on it. A theme can be real and still become crowded. A stock can keep going up and still reduce diversification if it grows into an outsized share of a portfolio.

RBC estimated that seven AI-oriented stocks accounted for 52% of the S&P 500’s total return in 2025. That does not make those stocks bad investments. It does show how much of the market’s result came from a small set of names. If the same leadership continues, a cap-weighted index, where the largest companies carry the most weight, will continue to benefit. If leadership broadens, pauses, or reverses, the experience for investors could look very different.

Different mandates can create different outcomes

This is where framing matters. When a diversified portfolio behaves differently than a U.S. mega-cap growth index, the right framing is not “underperformance.” The better framing is that different outcomes are being driven by different mandates.

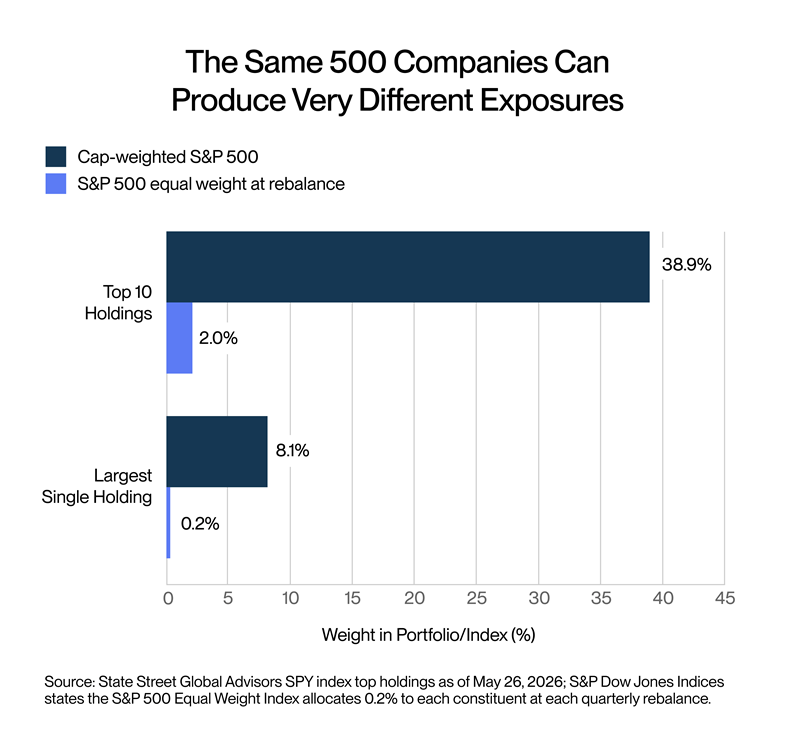

A cap-weighted S&P 500 exposure is designed to follow the largest public U.S. companies in proportion to their market value. An equal-weight S&P 500 exposure owns the same companies but gives each one roughly the same weight at each quarterly re-balance. A diversified multi-asset portfolio has a different job again: it is trying to balance return, risk, liquidity, income, valuation and resilience across more than one market environment.

These portfolios are built to deliver different outcomes and should be expected to behave differently.

What this means to your portfolio

A portfolio can own many securities and still be exposed to one dominant market theme. It is more telling to telling to ask whether different parts of the portfolio are likely to respond differently if the environment changes.

For clients, this means looking through the labels. A U.S. equity index fund, a global equity fund with a large U.S. allocation, a growth manager and a technology sleeve may all be different line items on a statement. But they may still share meaningful exposure to the same AI-led mega-cap trade.

The questions that matter about a portfolio are straightforward:

- How much relies on a small group of U.S. mega-cap companies?

- How much relies on the AI capital-spending cycle, either directly or indirectly?

- How much would still have a reasonable path to return if market leadership broadened beyond AI?

This is not an argument to abandon U.S. equities. It is not an argument to avoid AI. It is an argument to size the exposure honestly and understand what role it plays. Public equities remain an important part of long-term wealth creation. The question is whether they are being asked to do too much of the work

What we are watching

We’re not focused on a single data point, rather, the interaction between concentration, earnings, valuations, and investor psychology.

We are watching:

Market breadth: whether returns are broadening beyond a small group of mega-cap AI beneficiaries.

Earnings contribution: whether the largest AI-linked companies continue to grow earnings fast enough to support their index weight.

Capital spending discipline: whether cloud, semiconductor and data-centre spending earn enough on the capital invested to justify the cost.

Valuation sensitivity: whether higher rates, slower growth or weaker guidance change the market’s willingness to pay high prices relative to company earnings.

Correlation under stress: whether names that appear diversified by sector move together when the AI narrative is challenged.

The bottom line

AI may be one of the most important investment themes of this cycle. It may also continue to create significant value for companies, consumers, and investors. We should not dismiss it simply because it has become popular.

But popularity changes the nature of portfolio risk. When one theme becomes large enough, it can quietly turn a diversified-looking portfolio into a narrower bet. That is the hidden risk in today’s U.S. equity market.

Our view is not to avoid the theme. Our view is that clients should understand it, decide how much to hold, and avoid letting it become the only answer to the portfolio question. Long-term wealth is not built by eliminating risk. It is built by taking risk deliberately, being compensated for it where possible, and pairing it with other exposures that can help a portfolio endure more than one outcome.

That is what real diversification is meant to do.