As the ETF industry continues to grow, so do new ideas for strategies and opportunities. WPC takes a closer look at eight areas where that innovation is playing out in 2019

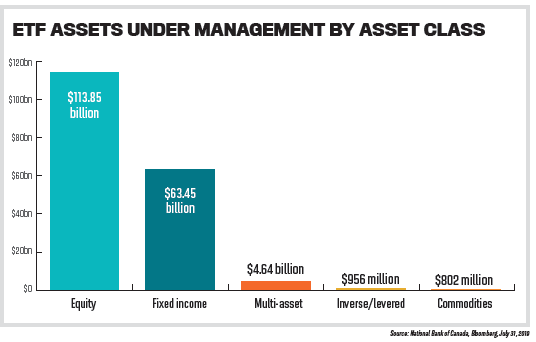

The Canadian ETF industry reached $183.7 billion in assets, spread across 721 funds and 37 providers, at the end of July. The numbers continue to grow at incredible speeds as more investors look to ETFs as their investment vehicle of choice.

As the industry evolves, ETFs are offering more and more options to investors. Products now feature strategies like factor-based investing, portfolio solutions and strategic beta. ETFs are also becoming more specialized. More thematic and ESG ETFs continue to hit the market, allowing investors to put their money behind certain sectors and values.

The past year has seen many developments across the ETF industry. One area of note is alternative funds, which flooded the retail investment space when new regulations were introduced in January. Fixed income has been another highlight of 2019, carrying ETF flows as investors look to insulate themselves against volatile markets while still generating attractive yield.

Given the increased innovation, strategies and options in ETFs, there’s no doubt that this investment vehicle is poised to take on an even bigger role in Canadians’ portfolios.

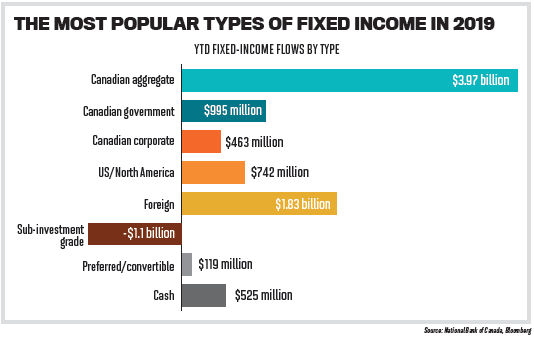

FIXED-INCOME ETFs

So far in 2019, fixed-income ETFs have dominated the story. In July alone, Canadian fixed-income ETFs saw inflows of $1.5 billion, which represented 83% of all flows during the month and one of the highest months for fixed-income inflows in history. Fixedincome ETFs’ current popularity stems from a number of factors, including the fact that they offer more diversification and exposure than single-issue bonds at an attractive price, with the added value of increased liquidity.

One person who has observed the changes in the fixed-income ETF space firsthand is Kevin Gopaul, BMO’s global head of ETFs. BMO has been a leader in fixed-income ETFs, recognized in the top 10 globally, and has introduced several innovations to the Canadian marketplace, including Canada’s first high-yield bond ETF and a discount bond ETF that maximizes tax efficiency.

Gopaul, who recently wrapped up his term as chair of the CETFA, says fixedincome ETFs have come a long way in a short amount of time.

“We always have a lot of inquiries around fixed income,” he says. “Fixed income has always been essential for risk management, portfolio diversification and income generation across all investor types. While fixed-income products are essential portfolio construction tools, there has often been a level of opacity around pricing, bid-offer spread and general accessibility. The emergence of fixed-income ETFs has improved access and efficiency to the asset class.”

The outlook hasn’t always been so good for fixed-income ETFs. Gopaul remembers the challenges the product had just a few decades ago, when brokerage houses classified them as equities simply because they were an ETF.

“There was also a time where market makers had difficulty with fixed-income ETFs, pricing them and having proper bid-offer spreads,” he says. “It has come a long way – now there are products that cover all segments of the global fixed-income market. There is smart beta, active management, and with it all coming together, it has improved the market for fixed-income ETFs.”

Gopaul points to three reasons why fixed-income ETFs have seen a surge in popularity, especially recently. “I think the first is a general movement from single-issuer exposure to diversified strategies,” he says. “The second is the current market conditions, where the need for yield is as insatiable as ever. Finally, the breadth of offerings – there has been so much innovation in fixed-income ETFs, more than pooled or mutual funds.”

In regard to the movement away from single issuers, Gopaul points out that more and more investors are exchanging a single corporate bond for an ETF in order to gain access to a collection of issuers. In addition, the creation of corporate bond ladders has resulted in better diversification and potentially better outcomes for advisors when building portfolios.

As for market conditions, because many experts believe that the current economic cycle is in its later stages, Gopaul feels more money will continue to flow into fixedincome ETFs to lower risk. With more products out there, the choice for satisfying investors’ needs has never been greater.

Gopaul notes that fixed-income ETFs give advisors an opportunity to simplify things for clients, in addition to their other benefits. “Fixed-income trading, pricing and accessibility has always been challenging for the vast majority of the population. Buying a fixedincome ETF can give you the exposure and efficiency at an attractive price – I think that is a key factor. With one purchase, you can have access to hundreds of issuers.”

He also believes the access to professional management appeals to advisors. “There are only so many levers a fixed-income manager can pull to add value: credit, sector, duration, maybe geography. It becomes difficult to show added value. So fixed-income ETFs give you exposure at the price you want. The quality of the manager is becoming key, so large-scale investment managers gain better pricing, insights and access to issues.”

Liquidity is another advantage of fixedincome ETFs. “Diversification can lead to better liquidity,” Gopaul explains. “Instead of one to four lines in your fixed-income portfolio, you can have many more. That improves liquidity, as selling a larger number of smaller pieces of bonds is easier than selling the same dollar amount in one bond. Additionally, it lowers risk, improves diversification and improves portfolios.”

With so many products available, Gopaul stresses that advisors need to know what they’re purchasing. “Understand what your client’s needs are, whether income, portfolio diversification or other, and find the product that matches,” he says. “It’s an area where there’s a need for more information, so aligning with high-quality managers who can give you the support you need with the offerings you need, and at the right price, is important.”

Having a good understanding of products is also one of the greatest challenges with fixed-income ETFs, Gopaul says, as managers continue to launch new products with different outcomes. “As the outcomes become more customized,” he says, “you have to understand what you are getting and make sure it suits you.”

Going forward, he adds, “I think fixed income is going to become more precise, with more specific exposures – for example, just AAA or BBB bonds. The more discussions we have, the more we understand people’s needs and how they differ between clients.”

Gopaul also predicts an increase in active management in fixed income. “There are good active managers in the marketplace who understand the ETF wrapper opens a new distribution channel,” he says, “so I think we’ll see more active in the near future.”

ALTERNATIVE ETFs

Earlier this year, a regulatory update allowed for the offering of alternative investment products by prospectus to retail investors in Canada, and a deluge of products subsequently flooded the market. Yet alternative ETFs aren’t like those in other asset classes.

National Bank Investments was one of the fund providers that jumped on the alternative bandwagon in January. Part of their first suite of ETFs was NALT, an alternative fund that aims to provide non-correlated returns with lower volatility. Terry Dimock, head portfolio manager at National Bank Investments, stresses that the key with any alternative is understanding the product.

“When you are looking at alternatives, you are looking at diversification,” he says. “It is an asset class that is uncorrelated, can lower your risk and protect capital in difficult markets. I think understanding what role an alternative ETF plays in your portfolio is important. You need to make sure you understand the behaviour and how it will perform in both up and down markets.”

Dimock wasn’t surprised to see so many alternative products hit the market at the beginning of this year, as many producers were already using such strategies on the institutional side. Once the rules changed, adapting these strategies for retail investors wasn’t too difficult. Dimock urges advisors and investors to pay attention to the strategies used within an alternative ETF, as they can vary widely.

“There’s a myriad of strategies you can employ,” he says. “It’s more of a question of what kind of expected behaviours you will get from the strategy itself, as well as what type of underlying assets are used to construct the strategy and the role it plays in the portfolio.”

Pierre Laroche, a strategist at National Bank Investments, explains that many common hedge fund strategies can be employed in alternative ETFs, including long/short equities, market neutral and global macro.'

“When you look at global macro strategies, this is where the philosophy may distinguish one product from another,” he says. “Most players position themselves as having good global macro managers who can forecast the market. Then they sell and explain the merits of their strategy. There are different approaches they can take as well, including discretionary, more quantitative, exclusively quantitative and exclusively discretionary. The approaches can also be linked to activities on their institutional desks.”

Given the variety of strategies and approaches, putting alternatives in an ETF format allows advisors to easily find the proper strategy for their clients’ portfolio construction needs. “Alternative ETFs provide simplicity and diversification at a lower cost, which is at the heart of what advisors are trying to help their clients with by providing advice,” Dimock says.

“Typical Canadian investors will be heavy on equities, say roughly 60% equities, 40% in fixed income,” Laroche adds. “Finding an asset class that is not correlated to both stocks and bonds is a challenge. Most advisors have a basket of stocks they can manage properly, but when it comes to, say, commodities, it falls outside of their comfort zone. This is where they need help from professional asset managers to package a portfolio with a sound investment strategy that would expose the portfolio to non-equity strategies. Alternative ETFs give access to an asset class they may not be as knowledgeable about.”

Both Dimock and Laroche point out the potential risks with alternative ETFs, including underlying strategies that could rely on positions of less liquid assets or potential dissatisfaction with returns in bull markets. To counter both risks, understanding the product and the role it’s intended to play in a portfolio remains paramount.

“Advisors need to do their homework,” Dimock says. “Finding the right allocation [to alternatives] is really the heart of their job.

You have to understand the whole view of the portfolio and the needs of every client. You need to understand the role of the alternative, its behaviours and mechanisms. When you do, it will help you build a better portfolio.”

Dimock is optimistic that once people become more familiar with alternative funds and their behaviours, their popularity will grow. “I think it can be a part of a welldiversified portfolio,” he says. “I think equities and traditional fixed income will remain the most important parts, but we’ll see alternatives grow. I think they are here to stay. I don’t think you can lump them into one alternative category – they can be quite different. Homework has to go into really understanding alternatives and how they fit into portfolio construction.”

FACTOR BASED ETFs

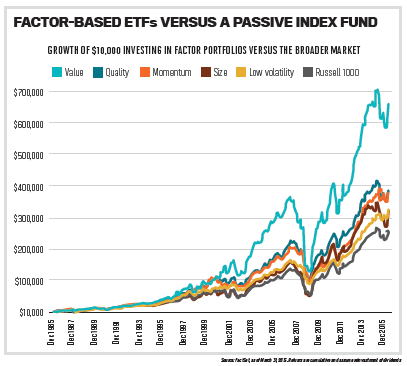

The concept of factor-based investing isn’t new – the idea of focusing on which factors tend to drive stock performance dates back to the 1960s. Back then, importance was placed on market and company risk, but as the industry evolved and more information became available, more risks started to be identified, and ultimately more factors were created.

A number of factors evolved out of this early analysis, including dividends, low volatility, quality, value, momentum and size. Today, factor-based investing has become more common as fund providers aim to offer more customizable approaches to address individual investors’ needs.

“In the early 2000s, factor-based investing started taking off,” says Andrew Clee, vice-president of ETFs at Fidelity Canada. “Essentially the thesis is: identify market anomalies that go against the market hypothesis that says we should be able to outperform broad indices, reduce volatility or enhance the yield. If we can capture these risk premiums, the strategies have the opportunity to outperform or offer superior risk-adjusted returns over time.”

Factor-based ETFs have become one of the fastest-growing areas in the ETF landscape. Clee believes this is because factor strategies put the focus on the client experience.

“Historically, when ETFs launched, 90% to 95% of the market was in market-capweighted ETFs, whether the S&P 500 or TSX,” he says. “Back then, we were essentially saying one size fits all. The conclusion was that every investor should be invested in the S&P 500 or S&P/TSX. We are now getting past ‘one size fits all’ and allowing clients to tailor portfolios to their unique circumstances.”

Clee says focusing on certain factors can help different types of investors by allowing advisors to create a customized portfolio to address specific circumstances.

“A retiree, for example, who lives on their RRSP as source of income has different requirements than an investor who is 30 years old with a 30-year investment horizon,” he says. “If you have a client nearing retirement, income might not be a requirement, but reducing volatility is, so a low-volatility ETF makes sense. Similarly, if you had a retiree who did need income, a dividend ETF would allow them to enhance the yield or income distribution on a monthly basis. If you take high-quality, that allows you to create a higher-quality company profile in your portfolio. With factors, we can address unique needs of each investor.”

Given current demographics and market conditions, Clee says dividend and lowvolatility strategies are the most popular, but momentum and quality are starting to see growth. “I think where we are in the market cycle and with demographics, dividend makes sense, given an aging profile, and with interest rates low, we are seeing clients move into dividend-focused products to enhance yield.”

He notes that factors can be cyclical, and while there is research to show that they tend to outperform the broad market over the long term, there’s also the potential for periods of underperformance.

“You need to understand why you own the ETF,” he says. “If it’s to address income needs, there could be periods where dividends could underperform or overperform, based on moves in the business cycle. I think that cyclicality can be a challenge.”

For advisors looking to incorporate factor strategies into their clients’ portfolios, Clee says the most important thing is to know each client’s unique situation. By determining both short- and long-term goals, advisors can create the most customized solution for the client. “I think factor ETFs can play a pivotal role in the portfolio construction phase because they allow for customization at a more personal level than a passive ETF,” he says.

Clee adds that factors can be used by advisors for asset allocation to express a certain view on the market, or can be used as part of a long-term approach to outperform a passive strategy. He believes factor-based investing will only continue to grow as the industry embraces goals-based solutions.

“Looking at trends around the world, the industry is looking at how a client gets to their end goal,” he says. “Factor-based plays a role in that, in how to build a portfolio that meets the risk/return objectives of the client and their unique goals. I think that will lead to more growth in the factor-based investing space.”

THEMATIC ETFs

In 2018, cannabis ETFs were the focal point of the thematic world. Many investors were looking to gain access to the sector but weren’t quite sure how. In stepped ETF producers, who offered broad exposure to the industry and allowed investors to sidestep the challenge of attempting to pick a single stock winner. Today, the thematic ETF segment in Canada continues to grow as more innovative products hit the market, promising investors access to a variety of exciting industries.

Raj Lala, president and CEO of Evolve ETFs, a leader in thematic ETFs in Canada, stresses the need for fund providers to tread carefully when creating these products.

“We try to look at the long-term trends that get adopted – things we feel make a good investment case – and stay away from fads,” he says. “Once we identify something, we ask: What will a product do in portfolios? Will it generate alpha? Will it be a duplicate of something else? When it comes to themes, it has to be something different.”

As for cannabis, Lala feels that while sentiment has cooled, the industry still has plenty of value. In addition to its global marijuana ETF (SEED), Evolve launched a US-focused marijuana fund (USMJ) earlier this year.

“It has to show that it can perform,” Lala says of the cannabis sector. “The volatility cannabis has seen has deterred people’s desire to invest in it. The industry is entering its second phase, and now it has to be about the numbers, not just future hype. Some companies haven’t had the best reported earnings, which has hurt in the short term, but long term, we still see the growth opportunity.”

“It has to show that it can perform,” Lala says of the cannabis sector. “The volatility cannabis has seen has deterred people’s desire to invest in it. The industry is entering its second phase, and now it has to be about the numbers, not just future hype. Some companies haven’t had the best reported earnings, which has hurt in the short term, but long term, we still see the growth opportunity.”

Thematic producers such as Evolve have started to turn their attention to other opportunities, such as technology. “Cybersecurity can be an interesting subsector to technology because it is an essential service, so even when there is volatility in the markets, it continues to shine,” Lala says. “Artificial intelligence is another area that we continue to see grow; another we see advancing is robotics. I think it all stems around the technological disruption. That will continue to grow and create future opportunities.”

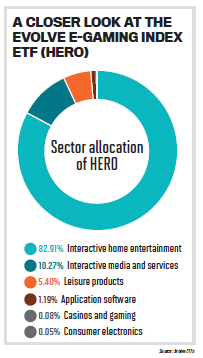

Lala foresees more thematic ETFs coming to market that integrate many of these aspects. Evolve broke new ground with its launch of an e-gaming ETF (HERO) earlier this year.

“If you would have asked me about it eight months ago, I would have said I don’t understand the thesis behind creating a fund,” Lala says. “With research, and looking at the demographics of gamers and the eyes on big tournaments, I realized all of the ancillary businesses that come out of e-gaming. We wanted to create something that could capitalize on the economy around the game – business lines like in-app purchases, events, prize pools, media rights and sponsorship opportunities.”

Another theme that has gained a lot of attention recently is cryptocurrency, but for Lala, the jury is still out. “Some see crypto as a reserve currency; others [see it as] a currency for criminals,” he says. “Some people have moved to it as a protest to their own reserve currency. I think it is easier to accept the blockchain technology behind it. That is a little less controversial because I can see its applications outside of just cryptocurrency. The challenge is that it is currently so closely tied to crypto. Until the two are separated, it is a tough area to be in, but if they do, it will be an approachable investment opportunity.”

He does note that as more big firms get behind cryptocurrency, it’s giving skeptics a little more confidence. “Facebook’s Libra brought it back to life, in addition to the Bitcoin bounce,” he says, but adds that “we still can’t see a clear outcome, and until we do, we can’t be invested in it.”

Moving forward, Lala believes there’s a place for thematic ETFs in portfolios, especially those of millennial investors who are looking to express a certain view through their investments. But at the end of the day, producers need to offer something unique that can perform, especially in the Canadian market.

“The challenge in Canada, compared to the US, is they can get a billion in assets in a thematic ETF,” he says. “We are smaller and have to assume we’ll only get tens of millions before hundreds of millions. You really need high conviction behind a theme.”

ETF FEES

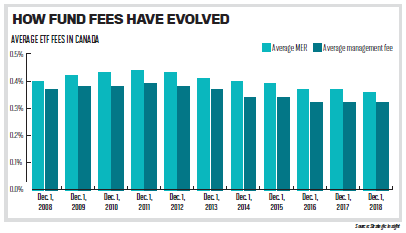

In 2018, the ETF industry saw a race to the bottom on management fees. While fees remain part of the discussion in 2019, Pat Dunwoody, executive director of the Canadian ETF Association, believes the conversation has evolved beyond the fees themselves.

“I think the discussion on low fees has morphed into appreciating what fees are,” she says. “Way back when, the whole discussion about ETFs was that they were cheaper than mutual funds, and therefore you should have ETFs in portfolios. I think we are seeing fee compression everywhere, so while I think that saying is still true, we don’t hang our hat on it anymore.”

Even as the conversation is changing, Dunwoody notes that both MERs and management fees are now the lowest they’ve been in the last decade. While her data doesn’t distinguish between active and passive funds, the overall numbers point to significant fee compression on passive products.

“From 2008 to 2018, MERs went from a 0.4% to a 0.36% average for the Canadian ETF industry,” she says. “It’s not dramatic, but given the number of active ETFs on the market, it says a lot because active fees will be higher. For the overall fees to be lower, the fee compression is definitely showing on the passive side.”

Dunwoody believes fees will continue to trend lower or stay at their current level. “I think there will be too much competition for fees to go up,” she says. “If they go up, they will come down again because someone will fill in the gap. I don’t think we will see fees go the other way. The more educated clients get, the more they become part of the portfolio, advisors are going to have to justify an increase, and I don’t know what that justification could be. The only way you would see it going up for the entire industry is if the assets start swaying to a higher percentage on the active side.”

Still, the discussion on fees has helped the ETF industry attract new assets. Dunwoody says many investors have been approaching their advisors with questions about low-fee products, but it’s up to the advisor to determine if such a product is right for the client’s portfolio. That’s especially true as investors continue to shift their focus from a fund’s results to whether they’re on track to meet their goals.

“They are just really like any other product,” she says. “Regardless of what it is, advisors have to make sure the fee level is just one component they are looking at for clients. Yes, fees are important, but you have to make sure it is the appropriate product and works in their portfolio. So you don’t want fees to be the only factor, but certainly one of the factors.”

Moving forward, Dunwoody doesn’t see the conversation about fees going away, but she does expect it to continue to evolve from focusing on the level of fees to concerns about the transparency behind them.

“DSC fees may be disappearing,” she says, “but there are still low sales charge fees that have the same component – they are still part of the MER, so clients need to be aware of them. The charge may be lower, but it is still buried in the MER. Yes, clients have the fee statements, but they still make statements that they aren’t paying anything, so they are clearly not looking at the fee statement. We have to assume that clients don’t understand [fee structures], and therefore there needs to be more information given to them. You can say the top fund has a low or no fee, but I would hope that there’s a clear appreciation and discussion of the overall cost of ownership of a product. You can only hope that is part of the conversation advisors have with clients.”

ETF PORTFOLIOS

One of the challenges many advisors face is how to effectively service clients with fewer investable assets – a demographic that’s often the most in need of financial advice. As alternate channels such as robo-advisors continue to draw these investors, it’s more important than ever for advisors to find a way to compete. The answer might lie in ETF portfolios.

Essentially an ETF of ETFs, these portfolios provide exposure across a wide range of assets and sectors at a lower cost and can take an investor’s general risk tolerance into account. The idea is similar to balanced mutual funds, which have nearly $750 billion in assets. The ETF industry previously didn’t have the depth of offerings to create these type of funds; however, now that Canada’s ETF space boasts more than 700 funds, these solutions are becoming more readily available.

"It makes intuitive sense that ETF investors are looking for these solutions,” says Mark Noble, SVP of ETF strategy at Horizons ETFs. “It was relatively easy to build an ETF portfolio when there were less than 100 ETFs to choose from. Now even the most seasoned ETF watcher will have trouble keeping up with 700.”

Noble sees ETF portfolios as a more attractive alternative to balanced mutual funds based on their lower cost and flexibility to buy and sell. “It could be the next major area of disruption for the mutual fund industry as self-directed investors and advisors migrate balanced fund solutions to more cost-effective ETF strategies,” he says.

Noble says these solutions target retail investors who are building long-term buy-and-hold strategies and want to outsource the portfolio management component.

“We’ve seen many of these ETFs get embraced by self-directed investors,” he says. “Intuitively, that should make sense, since a big focus for investment advisors is asset allocation, so the segment of investors in need of the most guidance on asset allocation are investors without an advisor. We expect that advisors will eventually gravitate towards these funds as well and use them in smaller client accounts or TFSAs and RESPs.”

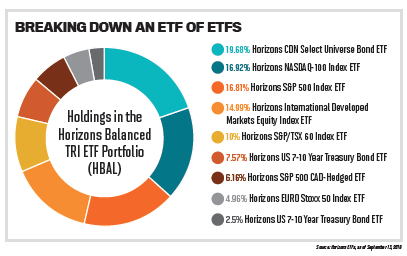

Horizons launched a pair portfolio options, one conservative (HCON) and one balanced (HBAL), earlier this year and recently expanded the suite with a growth option (HGRO). Noble says the success of strategies like this rely on the asset allocation.

“There’s a lot of product and portfolio development in establishing a consistent asset allocation framework,” he says. “From there, it’s pretty straightforward – the ETFs follow that set asset allocation and are rebalanced on a biannual basis to a strategic asset mix of ETFs. In the case of HBAL and HCON, we don’t charge anything on this asset allocation their management fee is 0%. However, investors will pay the management fees of the underlying ETFs in the portfolio, which will be reflected in the MER.”

Making investors aware of the costs associated with these strategies is important. In addition, Noble says an understanding of the composition of the fund is key to setting proper expectations for clients.

“I think the biggest challenge with marketing balanced mandates is that they are diversified, so you tend to be cutting off the top end of the equity performance range due to the allocation to fixed income,” he says. “These ETFs will invariably lag the returns of 100% equity strategies, which sometimes can be confusing to clients who expect larger returns in bull markets. That diversification certainly helps in market declines.”

Noble believes the real value of ETF portfolios is the options they provide for smaller clients. “I don’t think you’re going to see ultrahigh- net-worth advisors putting their clients in balanced ETFs,” he says. “These will be, by and large, used as asset allocation tools to streamline the security selection in smaller client accounts where there isn’t the same amount of compensation to get granular with the asset allocations.”

ESG ETFs

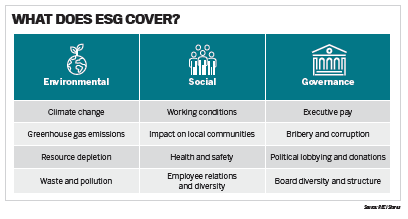

At the Inside ETFs conference in Florida back in February, one of the big topics was the growth and demand for environmental, social and governance [ESG] investing in ETFs, and how North America was lagging behind the rest of the world in incorporating ESG principles into funds.

But Pat Chiefalo, managing director and head of iShares Canada at BlackRock, has noticed that North American investors are starting to close the gap. “We are seeing continued growth in demand, not just about fundamentally incorporating ESG in portfolios holistically, but helping to achieve financial goals,” he says.

Chiefalo believes the future of ESG will include a portfolio tilt, not just a product tilt, and will grow dramatically in Canada over the next five to 10 years.

“ESG today is kind of where factor investing was five to 10 years ago,” he says. “We are in the early stage, with awareness and adoption growing. In the next five to 10 years, flows into ESG-type portfolios and products could rival flows into market-cap-weighted benchmarks.”

With this demand will come a need for increased education for investors. “There are different perspectives on how to incorporate or think about ESG,” Chiefalo says. “Discussions with investors are needed to help them understand how they interpret ESG and how they can translate it into an investment vehicle.”

In addition to education, Chiefalo also feels the industry needs to focus on awareness. “It’s great that investors want to follow a direction, but what’s out there to help them from an infrastructure and data standpoint? It’s important to show how companies are screened and that there is infrastructure and data to work around sustainability and investing. That can help fuel and assemble products that align with how investors are looking to invest.”

Chiefalo says fund managers will need to offer different strategies that help investors express their views, achieve their goals and manage risk. BlackRock, via its alliance with RBC, recently launched the iShares Sustainable Core ETFs suite, a lineup of six ETFs that gives investors ESG exposure that’s aligned with familiar benchmarks.

As ESG ETFs become more prominent, Chiefalo says advisors will need to have conversations with their clients about how they want to incorporate these strategies. “I see more and more clients incorporating more ESG as a requirement in their investment process,” he says. “Conversations will increase around ESG with questions like how much they have, how to get more and how their portfolio reflects it.”

One factor that’s likely to continue to drive the growth of ESG is the transfer of wealth from baby boomers to millennials. “We know millennials put a high degree of importance on incorporating sustainability in investing,” Chiefalo says. “From our standpoint, ESG investing will be linked to helping clients achieve financial goals and enhance long-term performance.”

Once advisors determine what their clients' goals are, a partnership with fund providers becomes important. “We can help with the education and awareness of what products we have in market today,” Chiefalo says. “Also important is that dialogue. We want to better understand the conversation with clients and how they want to incorporate ESG. Do the products we have in the market satisfy their needs? Do we need more? Do the strategies need to change, or do we need to add and adopt greater strategies?”

Chiefalo expects to see more ESG-focused products, strategies and approaches hit the market in the coming years. “I think, locally and globally, ESG ETF assets will rise dramatically over the next decade,” he says. “The demand will come from retail and institutional investors. I see different types of products in the coming years as we look to refine and align better with what investors are looking to achieve in ESG.”

Ultimately, incorporating ESG products makes sense, given that sustainability already surrounds investors in all aspects of their lives. “I think it is an important topic,” Chiefalo says. “If people look around in their day-to-day lives, they will appreciate that sustainability is part of a lot of things they do. We want to make sure, from an investment standpoint, we are prepared to provide the tools and choices they want when they choose to build their portfolios that align with that methodology and strategy.”

STRATEGIC BETA

There has long been a debate about passive versus active strategies in ETFs. Yet strategic beta, which looks to leverage the goals of both active and passive management, is a concept gaining popularity with investors. It’s no coincidence that more fund managers are looking to enter the strategic beta space to provide their own options to investors.

“Strategic beta is a broad term that generally means index-based strategies that aim to deliver outcomes which are different in some way from a traditional index,” says Mark Bankay, head of ETF and institutional product at Manulife Investment Management. “Sometimes that means reducing volatility or generating higher yields or, in our case, enhancing long-term return potential.”

“Strategic beta is a broad term that generally means index-based strategies that aim to deliver outcomes which are different in some way from a traditional index,” says Mark Bankay, head of ETF and institutional product at Manulife Investment Management. “Sometimes that means reducing volatility or generating higher yields or, in our case, enhancing long-term return potential.”

Manulife launched its ETF lineup in 2017; it now has 11 funds, all of which incorporate strategic beta. On the active side, these strategies offer the potential for outperformance by emphasizing specific segments of the market. On the passive side, they offer the benefits of a passive index structure, low cost and transparency.

“Generally, strategic beta strategies leverage empirical research, which can be embedded within investment strategies,” says Darnel Miller, director of ETF distribution and capital markets at Manulife Investment Management. “As an example, Manulife ETFs implement a strategic beta approach based on research showing that over time, stocks of smaller companies with lower relative prices and higher levels of profitability have the potential to outperform over the long term.”

While strategic beta can be applied to a number of areas, one sticks out for Bankay. “Innovations in product design are happening across virtually all asset classes, but the increase in factor-based equity strategies has been very encouraging,” he says. “In fact, strategic beta ETFs have seen a growth rate of approximately 30% in AUM over the past 10 years.”

That growth in assets has gone hand in hand with an increase in product options, Miller notes. “Investors are increasingly looking for ways to balance long-term results with the overall cost of their portfolios, and this investor preference will most likely continue,” he says.

For advisors, Bankay says strategic beta solutions allow them to construct a portfolio that balances costs with results. “For example, many investors hold the majority of their US equity exposure in well-known large-cap companies,” he says. “We’ve found increasingly they’re considering diversifying that exposure into the mid-cap space, and a multi-factor strategy is a great way to do that.”

As more Canadian investors look to use ETFs and become more comfortable with the Management design and strategy behind some of the newer types of funds, strategic beta is an area that’s poised to grow.'

“Mixing thoughtful investment solutions with lower costs is what drives the demand for funds in this space,” Bankay says. “Larger numbers of Canadians are using ETFs as they become more comfortable with newly designed funds and they seek to complement investments in traditional funds.”