The mutual fund industry continues to hold a significant number of assets in Canada. WP examines eight funds and product suites that offer access to different classes and sectors

The growth of ETFs continues to dominate headlines, so it can sometimes be easy to forget just how large the Canadian mutual fund industry is. At the end of 2020, mutual funds accounted for $1.78 trillion of the total $2.04 trillion invested assets in Canada, according to the 2020 IFIC Investment Funds Report. And while new product development has slowed, there were still 3,459 total mutual funds at the end of the year – an impressive breadth of options available to Canadian investors.

Last year was the first one in the past decade when the total number of mutual funds decreased, and five firms pulled out of the mutual fund market altogether. However, IFIC attributed that decline largely to consolidation, pointing to the stronger competition in the industry, which ultimately benefits investors.

When it comes to the types of mutual funds investors are gravitating to, IFIC reports that balanced funds account for nearly 50% of total assets, followed by equity at 33% and bonds at 14%. And while ETFs have outsold mutual funds for the past three years, mutual fund gross sales have continued to trend upward. In 2020, mutual funds generated their largest ever gross sales at $300 billion.

With so many assets still invested in the mutual funds, WP wanted to focus on some of the products and solutions that are available. With more than 3,000 funds, it’s difficult to capture the entire industry, but over the next few pages, WP explores a few different areas where mutual funds are excelling and their benefits for both advisors and investors.

Taking managed solutions to the next level

With multiple options in its managed solutions suite, Canada Life is giving advisors more ways to meet clients’ evolving needs

Since 2008, investors have increasingly been turning to managed solutions. Allocations toward managed solutions grew from approximately 12% in 2009 to 25% in 2019, according to Investor Economics, and are expected to surpass 31% by 2028. It’s an area that Canada Life has taken note of, devel-oping multiple solutions that allow advisors to leverage the trend and find the best option for their clients.

“I think there are three main reasons [for this trend],” says Steve Fiorelli, SVP of wealth solutions at Canada Life. “One is the challenging market conditions. You simply aren’t going to get the big returns from an all-bond portfolio like you would 15 years ago. You need to diversify thoughtfully and cast a wider net when looking for return opportunities. You also have to put the right buffers in place so that client portfolios remain resilient.”

That means advisors must stay on top of constantly changing market dynamics – and managed solutions help take some of that burden off the advisor.

The second reason Fiorelli believes managed solutions have gained popularity is because they significantly improve business efficiency. By eliminating some of the administrative load associated with portfolio monitoring and rebalancing, it frees up time for advisors to focus on other value-added activities, such as holistic planning.

“[Managed solutions] are turnkey solutions that offer advisors simple, scalable ways to carry out portfolio construction and management responsibilities,” Fiorelli says.

The third area that has propelled managed solutions’ popularity is increasing regulatory expectations. With the incoming client-focused reforms, there is greater onus on advisors to understand and document the cost, risk and suitability of investment products that they recommend. Managed solutions can help reduce this burden in that they are often a simple, easy-to-understand investment solution that advisors can match to a client’s unique goals and risk tolerance, since most provide a spectrum of portfolios by risk level and growth potential.

To meet the needs of advisors, Canada Life has a full suite of managed solutions. The company aims to cater to the unique needs of each advisor and their client base.

“We offer straightforward balanced funds, target risk asset allocation funds, more sophisticated risk-managed strategies and our goals-based investing managed program, called Constellation, for advisors who want that immersive customizable experience for clients,” Fiorelli says.

Canada Life has recently expanded its balanced fund category to offer advisors even more choice. It launched five global balanced segregated funds in May 2020 and seven new mutual funds in September 2020.

The target risk asset allocation funds are single-ticket solutions designed to provide diversified portfolios focused on return within a target risk level. Available in conservative, moderate, balanced, advanced and aggressive options, they look for best-in class investment strategies and managers from around the world and combine them in a mix that aims to achieve strong, consistent returns.

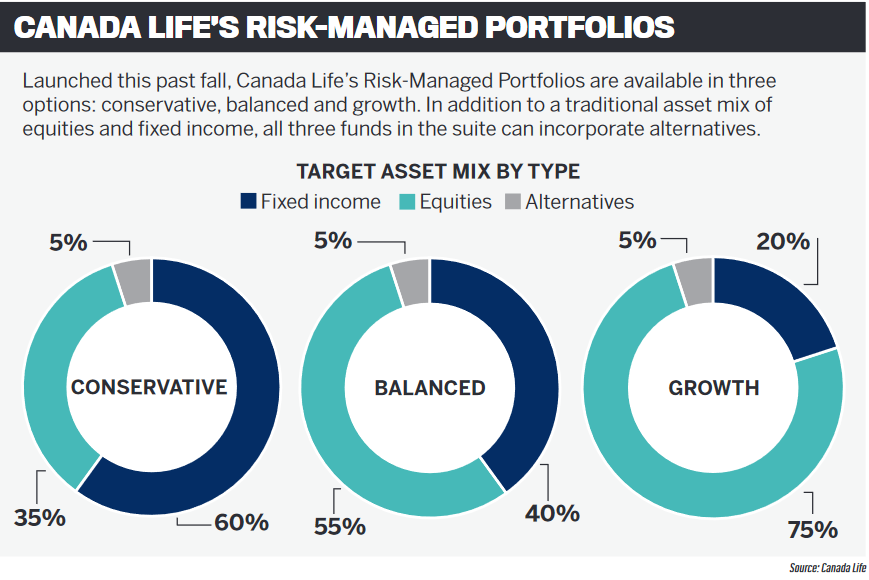

Canada Life’s three Risk-Managed Portfolios (conservative, balanced and growth), launched last fall, are similar to the target risk asset allocation funds; however, they bring together traditional and non-traditional investments.

“These have gained traction with advisors because they can offer clients more predictability and consistency in their portfolio,” Fiorelli says. “This is important to retirees and pre-retirees who have a shorter time horizon where they do not have the time to make up significant losses. The portfolios seek to mitigate risk without forgoing the upside returns.”

What makes Canada Life Risk-Managed Portfolios unique is that they go beyond the traditional diversification typically found within most balanced funds. They leverage four distinct risk-management levers. The first is a risk reduction pool that uses an option strategy, specifically puts and calls, to create an upper and lower limit to equity returns, helping to mitigate extreme equity volatility. The second lever uses lower-volatility equity mandates. The third, a global tactical equity solution, is designed to reduce equity exposure in response to market volatility. Finally, liquid alternatives seek to provide positive absolute return through uncorrelated sources of return.

What takes Canada Life’s offering to the next level is its Constellation Managed Portfolios – a goals-based managed investment program that provides advisors with a digital tool to select model portfolios and customize the investment fund mix to meet their clients’ unique financial goals.

When it comes to building managed solutions, Fiorelli says Canada Life starts with a client-first mentality. “We look at challenges that investors are facing currently (e.g. low yield environment), what challenges they might face in the future (e.g. continued volatility, potential for rising rates and threat of inflation), and we design solutions that help advisors address these issues for their clients.”

Next, Canada Life designs its managed solutions around risk-aware portfolio construction. “If you look at what we are facing today – uncertainty combined with low returns – it is hard for advisors to generate the returns clients expect,” Fiorelli says. “There are also expectations from clients to reduce losses. So, we thoughtfully engineered a risk-aware approach with growth potential.”

Fiorelli believes the time for managed solutions is now, and he feels Canada Life is ushering them to new heights, especially with Constellation.

“Digital capabilities are becoming increasingly important,” he says. “We have this interactive, goals-based investing digital interface for both advisors and investors, so advisors can give a first-rate experience to clients while also gaining efficiencies for their practice. We built our model portfolios in Constellation based on forward-looking capital market return assumptions and had them back-tested. We monitor these portfolios to ensure they continue to meet our return expectations. Advisors can select the right model portfolio that aligns with the client’s goals, time horizon and risk tolerance, and customize the underlying investment mix with a diverse selection of funds.”

Client portfolios in Constellation are monitored daily and rebalanced if an asset class deviates from its target weighting in the portfolio. This is an important process to ensure clients’ goals remain on track, Fiorelli notes.

“Our client portfolios are made up of taxable, tax-exempt and tax-deferred accounts,” he says. “Built into Constellation is a tax-efficient asset allocation strategy, known as asset location, that considers the different tax treatments on different investment income types and optimizes the allocation of assets within each account to help maximize after-tax returns.”

Through these features, Constellation helps advisors create a very disciplined approach to investment management – and it’s also a very efficient way for advisors to run their practice because it reduces some of the back-office support needs. The program’s digital goals-based approach, which Fiorelli believes is a true enabler of successful investment planning, gives clients greater visibility into their plans by allowing them to digitally track their progress toward goals.

“When we think about risk, we think about standard deviation of a portfolio, but risk should also be viewed as investors not reaching their goals,” he says. “It must be relatable, and the industry has lost that a bit. Risk is crucial in fund performance, but ultimately the most important measure of risk is not being able to pay bills or meet retirement needs. Constellation gives advisors a meaningful way to help clients visualize progress towards their goals and see the likelihood of reaching them, which can be way more important than any particular year’s return.”

A balanced approach to innovation

CIBC’s award-winning Global Technology Fund offsets single-sector risk by focusing equally on technology and healthcare

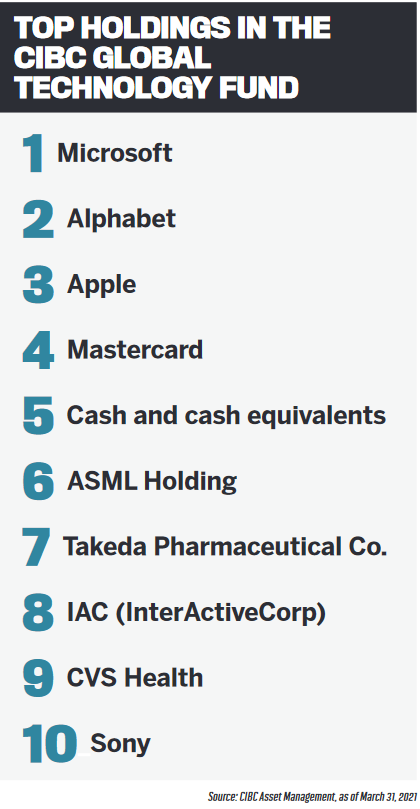

Technology and innovation have been key areas in the realm of thematic investing. While many investors want to gain exposure to the latest innovations, detractors are weary of the sector’s volatility. That’s why CIBC took a different approach with its Global Technology Fund, which invests in both healthcare (human genomics, genetic engineering and personalized medicine) and technology (AI, IT and communications). The combination has given the fund a strong risk/return profile, something similar funds don’t have.

“We are making a large bet that over the next couple decades, the world is going to continue to grow as a function of scientific and technological advancements in these fields,” says Michal Marszal, who manages the fund along with Jonathan Mzengeza. “That is where we specialize and the principal philosophy of the strategy.”

The duo essentially splits the portfolio management duties: Marszal focuses on healthcare and Mzengeza on technology. Both have a background in those fields, and that expertise is something they believe sets them apart.

“In these sectors, people really don’t appreciate the lethality of ignorance,” Marszal says. “Either you have the expertise or not.”

The fund holds approximately 30 names at a given time. It’s currently slanted towards technology, given overall market trends. Marszal and Mzengeza start with more than 500 stocks in the universe and whittle them down using their own screens, including quality, return on invested capital and volatility. Both PMs know the companies thoroughly, which helps them make their core selections. While most of the names do appear in the benchmark, they’re not afraid to go outside it, especially when it comes to the fund’s tactical allocation, which is usually composed of small and mid-cap names still in their development phase. Those companies usually hold three to five positions in the portfolio.

The strategy behind the CIBC Global Technology Fund is driven by three main investment principles. The first is risk management, something Marszal believes is a true differentiator.

“We’ve had a steady progression on performance in all periods,” he says. “That is largely due to the risk management process we implement. It is really 90% of what we do. We use it for core position sizing, analysis, stress testing scenarios and to figure out the downside.”

“We’ve had a steady progression on performance in all periods,” he says. “That is largely due to the risk management process we implement. It is really 90% of what we do. We use it for core position sizing, analysis, stress testing scenarios and to figure out the downside.”

The second pillar is long-term investing. Marszal notes that the fund’s core positions are typically owned for five to 10 years, and even its tactical positions will be held for 12 to 18 months.

Finally, Marszal points to the team’s expertise, which helps to identify and avoid any risks – the overarching one, Marszal says, is security risk of underperformance in one of the sectors. In healthcare, he highlights potential concerns such as demand for services, drug pricing and reforms that can ripple beyond pharmaceuticals to impact research and development. On the tech side, Mzengeza keeps an eye on the geopolitical landscape, trade tensions, intellectual property, conflicts, regulations, political backlash, cybersecurity and privacy. Yet because the two sectors are not correlated, even if a risk materializes in one, the other side of the fund can help it weather the storm.

Ultimately, both Marszal and Mzengeza see the fund as a great complement for Canadian investors looking for exposure to these themes.

“We are trying to provide Canadians with a breadth of investment opportunities with equities,” Marszal says. “What we are trying to do is tap in and extract opportunities on the innovation angle of these strategies. We try to provide a custom-made solution where investors can make a bet on innovation-driven industries outperforming broadly diversified assets and [have] this be their thematic exposure.”

The stability of short-term bonds

Franklin Templeton’s Franklin Bissett Short Duration Bond Fund looks to leverage the steadiness of the short-term bond market to help investors with fixed income exposure

The search for yield has never been greater – and it’s pushed many investors up the risk spectrum. Yet those who still want fixed income exposure to protect capital aren’t looking at traditional offerings the same way, which has forced asset managers to create innovative ways to offer fixed income exposure.

That’s exactly what Franklin Templeton is aiming to do with its Franklin Bissett Short Duration Bond Fund. The fund is similar to the Franklin Bissett Core Plus Bond Fund and Franklin Bissett Corporate Bond Fund, but it only looks at bonds with a maximum duration of five or six years. Seventy-one percent of the fund is allocated to corporate bonds, 15% to federal and 14% to provincial bonds.

“We tend to be heavy corporate versus the index because we perceive the spread between corporate and government bonds to offer a bit of cushion,” says Adrienne Young, director of credit research at Franklin Templeton Canada. “So, in a volatile interest rate environment, where federal bonds get slaughtered when central banks increase short rates or because the market worries about inflation and long rates rise, we have a cushion to help reduce the blow.”

Young adds that when it comes to corporate bond selection, the team leverages the expertise of Franklin Templeton’s fundamental corporate credit analysts, which has generally led to outperformance versus the index.

“We think in a tight market, you have to be picky, and we are very careful about credit quality,” she says. “We believe in in-house fundamental credit analysis to identify where there is value. So that is a pitch for active versus passive and looking under the hood.”

That’s just one of the capabilities Franklin Templeton provides; Young believes there are additional factors that help make the fund unique.

“Because we are big enough to have our own loan group in San Mateo, California – whereas loans don’t trade in the secondary market in Canada – we have loans in the fund,” she says. “That helps to give us some diversification. We can invest in high-yield credit in the US, which we prefer because US high-yield is more liquid than the Canadian market.

“We are also able to take advantage of quants that work in Franklin Templeton to spot opportunities in derivatives markets, so we buy currency derivatives. We also use interest rate derivatives. Rather than buying and selling bonds in order to get our duration down by half a year versus the index, we’ll manage that with interest rate swaps. Rather than selling bonds we like and know we can’t get back easily, we buy credit default swaps. It allows us to manage our credit exposure without having to sell the bonds we may be unwilling to sell.”

Young acknowledges that a short-term fund like this might not offer the high returns many clients are looking for, but it will provide stability. The Franklin Bissett Short Duration Bond Fund has historically provided more of a return than the index, money market funds and the Canadian Short Term Bond Index, with less volatility because of its shorter duration and added diversification.

“I think in a slightly inflationary world,” Young says, “people looking for something that will preserve capital should find that attractive.”

Why short-duration bonds now?

Adrienne Young offers a simple analogy to illustrate why advisors and investors need short-duration bond exposure now.

“I think of duration as a diving board, anchored at one end, springy at the other,” she says. “If rates rise, the short end is somewhat anchored, and the long end is where you see the most volatility. You are going to see the most volatility in government bonds, and you will have a little cushion in corporate with the spread from governments, so you’ll have a little less risk. This kind of portfolio, which includes both corporate and government bonds and is at the short end of the curve, is a little more protective.

Exposure to the ‘good life’

The staples in the RBC European Equity Fund offer exposure to many of the continent’s storied lifestyle brands

In recent years, many advisors have looked to diversify their portfolios by going global, but one area that sometimes gets overlooked is Europe. However, the opportunities on the continent are unlike what investors will find in North America or in emerging markets. From luxury items like clothing and alcohol to consumer staples and pharmaceuticals, plus areas with quality intellectual property like engineering and health sciences, European companies can be a unique addition to portfolios.

RBC Global Asset Management’s European Equity Fund dates back to 1987 and is managed by a team in London. It looks at investments in continental Europe and the UK and has growth mandate.

“More realistically, we are more interested in total return,” says Dominic Wallington, senior portfolio manager and head of European equities at RBC Global Asset Management in the UK. “Europe has a culture of paying and growing dividends on real bases, higher than inflation.”

The fund aims to invest in companies with high, stable returns, targeting those that show high levels of return on invested capital.

“We like companies that have low levels of capital intensity,” Wallington says. “The companies we invest in tend to be less expensive to grow the top line. Many of them turn over their assets many more times on an annual basis. The reason we like these businesses is the cash conversion is higher and can be returned to shareholders or directed towards growing the business.”

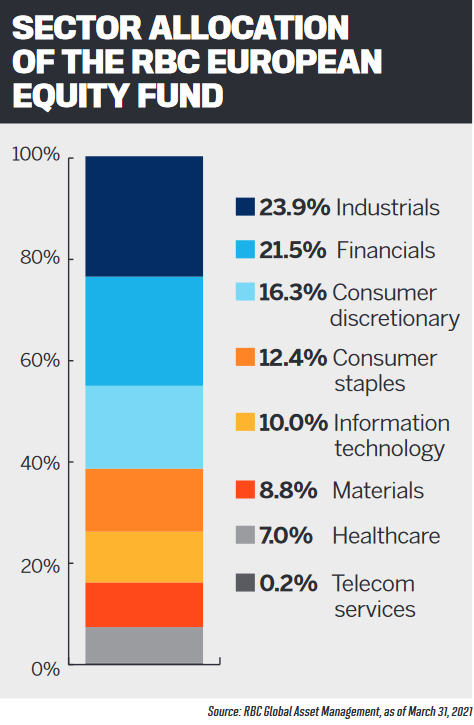

The companies that tend to fit the bill are usually ones with established brands, something Wallington says RBC GAM looks for. The fund’s 51 holdings include staples like alcohol, spirits, brewers, food companies and businesses with high-quality, sustainable intellectual property. Many of those staples are classified as luxury items, an area the fund targets.

“The total luxury market is $1.4 trillion, and we believe it is a very important and a highly profitable industry,” Wallington says. “Scale and voice are important to keep brands in front of people, so we still see opportunity in luxury. Europe is still top of the list in soft power – use of attraction or persuasion – promoting the idea of the good life.”

Wallington believes Europe is leading the way in and commercializing soft power, which is one of the opportunities he sees in a European fund.

Wallington believes Europe is leading the way in and commercializing soft power, which is one of the opportunities he sees in a European fund.

“There are pockets of companies all around Europe that we like to focus on,” he says. “We believe there are some great opportunities with intellectual property. One of the best semiconductor companies is based in Holland. In Denmark, there are great health sciences companies. Those different pockets are why I think the fund should be in portfolios.”

Wallington notes that the fund deviates from the index, as RBC GAM believes the companies it selects will outperform over the long term. While the team has many processes in place to mitigate risk, investors do need to be aware that the fund can underperform during certain periods. Still, Wallington believes this approach will do better over the long term.

Another potential area of concern for investors is the impact European politics can have on the fund. Wallington acknowledges the issue but notes that it can also provide discount valuations.

“I think there are issues everywhere in the Western world, so I’m not sure how different Europe is,” he says. “What background politics does is allow for discount valuations compared to companies situated in, say, the US.”

An option for US mid-cap stocks

A bottom-up ethos, informed by secular trends, has fuelled the success of Mackenzie Investments’ US Mid-Cap Opportunities Fund

For the average fund manager, keeping up with the companies in their portfolio means listening to earnings calls, reading analyst reports, analyzing financial statements and poring over regulatory filings. But when Sonny Aggarwal, vice-president and portfolio manager within Mackenzie Investments’ Growth Team, says he and his fellow portfolio managers are familiar with the companies they invest in, he means it on a whole other level.“

One great thing about being a portfolio manager in the mid-cap space is you have good access to the C-level management teams of your portfolio companies,” Aggarwal says. “I can speak with the CEOs of most of our companies to talk strategy – what they’re looking at, what they’re trying to do and what their outlook is three or five years down the road.”

Being on a first-name basis with CEOs of portfolio companies has enabled the Growth Team to get deep qualitative information to reinforce or counterbalance financial data and models. That’s just one of several capabilities underpinning the Mackenzie US Mid-Cap Opportunities Fund, which draws from the approach of Mackenzie’s US Small- to Mid-Cap Growth Fund.

The US Mid-Cap Opportunities Fund has enjoyed considerable success since its launch a year ago. According to Aggarwal, it crossed the billion-dollar AUM mark in April, and it has been consistently in the top five of sales across all of Mackenzie’s retail funds since the beginning of 2021.

Its performance has been remarkable, too. Since its debut, the US Mid-Cap Opportunities Fund has achieved a 56% return, compared to 40% for the S&P 500 and 53% for the overall US mid-cap space. Over the past 15 years, Aggarwal notes, US mid-caps have outperformed both the S&P 500 and the small-cap index, reinforcing the notion that mid-cap stocks are a desirable “sweet spot” in the world of equities.

Its performance has been remarkable, too. Since its debut, the US Mid-Cap Opportunities Fund has achieved a 56% return, compared to 40% for the S&P 500 and 53% for the overall US mid-cap space. Over the past 15 years, Aggarwal notes, US mid-caps have outperformed both the S&P 500 and the small-cap index, reinforcing the notion that mid-cap stocks are a desirable “sweet spot” in the world of equities.

“You see on one end of the spectrum, people invest in large-caps because they want established companies with diversified business lines,” he says. “But a lot of the time, ‘diversified business lines’ is code for mature companies with slow growth. On the other end of the spectrum, people invest in small-caps because they want that fast-growth, home-run type of scenario. But just like buying lottery tickets, it could be a very risky investment strategy.”

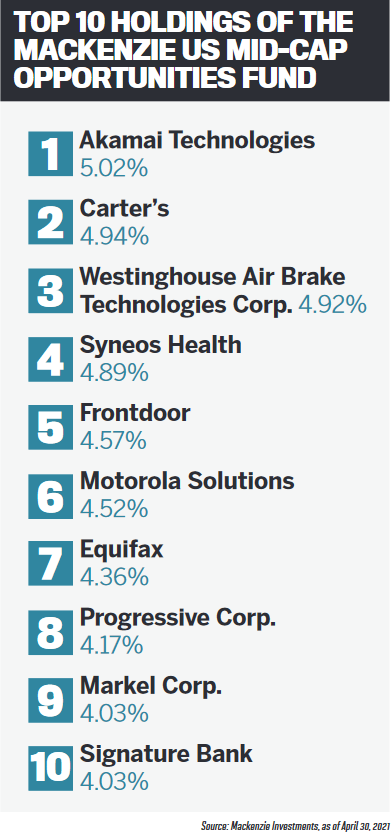

From where the Mackenzie Growth Team sits, mid-caps possess the best of both worlds: growth profiles akin to small-caps, but with more of the stability of large-cap stocks. That belief has translated into a high-conviction portfolio of between 30 and 35 names, which has been built through a well-considered bottom-up approach. Aggarwal says his team looks for companies with strong prospects of sustainable growth, typically driven by large secular themes. To create an all-weather portfolio, they have identified 10 secular themes that well-positioned companies can benefit from not just over the next year, but also for the next three, five or 10 years.

“One sector that we went overweight on initially was financials, which did struggle for the better part of last year while the NASDAQ reached all-time highs from tech valuations going to the moon,” Aggarwal says. “But we believed the financial sector and other cyclicals would have their time in the sun as the economy rebounded. We held on to financial companies that had a really good credit track record, and it’s paid off nicely over the past three to six months.”

A unique approach to Canadian exposure

Invesco is using its global capabilities to add another dimension to its Premier Canadian Balanced Fund

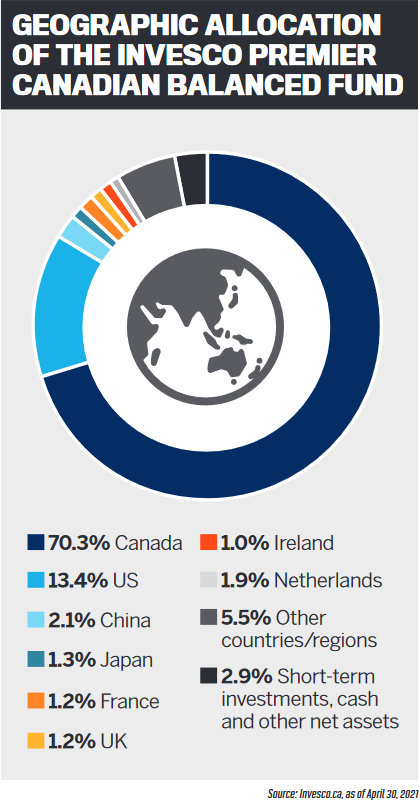

It's no secret that Canadians tend to have a home bias when investing, and their portfolios tend to be made up of the country’s most prominent industries, such as financials and energy. Canadian balanced funds feature many of these same industries, but they do have other exposures. While many look to familiar areas like the US for additional exposure, Invesco has taken a different approach with its Premier Canadian Balanced Fund, which targets international exposures in both equities and fixed income.

“The strategy falls under the Canadian neutral balanced fund category,” says Avi Hooper, portfolio manager for Invesco Fixed Income. “There will always be 60% equity and 40% fixed income. As markets move, we’ll adjust monthly.”

Richard Nield, senior portfolio manager at Invesco, adds that “the premise was a growth mandate on the equity side that invested in long-term quality compounders, and having Canadian and foreign equities. We have a little more foreign equities than our peers and not as much tilted to the US. We have a dedicated US team but look at Europe and Asia so we don’t put all our eggs in one basket.”

The result is that the fund can have up to 30% international exposure. Both Hooper and Nield use their expertise in that area to bring global opportunities to the fund.

When it comes to selecting securities on the equity side, Nield says the team looks for growth but also cares about valuations. “We look for growth companies, but not the fastest-growing growth companies. We look for sustainable growth,” he explains. “We are happy to find businesses that can grow their earnings 10% to 15% per year.”

On the fixed income side, Hooper says the team combines “macroeconomic broad themes with our credit research. Our best ideas, from the bottom up, are integrated in the portfolio.”

On the fixed income side, Hooper says the team combines “macroeconomic broad themes with our credit research. Our best ideas, from the bottom up, are integrated in the portfolio.”

Despite the fund’s international spin, both Nield and Hooper see opportunities in Canada. “We look at Canada as very attractive at this point,” Nield says. “When we look at Canada, with vaccination rollout, having just gone through the pandemic, GDP is roaring back, and there is still a lot of stimulus. I think that bodes well for Canada. There is opportunity on the industrials side, financials are still a key contributor, and a good way to approach commodities is some of those energy names tilted to natural gas.”

Hooper shares that positive outlook on the fixed income side. Right now, the fund is overweight toward corporate credit and underexposed to government debt. One of the reasons why is that banks and large insurance companies have offered subordinated debt, a higher-yielding hybrid structure.

“The accommodating monetary policy leans to overweighting corporate debt,” Hooper explains. “Canada’s banking sector is incredibly strong; the banks have issued subordinated debt. It’s a great opportunity for us to enhance yield [and] reduce interest rate sensitivity, focusing more on the credit risk sensitivity with the highest-quality companies in Canada.”

Because the fund gives investors a bit of everything, Invesco considers it a core product. While the international exposure makes it unique, Nield notes that the importance placed on valuations and the bottom-up construction are also key differentiators that make it less risky than similar funds.

“Investors seem to like the one-stop shop,” Hooper says. “At a high level, it has equity and fixed income allocations but is very diversified across sectors and globally. Even though we are finding opportunities here, it’s how we leverage our global research team and take advantage of those capabilities. I see it playing an important role, and I value our approach of being global in our thought process.”

Taking advantage of real estate trends

Middlefield’s established Global Real Estate Class Fund has capitalized on subsectors that were disproportionately hit by COVID-19, leading to an award-winning result

The COVID-19 pandemic has made for an interesting time in real estate investing. Some subsectors, like e-commerce, have taken off, while others were hit hard. Yet those battered subsectors have presented opportunities for the team at Middlefield to buy in areas they felt were unjustly punished. That reallocation led to success in the form of a 2020 Lipper Award for the Middlefield Global Real Estate Class Fund.

“It is a diversified real estate fund,” explains Dean Orrico, president and CIO at Middlefield. “Within real estate, you have sectors that have behaved very differently over the past 12 to 18 months. Several years ago, we decided to target one area that we thought would go through a multi-year run of growth: e-commerce REITs.”

While the fund’s exposure to e-commerce has helped make it successful, Middlefield’s decision to pivot its approach is what kept the fund strong during the pandemic.

“We looked at those sectors that were left behind and thought it presented an attractive opportunity to invest in some of those companies,” Orrico says. “We rotated out of some of those e-commerce names – we didn’t sell them, but reduced their weight – and then invested in some of the areas that were left behind, mainly multi-family, brick-and-mortar retail and select office REITs.”

There were very specific reasons why Middlefield thought those areas represented good opportunities, Orrico says. In brick-and-mortar retail, an area hit hard by the rise of e-commerce, Orrico says there are still opportunities in open-air retail, especially anchored by needs-based stores like groceries.

“We still think they have a lot of runway,” he says, “because they are trading at a valuation that is below where they were historically and at a discount to retail REITs in the US.”

Another area where Orrico sees opportunity is the multi-family subsector. The transition to working from home didn’t correlate to people leaving the cities to purchase suburban houses because home prices are still high, he points out. He also feels that when Canada resumes immigration, with the government targeting 400,000 new arrivals per year, the demand for rentals will remain elevated.

Finally, Middlefield is looking at select opportunities in the office space. While Orrico sees a future hybrid work environment split between home and the office, he believes many people will return to offices. One area Middlefield is targeting is purpose-built office, which is more common in the US, but Orrico says the team likes companies focused on specific niches.

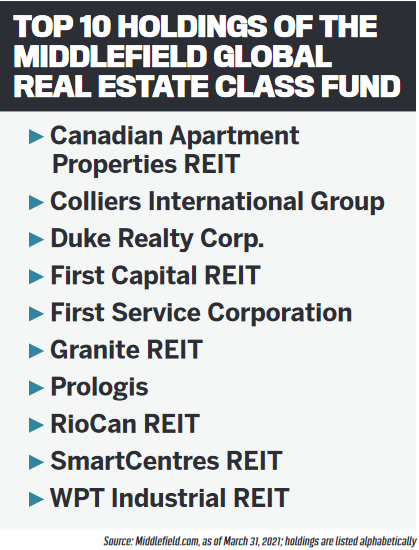

He notes that the Middlefield Global Real Estate Class Fund can invest in any real estate subsectors and, because of its global nature, is not tied to one country; the current breakdown is roughly 50% Canada, 40% US and 10% international. While e-commerce REITs still hold a strong position in the fund (35% to 40%), it is well diversified across many subsectors, including retail REITs/open-air shopping centres (15% to 20%), multi-family REITs (15% to 20%), office REITs (5%), real estate services (10%), and healthcare REITs and other (10%).

He notes that the Middlefield Global Real Estate Class Fund can invest in any real estate subsectors and, because of its global nature, is not tied to one country; the current breakdown is roughly 50% Canada, 40% US and 10% international. While e-commerce REITs still hold a strong position in the fund (35% to 40%), it is well diversified across many subsectors, including retail REITs/open-air shopping centres (15% to 20%), multi-family REITs (15% to 20%), office REITs (5%), real estate services (10%), and healthcare REITs and other (10%).

“Generally speaking, we are focused on larger-cap issuers – we tend to stay away from smaller-cap names because you can have a liquidity issue,” Orrico says. “We tend to be value-oriented, but I describe it as growth at a reasonable price – we like to see companies that can grow revenue streams, but we don’t really want to pay up for them.”

He notes that Middlefield also looks to identify companies focused on specific areas and that the quality and the track record of managers goes a long way in determining where capital is allocated.

When it comes to real estate’s position in portfolios, Orrico believes all investors should have exposure to it.

“It makes sense as part of a core component because real estate does well in various economic cycles,” he explains. “It does well when interest rates go down because there is more cash flow available to pay dividends or upgrade properties. However, if you look back over 30 to 40 years, it does well in inflationary environments because if you have lease renewals in the portfolio and the economy is doing well, you can renew leases at higher levels, so it has become a good hedge against inflation as well.”

Concentrating on emerging markets

Fidelity Investments’ Emerging Markets Fund limits exposure to sectors, countries and individual stocks to give investors a diversified solution

Fidelity Investments’ Emerging Markets Fund limits exposure to sectors, countries and individual stocks to give investors a diversified solution

Between the pandemic and a strong US dollar, emerging markets have had a tough time lately, but it’s an area where Fidelity Investments sees opportunity on the horizon.

“The EM opportunity is exciting today,” says portfolio manager Sam Polyak. “EMs have had a tough time in general relative to developed markets. When the dollar is strong, EM currencies are weak; it leads to inflation, and these countries raise interest rates, which hurts consumption and growth. Because of that, you have a lot of pent-up demand that I think will dissipate.”

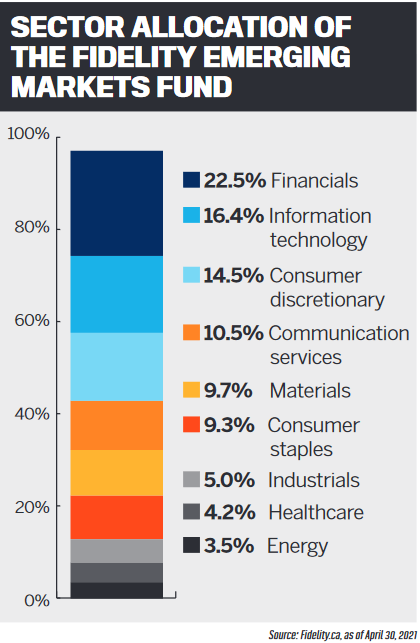

Polyak is analyzing areas that will benefit and getting those exposures into the Fidelity Emerging Markets Fund. While many EM funds are index-focused, Polyak takes a concentrated approach, focusing on 40 to 50 stocks, then adding a layer of protection to ensure the fund isn’t overexposed to one area.

“We have these guardrails in place that make it unique,” he says. “As such, the fund will not be more than 5% overweight or underweight a sector, 10% for a country and 5% of the benchmark weight for an individual stock. It keeps the volatility down. From a risk perspective, the fund will not blow up if one area significantly underperforms. It has, therefore, been able to deliver in up and down markets, growth and value cycles, and been consistent because the focus is the individual stocks.”

Fidelity’s experience with emerging markets goes back more than a decade when it rebuilt its approach. Today, a seasoned team focuses on stock selection and returns, not just individual themes. Polyak notes that the team is looking for companies that will continue to grow for years to come.

A few of Fidelity’s capabilities help add to he fund’s uniqueness. The first is its corporate governance team, which looks at balance sheets and income statements for aggressive accounting, but also at the people behind the companies. The second is Fidelity’s geopolitical analyst, a former CIA agent who helps the team understand geopolitical relationships so they are not caught off guard by an event.

When selecting stocks, Polyak says his philosophy is growth at a reasonable price, and he looks for companies that have a great product, consumer demand and are run by a management team with a good track record. “

The other thing I do is not mess with cash or developed market stocks,” he says. “I try to stay under 2% cash. As for developed market stocks, other funds may sometimes benefit by owning US tech stocks in an EM fund, for example, but I try to provide my investors pure EM exposure.”

Right now, Polyak is focusing on a few themes in emerging markets, including automation, local brands taking market share, innovation, e-commerce and infrastructure. While he has historically liked China, he is now looking at areas that have been hit hardest by the pandemic, such as Latin America and India, as he believes they will begin to grow at a faster rate during the rest of 2021 and into 2022.

“I think advisors who consider buying into EMs should look at active managers – they have outperformed through time because of two reasons,” Polyak says. “One, EMs have a big proportion of state-owned enterprises that often have the interests of the population and not minority investors in mind. The other area is corporate governance. An index buys a company because it is big, but they don’t care if the people running the company have other personal interests in mind. Those reasons are why I think active does well.”