As ETFs continue to become an ever more popular vehicle for investor money, Wealth Professional Canada takes a look at some of the most fascinating funds on the market

In 2018, Canadian ETFs outsold mutual funds for the first time since 2009. Despite the volatility in the markets, the industry brought in close to $20.1 billion in net new assets. By mid-2018, the Canadian ETF industry had surged to more than $160 billion in assets before the decline in the markets in the fall. The industry was still able to finish the year at $156.6 billion in assets, which, while not even close to the mutual fund industry’s $1.4 trillion, makes it clear that ETFs continue to grow in popularity.

While some investors have been reluctant to make the move from mutual funds to ETFs, the data shows that millennial investors are choosing ETFs as their preferred investment vehicle. One of the reasons for this is because many ETFs make it easier for investors to understand what they’re actually owning.With numerous products targeted towards sectors or industries, investors have the opportunity to put their money where they want. And the options continue to appear: Canada’s ETF industry saw more than 140 new funds hit the market in 2018.

The year also saw five new companies launch their first ETF products in Canada, bringing the total number of issuers to 33. All of the major institutions have now created their own ETF arm (CIBC recently launched its first four products), and in early 2019, the industry saw one of its biggest shakeups yet when RBC and BlackRock partnered to offer RBC iShares and become the largest ETF brand in Canada.

With so much happening in the industry, Wealth Professional Canada wanted to take a look at some of the most impactful and interesting products on the market to showcase the true range and possibilities of ETFs.

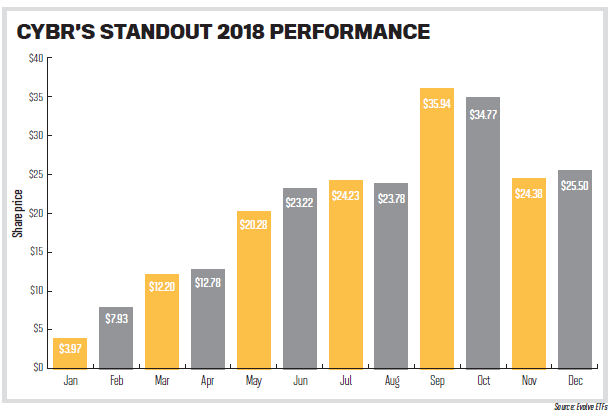

CYBER

Evolve Cyber Security Index ETF

In the modern world, data is constantly sent and received throughout the day. The volume of personal and business-related information on the move raises the risk for cyberattacks and data breaches, a trend that’s only going to grow as artificial intelligence increases the pace of automation. As more aspects of our lives become connected, cybersecurity will only become more important.

That’s something Raj Lala, president and CEO of Evolve ETFs, observed when he decided to launch the company’s Cyber Security Index ETF (CYBR), the first of its kind in Canada and only the fifth in the world, in December 2017. “Technology is so important,” Lala says. “I looked at other parts of the world and specifically HACK, a cybersecurity ETF in the US, to see if it was portable to the Canadian market. I felt strongly that it could work in Canada.”

An analysis published by CIBC in 2017 revealed that cybercrime costs the global economy $3 trillion annually, a number that’s expected to rise to $6 trillion by 2021. Lala identified the area as a long-term trend, not just a fad, and saw the need for a product in the space.

“We wanted to make sure the product had a solid investment thesis behind it,” he says. “Cybercrime is going to continue, so spending to prevent it will have continue. Even if companies have challenges, they will say they are reducing headcount, closing branches or deferring projects, but will never reduce their cybersecurity spend.”

That makes CYBR a good option for investors even if an expected recession hits, Lala points out. “It is in the same category as technology, but it’s not something that creates a shopping experience or product like a phone or watch,” he says. “The products provided by the companies in CYBR are services that governments and major companies worldwide will continue to spend on.”

Indeed, when tech stocks declined in the fall, CYBR was able to remain consistent. Lala says he’s working on spreading the message that CYBR represents a different kind of technology and can help advisors diversify their portfolios.

“A lot of advisors were really too heavy in tech through large companies in the sector like the FAANG stocks,” he says. “But why not allocate towards cyber? It is a different kind of technology that can potentially generate alpha.”

A passive index-based ETF, CYBR uses the Solactive Global Cyber Security Index to select its holdings, focusing on companies with a minimum of $100 million in market cap and a minimum of $2 million daily trading volume. There are 37 holding in the fund, primarily in the US, but Lala notes that even the smallest company in the fund has a market cap of $500 million. While there are other ETFs that have a cyber component to them, CYBR remains the only ETF in Canada that is fully devoted to cybersecurity companies.

So far, the fund has found tremendous success. It was Canada’s top-performing equity ETF in 2018 and was also the best-performing cybersecurity ETF worldwide. It outperformed FAANG in 2018 with far less volatility. And its success helped Evolve become Canada’s fastest-growing ETF provider; the firm had approximately $400 million in AUM as of December 2018. Looking forward, Lala says he has no reason to believe this momentum will shift.

“[CYBR] provides an opportunity for alpha generation, diversifies portfolios, and there is a long-term growth prospect within the sector,” he says. “The most important question that we get asked is, ‘Have I missed it?’ But when you look at what drives CYBR, cybercrime and spending on cybersecurity indicates more growth, and it could still perform well in a recession environment.”

HCRE, HEWB

Horizons Equal Weight Canada REIT Index ETF

Horizons Equal Weight Canada Banks Index ETF

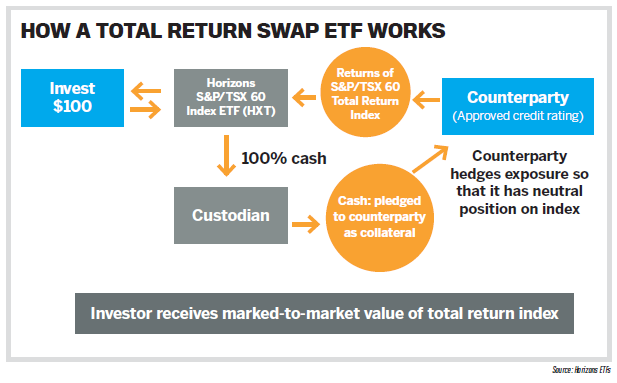

One of the big drivers behind ETFs’ popularity has been their lower cost. But management fees are only one component of those costs; taxes are another significant expense investors face. In many ways, the taxes investors pay on income distributions can far outweigh the costs associated with management. That’s one reason why Horizons ETFs has seen a big uptick in the sales of its family of Total Return Index [TRI] ETFs.

In 2010, Horizons took notice of the frequent use of total return swaps by larger Canadian pension plans and launched the first of what would become a suite of 14 TRI ETFs, each of which provides tax-efficient access to some of the investment world’s most popular index strategies. The company recently bolstered its TRI ETF lineup with the Horizons Equal Weight Canada REIT Index ETF (HCRE), which tracks a Solactive index of Canadian REITs, and the Horizons Equal Weight Canada Banks Index ETF (HEWB), which provides exposure to Canada’s Big Six banks. Horizons also reportedly has a preferred share TRI ETF in the works.

Horizons remains the only ETF provider in Canada to offer investors this specific tax-advantaged approach. “A TRI ETF is a synthetic structure that never buys the securities of an index directly,” explains Mark Noble, Horizons ETFs’ senior vice-president of ETF strategy. “Instead, the cash portion of the ETF is put into an interest-earning cash account. The TRI ETF then provides the investor with the total return of the index by entering into a total return swap agreement with one or more counterparties, typically large financial institutions, which will provide the ETF with the total return of the index in exchange for the interest earned on the cash deposit.

Any distributions that are paid by the index constituents are reflected automatically in the net asset value [NAV] of the ETF.

“As a result,” Noble continues, “the investor only receives the total return of the index, which is reflected in the ETF’s unit price, and is not expected to receive any taxable distributions directly. This means that an investor is only expected to be taxed on any capital gain that is realized if and when holdings are sold.”

TRI ETFs achieve their tax efficiency by allowing the value of their distributions to be reflected directly in their net asset value, rather than paid out separately as a taxable distribution. “It really benefits those investing in non-registered accounts, and TRI ETFs offer the potential for better after-tax returns,” Noble says.

High-net-worth clients in particular often are more concerned about the tax paid on dividends or other types of income distributions than they are about management fees. By using TRI ETFs, Noble points out, investors can potentially save on dividend taxes.

“Let’s say there is a dividend on an underlying stock of 2%,” he says. “Whether you decide to reinvest that or not, you are going to pay tax on it, which could be taxed anywhere from 25% to more than 50%, depending on your income level and whether they are Canadian or foreign dividends. That could cut the dividend in half. However, by using a TRI ETF, the dividend isn’t distributed to the ETF holder and is instead reflected in the ETF, typically resulting in no immediate taxation of dividends for the investor. Over time, this can potentially save investors hundreds or even thousands of tax dollars.”

Another key element of TRI ETFs is reduced tracking error. When an ETF physically replicates an index, it typically mandates that regular distributions, dividends or interest from the underlying securities be accrued during the year and paid out on a scheduled distribution date. As a result, the cash held within the structure does not participate in the index returns, creating a drag on the performance of the ETF. This, combined with the ETF’s transaction costs from rebalancing, contributes to tracking error. In a total return swap structure, these issues are essentially eliminated since the counterparty delivers the total return of the index. Thus, a TRI structure can greatly reduce the potential for tracking error.

The appeal of the TRI ETF suite’s tax efficiency has allowed Horizons ETFs to compete with larger players and become the fourth largest ETF provider in Canada. “When we came to market, there wasn’t a lot of space for us to compete with the larger companies,” Noble says. “We needed to differentiate ourselves, and one way we did that was by offering these tax-efficient funds.”

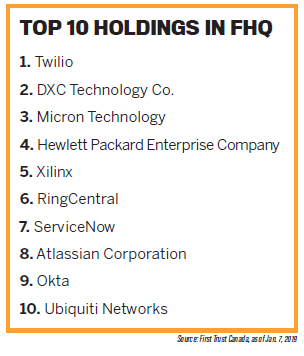

FHQ

First Trust Alphadex US Technology Sector ETF

After being a standout for some time, the technology sector has experienced some well publicized challenges over the last few months. Yet Karl Cheong, head of distribution for Canada at First Trust Portfolios, believes his company’s theoretical approach to its Alphadex US Technology Sector Index ETF (FHQ) will help it remain a strong option over the long term.

“What is so different about the fund is it doesn’t hold the FAANGs in a material amount,” Cheong says. “The traditional S&P 500 Technology ETF was very top-heavy with Apple, Google, Facebook and others that have driven the bus. We have been able to generate that type of performance without holding those FAANG stocks in a material way.”

FHQ is part of First Trust’s global Alphadex suite, which was originally launched in 2007 and has since found tremendous success. Introduced in 2014, FHQ was First Trust’s solution for adding technology exposure to Canadian portfolios.

“Tech in Canada is a very small portion of the overall market, whereas the technology sector represented approximately 25% of the S&P 500 and is very global in nature in terms of percent of income from foreign profits,” Cheong says. “Therefore, we saw an opportunity to add diversity to Canadian portfolios. We launched a hedged and unhedged version, and since then, it has been a way to add exposure to the best-performing sector over the last 10 years.”

What sets FHQ apart from other technology funds is the methodology behind it. Its multifactor model starts by identifying the best growth and value stocks in the Russell 1000 Index, which is composed of mid- and large-cap tech stocks. First Trust then narrows down the index to the top 75% of stocks based on value and growth scores. Then it equally weights each quintile, putting the top-scoring stocks into the first quintile and the lower scoring ones into the bottom.

“We don’t highlight any particular name, unlike traditional market-cap-weighted portfolios,” Cheong says, “so it is very much a balanced play toward the sector – usually stocks that are not well covered or familiar to Canadians. We held a lot of semi-conductor stocks over the last couple years. Picking up names that are not well covered led to the outperformance.”

“We don’t highlight any particular name, unlike traditional market-cap-weighted portfolios,” Cheong says, “so it is very much a balanced play toward the sector – usually stocks that are not well covered or familiar to Canadians. We held a lot of semi-conductor stocks over the last couple years. Picking up names that are not well covered led to the outperformance.”

That outperformance led FHQ to win a Thomson Reuters Lipper Award this past fall, which is given to the funds that have generated the best three-year risk-adjusted returns in the Canadian equity sector at the time of the award. Even though the tech sector has seen a major selloff since then, Cheong is hoping that the makeup of the fund will bring investors back to the sector.

“We still like tech, given its earnings profile,” he says. “It sold off dramatically in Q4, which creates a buying opportunity for longer-term investors. The question is, will people listen?”

Cheong is optimistic that investors will return to tech for a number of reasons. “Hightech capex spending is still trending higher, which is a positive for the sector,” he says. “When you look at what companies are most likely to spend on, most likely it will include technology, and that won’t go away. There is an incentive, now more than ever, to automate with technology and reduce costs/improve profit margins, given higher wages.”

Cheong also notes that consumer technology trends are still positive. He urges advisors and investors to think long-term, because in the short run, no one can predict where prices will go.

“I expect the technology sector to benefit, despite risks from trade squabbles, from pervasive digitization across the economy, high cash levels and low debt,” he says. “Investors should hold technology stocks because they are fundamentally healthy companies and relatively immune to higher interest rates. Overall, we are still more bullish than bearish in the long term, as most of the earnings growth in the S&P 500 will come from technology-oriented firms.”

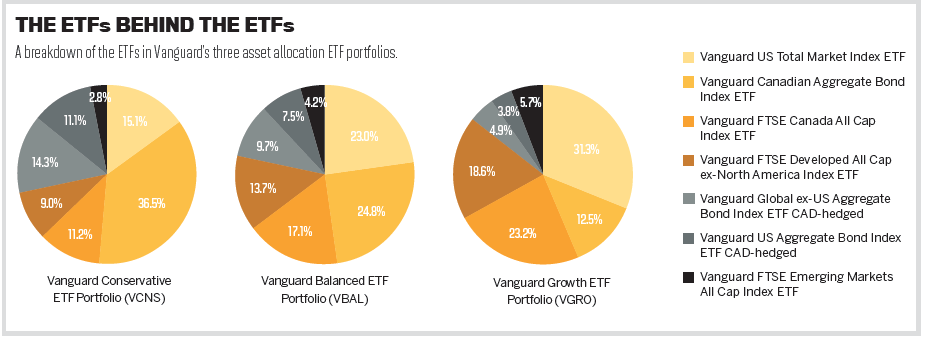

VCNS, VBAL, VGRO

Vanguard Conservative ETF Portfolio

Vanguard Balanced ETF Portfolio

Vanguard Growth ETF Portfolio

As more advisors transition to a fee-based compensation model, the importance of showing value to clients becomes paramount, as does the ability to provide a scalable option for smaller clients. Vanguard Investments Canada believes the answer to both of these issues lies in its asset allocation ETFs.

The fund manager launched its suite of asset allocation ETFs last year. The Balanced ETF Portfolio (VBAL) has a traditional 60/40 split between equities and fixed income, the Conservative ETF Portfolio (VCNS) reverses it to 40/60, and the Growth ETF Portfolio (VGRO) offers an 80/20 split. The three options offer different risk profiles that align with specific investor risk tolerance.

“This has become one of the fastest-selling areas in the industry,” says Tim Huver, head of product at Vanguard Investments Canada. “We have already seen more than $900 million in AUM. Advisors are gravitating towards these balanced products.”

The three portfolios are actually ETFs of ETFs; each one consists of seven underlying Vanguard ETFs, which ultimately provide investors with access to more than 25,000 different holdings with weightings adjusted based on the specific strategy.

“The asset allocation ETFs can be a one-ticket solution and serve as a portfolio on their own,” Huver says. “For many advisors, they can use them to serve as a core holding in a portfolio with satellite strategies around them. As one of the lower-cost options, at only 22 basis points, they provide a compelling offering.”

Vanguard’s creation of this product suite was prompted by an observation of trends in the market since the 2008 financial crisis. Huver notes that “investors began to see the benefits of a balanced portfolio … These ETFs have a sound construction and offer global and asset diversification. For advisors, that can provide a scalable solution for the smaller clients in their book with the broader industry shift towards fee-based models.”

Huver explains that a one-stop portfolio option can help free up time for advisors to focus on other elements of their business. “With greater importance now being placed on financial planning, these ETFs allow advisors to set the assets and focus on other value-added services such as tax planning and behavioural coaching.”

Because of their vast holdings, these products provide an efficient way to gain access to numerous underlying markets, though Huver notes that there is a 30% overweight to Canada. The ETFs are rebalanced by Vanguard’s asset management team, so advisors and investors don’t need to worry about the weighting ever falling out of line with their individual risk tolerance.

“These are a ‘set it and forget it’ approach, as we handle the rebalancing,” Huver says. “The ETFs are also very versatile and can be used in different account types like RRSPs and TFSAs. They are popular because they are an alternative way to add balanced products at a lower cost than other options on the market.”

Learn more about the diffence between RRSPs and TFSAs here.

HHL

Harvest Healthcare Leaders Income ETF

Traditionally, healthcare investing hasn’t held the same representation in Canada as it has around the world. In Canada, it makes up just 2% of the market, while globally, it represents closer to 15%. Because healthcare is a sector with potential for long-term growth, Harvest Portfolios wanted to bring the Canadian market greater access to it in the form of the Healthcare Leaders Income ETF (HHL).

“The Healthcare Leaders Income portfolio brings together 20 of the best leading global healthcare companies,” says Paul MacDonald, CIO at Harvest Portfolios. “It uses our covered call strategy to create more income and is exposed to a diverse group of healthcare companies.”

The healthcare sector’s long-term growth appeal was the driving force behind the fund’s original launch as a closed-end fund in 2014. (It was later converted to an ETF in 2016.) “We look at sectors with long-term growth, and healthcare has more of that than any other,” MacDonald says. “We noticed that there was limited opportunity for investors in the sector, but since it has a sound structural backdrop, that makes it worthwhile.”

Harvest considers healthcare to be structurally sound for three key reasons: An aging population will continue to spend on healthcare no matter the state of the market, developing markets are increasing healthcare spending disproportionately to rising income, and the space is seeing plenty of technological innovation.

Because there are thousands of companies in the healthcare sector, Harvest employs a specific strategy to narrow the field. “We have a proven process to gets that number down to something more manageable,” MacDonald says. “We start with companies that have a minimum US$5 billion market cap and some specific financial criteria, which gets us down to about 75 companies. From there, we actively select 20 that we think are leaders in their subsector and then diversify across those subsectors so we are not overexposed to any one area in a subsector.”

Because there are thousands of companies in the healthcare sector, Harvest employs a specific strategy to narrow the field. “We have a proven process to gets that number down to something more manageable,” MacDonald says. “We start with companies that have a minimum US$5 billion market cap and some specific financial criteria, which gets us down to about 75 companies. From there, we actively select 20 that we think are leaders in their subsector and then diversify across those subsectors so we are not overexposed to any one area in a subsector.”

The process ensures that the fund gains broad exposure, but MacDonald says Harvest will only add a company if it has a proven ability to extract value. This process produces significant benefits for the fund.

“The number one is it provides exposure to a sector with a robust growth upside,” MacDonald says, “and also diversification and, with our covered call strategy, a highly tax-efficient distribution.”

He specifically points to diversification as something that makes HHL valuable to advisors. “All investors want to make sure they have diversity, even in a specific sector,” he says. “You can own the stock of the largest company in a sector, but even it could have something happen to drop its value. So you need to diversify across the space.”

MacDonald adds that the fund adheres to the philosophy that the best offense is a good defence. “Healthcare is such a big component of the global market; it is structurally sound, offers growth and provides defensive characteristics. People are still going to buy their medication in a down market. The advancement of drugs and new devices is amazing. I like to say we are only in the seventh inning of development, which is moving at a rapid pace.”

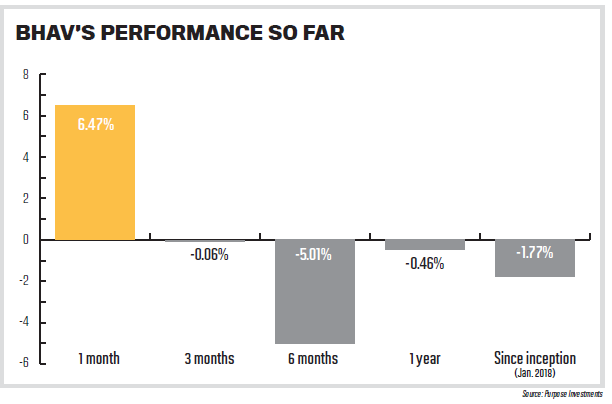

BHAV

Purpose Behavioural Opportunities Fund

As much as investors try to keep their emotions out of their decisions, when it comes to the financial markets, the bias never fully disappears. This observation encouraged the team at Purpose Investments to think about whether they could find profits in the mistakes of investors, and the Purpose Behavioural Opportunities Fund (BHAV) began to take shape.

“Two years ago, we started thinking that if emotions, behavioural biases and mistakes in the market happen, and a lot of people can be making similar mistakes, could those mistakes cause an asset to be mispriced – and then can we profit from it?” says Craig Basinger, CIO of Richardson GMP, who manages BHAV on behalf of Purpose.

Launched in January 2018, BHAV is designed to profit from mispriced assets caused by the behavioural mistakes of other investors, but the ETF really goes deeper with a methodology that studies human behaviour and the decision-making process. Purpose Investments’ process believes that investors are their own biggest challenge, often making mistakes that include holding a position too long, suffering from a home bias and chasing performance.

“If a whole bunch of investors are going to make poor decisions and make poor trades, how can we make money off them?” Basinger says. “That’s when we started developing the strategies that sit in BHAV.”

While some of the strategies his team uses have been used elsewhere in other variations, Basinger notes that his team’s specific methodology is pretty unique to what Purpose is doing. The fund employs multiple strategies, but the main one is what Purpose refers to as “unloved to less unloved.”

“We realized there was a herd mentality around companies with a high proportion of analyst buy ratings,” Basinger explains. “That caused overpricing towards the high-buy companies and underpricing towards other companies. What we found worked really well was if you look at companies that have gone unloved for a long period of time – three months or longer – they get beaten down, neglected, and their share price gets depressed. When they start to see some upgrades, they tend to have a strong run and mean aversion in their stock price.”

The other prime area where BHAV looks to capitalize on investors’ behaviour is with earnings results. “If you believe a company’s worth should be on its discounted cash flow, a company missing its quarterly earnings by a nickel shouldn’t impact the valuation very much, but that’s not what we see,” Basinger says. “It can go up or down by, say, 15%, caused by recency bias on the news that comes out.”

What Basinger and his team have found is that the market often overreacts to this news, both positively and negatively. “Highquality companies that miss earnings will see many people buy it on sale and bid it up,” he says. “On the flip side, if you are a low-quality company – measured by historical volatility or the beta of the company – and have a positive earnings surprise, we find those gains are fleeting, and they bleed back quickly. If you think of the shareholder and their behaviour, they may have wanted to sell that company for a while and now have the opportunity on the sudden spike higher. So when it gets that surge, those investors sell, and that leads to the gains bleeding back.”

With a goal of long-term capital growth, BHAV is a full prospectus fund that has a little bit of everything, but is predominantly made up of North American equity securities. “There are thousands of analysts who try to determine the value of a company,” Basinger says. “What we are trying to do is capitalize on when people are making mistakes on those mispriced assets. The strategy behind BHAV is unique because we are focusing on the other side of the trade.”

He adds that while there are hundreds of value and growth funds out there, BHAV is currently the only behavioural-focused ETF in Canada. “The capability the fund has to generate alpha should give it longevity because investors will always make emotional mistakes,” he says. “This is an alternative to capitalize on other factors in the market. I think as we move forward with investment management, more people will focus on the people making the trade.”