Get to know the biggest robo-advisors in Canada. This guide lets you understand who's leading the digital investing space and what it means for your practice

Robo-advisors have become a permanent part of the Canadian wealth management space. These digital platforms use algorithms to build and manage investment portfolios with minimal human intervention. They aim to make investing easier, faster, and often cheaper than traditional advisory models.

While most were originally built for retail investors, financial advisors in Canada are starting to explore how robo-advisors can be used to complement their services. Some firms partner with them directly. Others view them as competition. To know more about them, Wealth Professional Canada provides a list of robo-advisors in this article.

Robo-advisors in Canada

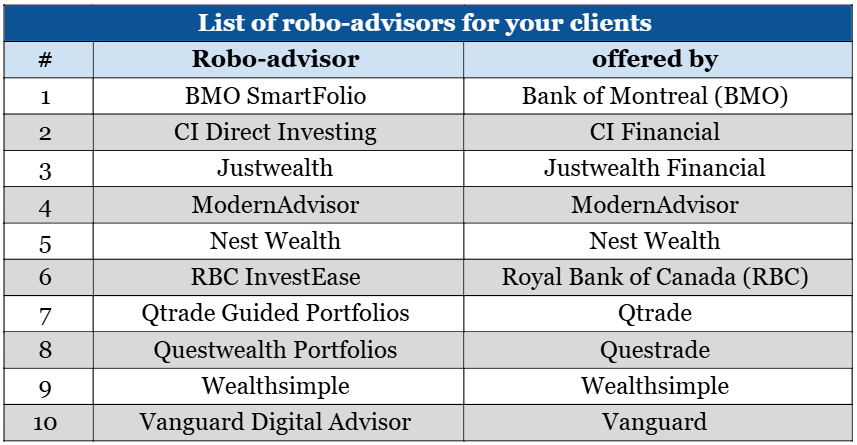

There are a lot of robo-advisors available in the country. The question is, which of them should investors pick? Check out the selection of robo-advisors that we’ve curated below:

Let’s discuss them at length:

1. BMO SmartFolio

BMO SmartFolio is a professionally managed digital investment platform that offers your clients a hands-off investing experience. It’s built by Bank of Montreal, and it combines the efficiency of a robo-advisor with the oversight of experienced portfolio managers.

Portfolios under BMO SmartFolio are monitored and adjusted by a team with centuries of combined investment experience. Advisory fees range from 0.4 percent to 0.7 percent, offering cost-effective solutions for clients seeking transparency and automation.

As for account types, BMO SmartFolio offers registered plans such as:

- Tax-Free Savings Accounts (TFSA)

- Registered Retirement Savings Plans (RRSP)

- Registered Education Savings Plans (RESP)

- Registered Retirement Income Funds (RRIF)

Non-registered options such as Individual and Joint accounts are also supported.

Read next: RRSPs vs. TFSAs: What's better for your clients?

2. CI Direct Investing

CI Direct Investing provides financial advisors and their clients with convenient access to professionally managed portfolios and advanced digital trading tools. As a wholly owned subsidiary of CI Financial, one of Canada’s largest investment companies since 1965, CI Direct Investing mixes institutional-grade technology with a client-focused approach.

Investors benefit from low management fees and access to no trading fee options, helping them keep more of their investment working for them. Whether a client is investing $1,000 or $1 million, the service is designed to make investing accessible, affordable, and easy to manage.

3. Justwealth

Justwealth is another robo-advisor designed to offer financial advisors a wide selection of professionally managed investment solutions for their clients. Justwealth is registered as a portfolio manager in every province in Canada and operates under a fiduciary legal standard.

Unlike most bank-affiliated financial advisors, this fiduciary duty ensures client interests are always prioritized. Notably, its Education Target Date RESP is ideal for parents seeking automated education planning.

Client assets are protected by the Canadian Investor Protection Fund (CIPF) up to $1,000,000. Management fees are around 0.50 percent on average.

4. ModernAdvisor

ModernAdvisor is a digital investment platform designed for those who are already working with a financial planner. It offers a low-cost, professionally managed solution for clients who want part of their portfolio handled with expert care. Like JustWealth, it’s registered as a portfolio manager in all Canadian provinces.

ModernAdvisor also meets regulatory standards and partners with third-party custodians to safeguard assets. These custodians provide CIPF coverage.

Backed by Guardian Capital Group Limited, with over sixty years of institutional experience, ModernAdvisor offers both passive exchange-traded fund (ETF) portfolios and active strategies. Clients enjoy seamless, paperless onboarding and real-time access via mobile or web.

5. Nest Wealth

Nest Wealth is another digital investment platform that provides financial advisors with a customizable, low-cost solution for managing client portfolios. This robo-advisor uses passive ETFs and pooled funds, with underlying management expense ratios (MERs) ranging from 0.06 percent to 0.37 percent.

Rather than charging a percentage of AUM, Nest Wealth applies a flat monthly management fee per portfolio, ranging from $5 to $150 depending on services and account size. This transparent structure helps clients retain more of their investment growth.

Accounts are held with either National Bank Independent Network (NBIN) or Fidelity Clearing Canada (FCC), and additional custodial fees may apply for administrative services.

6. RBC InvestEase

RBC InvestEase simplifies investing by combining automation with professional oversight. This robo-advisor makes it easier for financial advisors to support investors with varying financial objectives.

Investors are guided through a short questionnaire to match them with a suitable low-cost portfolio of ETFs. They can choose between standard and responsible investing portfolios held in a:

- TFSA

- RRSP

- First Home Savings Account (FHSA)

- non-registered account

Portfolios are professionally monitored and rebalanced, with automatic investing starting at $100. RBC clients benefit from added banking perks and integrated platform access.

7. Qtrade Guided Portfolios

Investors wouldn’t need to monitor or manage Qtrade Guided Portfolios since it's a fully automated service. Clients begin by completing a goal-based questionnaire and are matched with a portfolio designed to meet their specific financial objectives.

Like other robo-advisors above, Qtrade’s available account types include TFSAs, RRSPs, and non-registered accounts. Portfolios are automatically rebalanced and monitored by a team of investment professionals. Clients can also benefit from easy onboarding, mobile and web access, and the ability to make deposits at any time.

8. Questwealth Portfolios

Questwealth Portfolios offers a low-cost managed investing solution for clients seeking market exposure without the high fees of mutual funds. Investors receive a professionally managed portfolio of ETFs, built and overseen by experienced portfolio managers. Portfolio options include:

- Growth: better than average asset growth, for medium to high-risk investors

- Balanced: for growth with a moderate level of risk, ideal for medium-risk investors

- Aggressive: maximum asset growth, for high-risk investors

Each of these strategies is created to cater to different risk levels and asset mixes. For example, the Growth portfolio holds 80 percent equity and 20 percent fixed income. The total fee for this portfolio is 0.37 percent, combining a 0.25 percent management fee and 0.12 percent in ETF costs.

9. Wealthsimple

Wealthsimple can provide managed investing solutions designed to grow with investors’ portfolios:

-

Core: for clients with at least $1 in assets; includes 0.5 percent management fees, commission-free stock trading, and 1.75 percent interest on chequing balances

-

Premium: for clients with $100,000 or more; offers 0.4 percent management fees, 2.25 percent interest, financial advice, and reduced trading fees

-

Generation: for clients with $500,000 or more; has all premium features, plus 0.2 to 0.4 percent management fees, 2.75 percent interest, and private financial advice

Access to private equity and private credit for accounts over $50,000 is also available.

10. Vanguard Digital Advisor

For our tenth robo-advisor, we have Vanguard Digital Advisor. It’s a managed investing service that builds fully personalized portfolios based on each client’s financial profile. The experience begins with a detailed risk assessment, taking up to 30 minutes to guarantee the right asset mix and glide path are in place.

Vanguard's robo-advisor automatically adjusts and rebalances to stay aligned with client objectives. Retirement is the default anchor goal, but clients can set other goals such as buying a car or funding education.

What exactly is a robo-advisor?

The word “robo” might imply that this would be an actual robot, but this is not the case.

Robo-advisors are software. These are digital platforms that use algorithms to build and manage investment portfolios by optimizing and automating passive indexing strategies.

For more perspective, watch this short clip about the nature of robo-advisors:

And here’s why, at the end of the day, robo-advisors aren't your competition.

What was the first robo-advisor?

The first robo-advisor was Betterment, the brainchild of 29-year-old Jon Stein, created in the United States in August 2008. The main inspiration for Betterment was to make it more convenient, straightforward, and simpler for people to invest even in small amounts.

Betterment’s creation was also partly inspired by the global financial crisis of that year, which would then be recorded as one of the six biggest market crashes in history.

How does a robo-advisor work?

A robo-advisor works by automatically configuring clients’ investment portfolios. Usually, robo-advisors build a portfolio with ETFs and index funds. So, instead of having individual investors research on which stocks and bonds to buy or sell, the robo-advisor does the work for them.

The process often starts when an investor opens an account with a robo-advisor and is presented with a questionnaire. From their answers, the robo-advisor determines their financial goals, risk tolerance, and investing preferences, then assembles portfolios based on this data.

The robo-advisor will usually recommend five to 10 choices for an investor’s portfolio, and they will have risk tolerances ranging from conservative to aggressive. While chosen portfolios are based on provided data, clients will usually be given the option to override those choices and make some of their own.

Robo-advisor fees

As for the fees, investors will have to pay the management expense ratios (MERs) on those funds, as well as the robo-advisor’s management fee.

A noteworthy feature of a robo-advisor is its automatic rebalancing. Let’s say an investor has a portfolio composed of 60 percent equities and 40 percent bonds and there’s an increase in equities. The robo-advisor will automatically adjust their portfolio to fit their risk profile.

Do millionaires use robo-advisors?

Yes, some millionaires do use robo-advisors, especially those who prefer low fees and automated investing. Wealthy individuals can use robo platforms as part of their portfolio while keeping larger or more complex assets with private advisors or wealth managers.

Robo-advisors can appeal to tech-savvy clients and high-net-worth individuals who value simplicity and efficiency. However, millionaires might still rely on personalized financial planning for estate, tax, and business matters.

Which Canadian robo-advisor has the best returns?

It depends. Robo-advisor returns vary by year, market conditions, and the investment portfolios offered. To know which robo-advisor yields the best returns, one must look at the risk level chosen (conservative vs. aggressive) and how long the funds are invested.

Always check up-to-date performance reports published by each platform or third-party review sites before making a recommendation to your clients.

Is it worth paying for a robo-advisor?

Yes, for many investors, paying for a robo-advisor can be worth it. Robo-advisors provide low-cost access to diversified portfolios and automatic rebalancing. Clients can also utilize it for goal-based planning.

While they lack personalized advice, some platforms offer hybrid services with human support. As for fees, robo-advisors will often charge between 0.5 percent to 0.8 percent of the amount invested by the client per year.

Overall, robo-advisors are ideal for people who don’t want to manage investments themselves but still want to grow their savings. They’re also best for those who are looking for assistance in investing but don't necessarily want or need full-service financial planning.

Read next: How much is the average financial advisor fee in Canada?

Stay updated on the latest news about robo-advisors and more on our Industry News page.