Which option will help your clients earn more – RRSPs or TFSAs? Compare growth potential, tax perks, and long-term value in this comprehensive guide

Helping clients choose between a Registered Retirement Savings Plan (RRSP) and a Tax-Free Savings Account (TFSA) is a common part of financial planning in Canada. Both accounts offer tax advantages, but they function differently and suit different financial objectives. Understanding when to use either or both is the key to making effective, personalized strategies for investors.

In this article, Wealth Professional Canada will talk about RRSPs vs. TFSAs. We will highlight their differences to help you analyze whether an RRSP or a TFSA is suited for your clients’ retirement plans. We will also explore both their advantages and disadvantages for better comparison.

What are TFSA and RRSP?

Let's discuss both strategies for savings so that you’ll know what’s more suitable for your clients:

What is a TFSA?

A tax-free savings account or TFSA is a savings account available in Canada where the money saved by investors grows tax free. These can be:

- contributions

- dividends

- interest earned

- capital gains

Even though it is called a savings account, a TFSA account holds different investments like mutual funds and securities. Withdrawn money from the TFSA is also tax-free.

Your clients’ funds in their TFSAs are not taxable because the money contributed to the account has already been taxed.

To learn more about TFSAs and how they can help your clients grow their savings, watch this video:

What is an RRSP?

Registered Retirement Savings Plan or RRSP is a type of savings plan for employees or self-employed residents in Canada. Opening an RRSP account requires registration with any financial institution like banks or credit unions.

Pre-tax money is deposited into an RRSP account and grows tax-free. Any income that clients earn in their RRSP account is exempt from tax as long as their funds stay in the account. When the time of withdrawal comes, your clients’ income might be taxed at their marginal rate before they receive the payments.

Simply having finances in an RRSP account does not guarantee that your clients can retire comfortably. This is because the growth of its returns is determined by its content. However, what can be guaranteed is tax-free compounded growth while funds remain in the account.

Here’s video on how RRSPs work in Canada:

Is it better to invest in a TFSA or RRSP?

Although a tax-free savings account and registered retirement savings plan both work as a savings account, they still differ in many aspects. To know which is better for your clients, let’s look at some of their differences:

Age restrictions

To open a TFSA account, your clients must be at least 18 years old. However, there’s no age limit for contributing. For an RRSP, anyone under 71 with earned income and who has filed tax returns can have an account.

Annual contribution limits

In an RRSP account, annual contributions are capped at 18 percent of the total income with a threshold of $32,490. The TFSA contribution limit is $7,000.

Contribution deadline

TFSAs do not have any contribution deadline; contributions in this account type are not deductible. As for RRSPs, contributions made in the first 60 days of the new year can be applied to the previous tax year. This 60-day window is set under the Income Tax Act.

Tax advantages

Your clients’ money in their TFSAs will grow tax-free. Their withdrawals are also tax-free, regardless of timing or purpose. In RRSPs, contributions are tax deductible and can be carried forward to be used as a deduction in a future tax year, depending on when the tax break is most beneficial.

RRSPs vs. TFSAs: Spouses or common-law partners

Here are variations for RRSPs and TFSAs when it comes to spouses or common-law partners:

Spousal RRSP and the three-year attribution rule

A spousal RRSP is registered in one partner’s name (the annuitant) but funded by the other (the contributor). This strategy can help your clients balance retirement savings and reduce current taxable income. They’ll also be able to split income more efficiently during retirement.

The contributor claims the tax deduction now, while future withdrawals are taxed in the annuitant’s hands, likely at a lower rate.

The three-year attribution rule for spousal RRSPs prevents short-term tax benefits. Each contribution starts a three-year clock, including the year of contribution and the next two calendar years. If the annuitant withdraws during this time, the contributor is taxed, but only up to the amount they contributed in that period.

After three years, withdrawals are taxed to the annuitant. For example, a $10,000 contribution in 2022 followed by a withdrawal in early 2024 results in that withdrawal being taxed to the contributor. Waiting until 2025 shifts the tax burden to the annuitant.

TFSA contribution and transfer rules for spouses or common-law partners

Your clients can give money to their spouse or common-law partner to contribute to their own TFSA. Any income or gains earned will not be attributed back to the giver. However, each person must remain within their individual TFSA contribution limit.

In the case of a relationship breakdown, funds can be transferred directly between TFSAs without impacting either party’s contribution room. To qualify, your clients must have been living apart at the time of transfer.

The transfer must also be required or allowed under a separation agreement or court order. Such transfers are known as qualifying transfers. The recipient’s TFSA room remains unaffected, and the amount is not added back to the transferor’s room in the next year.

Pros and cons of RRSPs and TFSAs

To maximize either an RRSP or a TFSA, you need to guide your clients and help them understand both options’ advantages and disadvantages:

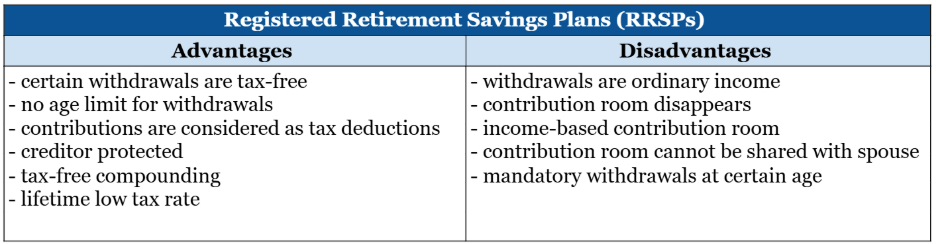

Advantages of RRSPs

-

Certain withdrawals are tax-free: RRSP contributions can be withdrawn by purchasing a house under the Home Buyers’ Plan (HBP) or through continuing education via the Lifelong Learning Program (LLP). These two programs have limitations on their withdrawals and may require that payments be made for 15 years.

-

No age limit for withdrawals: Withdrawals can be made at any age, even before retirement.

-

Contributions are considered as tax deductions: The contributions in an RRSP account are considered tax deductions which can lower net income. This can lead to eligibility for greater government benefits.

-

Creditor protected: Unlike TFSAs, RRSPs are well protected from creditors in the face of bankruptcy or lawsuits.

-

Tax free compounding: Investments made in RRSP accounts grow tax-free. Contributions grow much faster without being affected by annual taxes.

-

Lifetime low tax rate: Contributions can be made during the high tax years and can be withdrawn in low tax years. As a result, this can lower the average lifetime tax rate.

Disadvantages of RRSPs

-

Withdrawals are ordinary income: Compared to TFSAs, post-taxed RRSPs may turn all its gain into ordinary income. Income generated in these accounts gets taxed at a marginal tax rate.

-

Contribution room disappears: If your clients withdraw their contributions in their RRSPs, their contribution room will never come back. There’s no chance of getting it back in the next fiscal year.

-

Income based contribution room: The contribution room that your clients can have in an RRSP is based on gross income. This can be offset, compared to a TFSA where contribution rooms stay the same no matter how big or small the income.

-

Contribution room cannot be shared with spouse: Some couples disregard RRSP as their investment tool because they cannot contribute to each other’s account.

-

Mandatory withdrawals at certain age: RRSPs are closed when the account holder turns 71.

To summarize the advantages and disadvantages of RRSPs, check out this table:

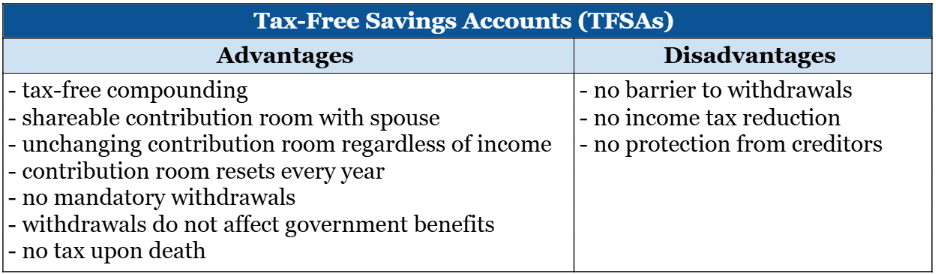

Advantages of TFSAs

-

Tax-free compounding: Investments made in a TFSA grow tax-free, allowing funds to grow faster and earn more without worrying about taxes.

-

Shareable contribution room with spouse: Since the contributions made in a TFSA have already been taxed, there should be no problems if your clients decide to make contributions to their spouse’s TFSA. This means they can share the contribution room with their spouse and take full advantage of having a tax-sheltered space too.

-

Unchanging contribution room regardless of income: Whether your clients experience changes in their income, the contribution room for their TFSA will stay the same. This is great for those who are earning a low and moderate income.

-

Contribution room resets every year: Whenever your clients make withdrawals from their TFSAs, the amount withdrawn is added back to their contribution room when it resets on January 1st of the following year. The same is true for any unused contribution room from the current year. This will work well for short- and medium-term goals.

-

No mandatory withdrawals: Unlike the RRSP that has forced withdrawal at age 71, TFSAs do not come with mandatory withdrawals.

-

Withdrawals do not affect government benefits: Withdrawals made from TFSAs will not be counted as income. No matter how many times your clients withdraw their funds, it will not affect their government benefits.

-

No tax upon death: Since TFSAs are tax-free, there are no tax payments even upon death. Your clients can transfer their assets to their spouse, children or loved ones without impact from taxes.

Disadvantages of TFSAs

-

No barrier to withdrawals: TFSAs do not have any mandatory withdrawals, and this lack of restriction can lead to potential drawbacks.

-

No income tax reduction: Another downside of TFSA is that your clients cannot decrease their income tax when contributing to this account.

-

No protection from creditors: The biggest setback when opening a TFSA is that they are not protected from creditors. If a TFSA account holder files bankruptcy or gets involved in any lawsuit, their account can be seized by creditors.

To summarize the advantages and disadvantages of TFSAs, check out this table:

Is it better to use RRSP or TFSA for down payment on a house?

While some might argue that a TFSA might be a better option, it still depends on the client’s financial situation. A TFSA can provide them with flexibility since it allows tax-free withdrawals at any time and does not require repayment. An RRSP can be used through the Home Buyers’ Plan, which lets first-time home buyers withdraw up to $60,000 tax-free, as long as the amount is repaid within 15 years.

Overall, both account types can serve and help Canadians in many ways—not just in saving or paying for a down payment on a property. It all boils down to your clients’ financial goals, then helping them evaluate whether RRSP or TFSA serves that goal best.

Check out our Retirement Solutions page for more information about RRSPs, TFSAs, and other savings plans.