Are you undercharging? See how your rates compare to average financial advisor fees in Canada

Understanding the average financial advisor fees in Canada is important for both new and experienced financial advisors. Many clients want to know how much they should expect to pay before committing to a long-term financial plan. Since fees can vary based on many factors, being able to explain how your fees compare to industry standards can improve your trustworthiness.

In this article, Wealth Professional Canada breaks down the average financial advisor fees across different service models. We will also review the average salary in major Canadian cities. As we look at how these models work, we’ll help you be become more confident in explaining your value as a professional.

How much is the average financial advisor fee in Canada?

It depends on the location. Check out these major cities in the country and the average fees:

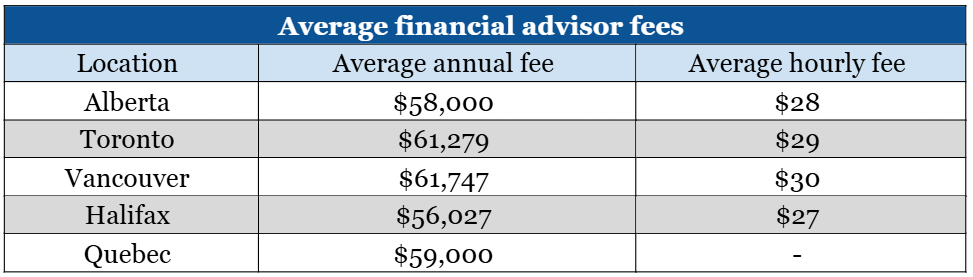

Alberta

In Alberta, the average financial advisor fee is $58,000 per year. Financial advisors in this province often serve a mix of clients, including professionals in the energy sector and small business owners.

Because many clients have mid to high-range portfolios, you can try offering tiered pricing, with lower percentage fees for larger balances. Hourly rates usually cost $28, depending on your experience and certification level.

The market is relatively competitive, which helps keep fees within the national average. However, clients with more complex financial needs, such as farm succession or oil and gas investments, might require more time and attention. This can influence the total cost of services.

Toronto

Toronto is the country's business and financial capital, so average fees are often at the higher end of the national range. You can charge an average financial advisor fee of $61,279 in this province annually. You can also ask potential clients for $29 per hour.

Flat fees for full financial plans can range from a few hundred to thousands of dollars, particularly when tax planning, real estate, or cross-border concerns are involved. To justify the costlier financial advisor fees, investors in Toronto will often expect a more premium service.

Vancouver

In Vancouver, financial advisor fees are similar to those in other large urban centres. The average financial advisor fee is $61,747 per year. Because of the city’s high cost of living and significant real estate wealth, many clients hold valuable non-registered assets. This is in addition to Registered Retirement Savings Plans (RRSPs) and tax-free savings account (TFSAs).

Financial advisors working with high-net-worth individuals often apply sliding scales or customized fee models. While competition in the market helps keep fees reasonable, those with specializations can charge more. Hourly fees usually start at $30, with some firms offering free initial consultations to attract clients.

Halifax

Financial advisor fees in Halifax are generally lower compared to larger Canadian cities. The average financial advisor fee charged here per year is around $56,000. Hourly rates average around $27, though many financial advisors are flexible with pricing depending on their clients’ financial situation and long-term engagement.

Halifax has a smaller market and lower operating costs, which helps financial advisors offer more competitive rates. The client base is often composed of:

- public sector workers

- retirees and unemployed

- small business owners

As such, the services tend to focus on retirement income and government benefits.

Quebec

In Quebec, average financial advisor fees align closely with national standards, typically falling between $59,000 to $66,000 per year. The province’s bilingual and regulated environment means financial advisors often serve clients with unique planning needs. This can include cross-border issues or intergenerational family businesses.

Like other locations, hourly rates will usually depend on your credentials and services. Quebec also has a growing number of fee-only financial planners. This helps improve fee transparency and gives investors more options on how to pay for advice.

As for the average financial advisor fee in Canada, you can earn around $60,000 per year and charge at least $29 per hour. All numerical values used above are from Glassdoor.

Check out this table for better comparison:

Factors affecting average financial advisor fees

The fees for a financial advisor can vary depending on several elements. Understanding these can help you explain to your clients why rates differ from one financial advisor to another:

-

Location: Where you operate can influence how much you charge. Financial advisors in major cities like Toronto or Vancouver may have higher fees compared to those in smaller towns. This is often due to higher business costs and demand for services in urban areas.

-

Your credentials: Those with professional designations might charge more. These credentials show a higher level of training and specialization, which can justify a higher fee.

-

The type of services offered: Comprehensive financial planning usually costs more than investment-only services. The more detailed the planning, the higher the value and the fee.

-

The complexity of your clients’ financial situation: People with multiple income sources, business assets, or cross-border tax issues often need more work and personalized planning. That can lead to higher advisory fees.

-

Your overall experience as an industry professional: Seasoned financial advisors with decades of experience often charge more than new advisors. Their track record and expertise can offer added value to their clients.

Common fee models for financial advisors

Here are some common fee models that financial advisors use:

1. Percentage of assets under management (AUM)

Many financial advisors charge a percentage of the total assets they manage on their behalf. This fee structure is typically around 1 percent of your clients’ assets annually. For example, if they have $500,000 in investments, a 1 percent AUM fee would be $5,000 per year.

2. Flat or hourly fee

Flat fees might range from a few hundred to a few thousand dollars, depending on the complexity of your clients’ financial situation. Hourly rates can also vary based on your experience and expertise.

3. Retainer fee

This type of fee structure involves paying a set amount on an ongoing basis to retain the services of a financial advisor. Retainer fees can cover a range of services such as financial planning, investment advice, and regular check-ins.

4. Commission-based

Some financial advisor services earn commissions on the financial products they sell to their clients, such as insurance policies or investment products. Be aware of potential conflicts of interest in this fee model, as advisors might be incentivized to recommend products that benefit them financially.

5. Combination

Others use a combination of fee structures. For example, they might charge an upfront fee for financial planning services and a smaller AUM fee for ongoing investment management.

6. Project-based fee

If your clients are seeking specific, one-time financial advice or assistance with a particular project like retirement planning or tax optimization, some financial advisors charge a flat fee for that project.

It’s vital to have a clear understanding of the fee structure before providing financial planning services to potential clients. Make sure that they know about any potential additional costs, such as trading fees or administrative expenses that might be associated with their investments.

Additionally, mention any qualifications, experience, and whether you have a Certified Financial Planner (CFP) designation.

When do people usually need financial advisors?

Knowing when people are most likely to seek professional advice can help grow your business. Here are the most common times when clients turn to financial advisors:

1. When their finances become complex

This is especially true for clients who manage multiple investment accounts or receive income from different sources. Investors who own businesses can often engage your services as well.

These types of clients might not have the time or knowledge to coordinate taxes, risk, and long-term planning. You can help by creating a plan that ties all their financial areas together.

2. During life changes

Major events like getting married, having children, getting divorced, or receiving an inheritance usually prompt people to look for financial guidance. These changes can impact their living expenses and financial objectives.

You can provide service by helping adjust their budgets and update insurance or investment strategies.

3. As they near retirement

Pre-retirees need support to make decisions like withdrawing money from their RRSPs and converting them to Registered Retirement Income Funds (RRIFs). Guide them in shifting from building wealth to drawing it down in a smart, tax-efficient way.

4. When they want to learn

Some people look for financial advice because they want to better understand their options. They might not be ready to invest yet, but they want to be prepared. Providing simple yet factual advice builds trust and can turn learners into long-term clients.

5. To manage risk

Insurance is often overlooked until it is needed. Conversations around risk often lead to deeper discussions about their full financial picture.

6. To meet long-term goals

Those who want to save for a child’s education, buy a home, or plan their legacy need structure and follow-through. You can help by building investment plans and checking in to make sure they stay on track.

The value of financial advice goes beyond investment returns. Investors seek your help at different points in their lives, especially when the financial stakes are high.

Knowing when they are most likely to reach out and being ready with cost-effective solutions helps you build lasting relationships and show your worth.

How to show clients that financial advisor fees deliver real value

Choosing the right fee structure is as important as selecting the right investments. Average costs in Canada run from one per cent of assets for full-service advice to a few hundred dollars per hour for planning only.

Before recommending any model, clarify the scope of work and show your clients the amount they will pay per time frame. Be transparent about trailing commissions, account administration charges, and trading costs, so that there are no surprises. Then link each service to a measurable benefit, such as tax savings and improved diversification. You can also go for behavioral coaching during market stress.

Review fees annually and benchmark them against industry data to prove ongoing value. When your clients understand what they receive for every dollar spent, fee conversations become easier, and relationships grow stronger. A clear disclosure plus focus on results will help you demonstrate that professional advice is worth the investment for most clients.

Read next: What is the fee for a financial planner?

Read and bookmark our Investor Resources page for more guidance and information on investment, wealth, and other financial planning topics.