Sponsored by CI Global Asset Management

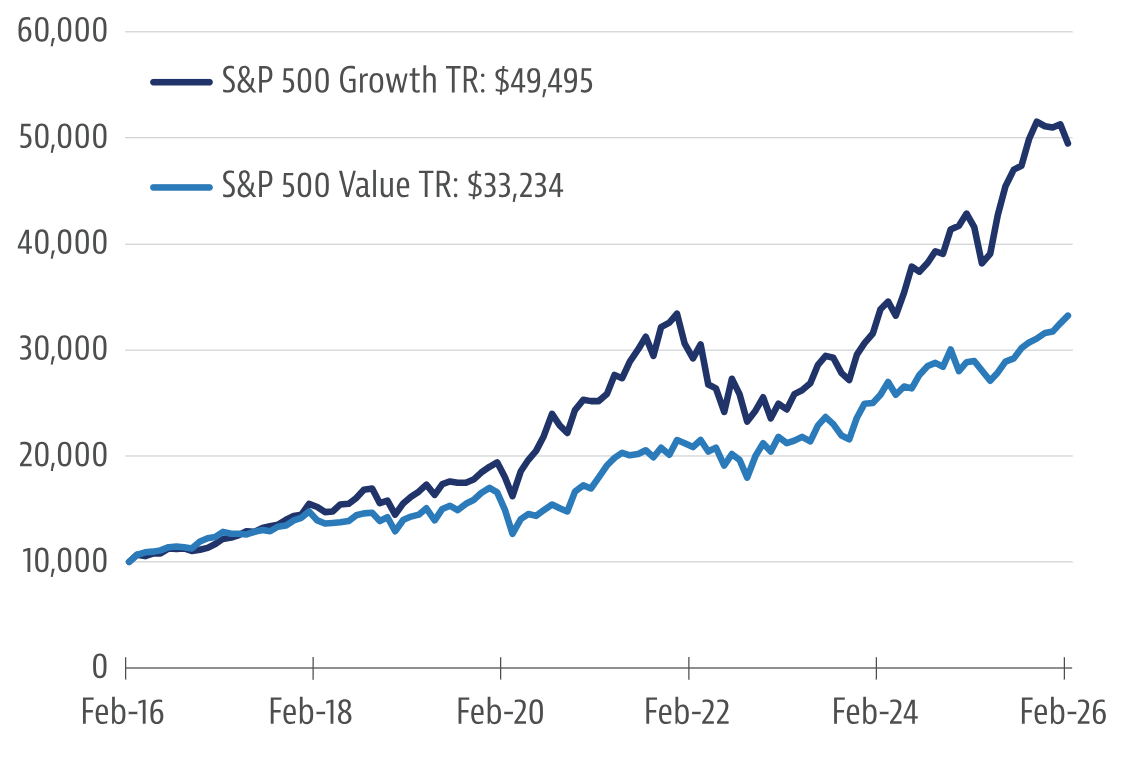

Advisors working with diversified portfolios often face a familiar imbalance. In some portfolios, asset allocations can shift over time, with increased exposure to U.S. equities, including large‑cap growth stocks.

That positioning has worked well in recent years, but it also introduces concentration risk tied to a relatively narrow set of sectors and valuation assumptions.

International equities can help address that imbalance. Within that universe, value-oriented strategies have drawn renewed interest as investors reassess valuations, earnings expectations and the role of diversification in portfolio construction.

CI Morningstar International Value Index ETF (VXM) sits at the intersection of those trends. It is an international equity ETF that focuses on developed markets outside North America, with exposure across Asia and parts of Europe.

The strategy targets companies trading at lower valuations while showing signs of improving earnings, offering a structured approach to international value investing.

International equities and factor leadership across regions

For advisors, factor exposure does not operate in a vacuum. Growth and value tend to express themselves differently depending on the region.

In the U.S., market leadership has been driven largely by growth-oriented sectors such as technology and consumer discretionary. These sectors benefit from scale, network effects and higher earnings reinvestment, which has supported persistent outperformance over the past decade.

S&P 500 EAFE GROWTH VS VALUE

Source: Morningstar Direct, as at February 28, 2026.

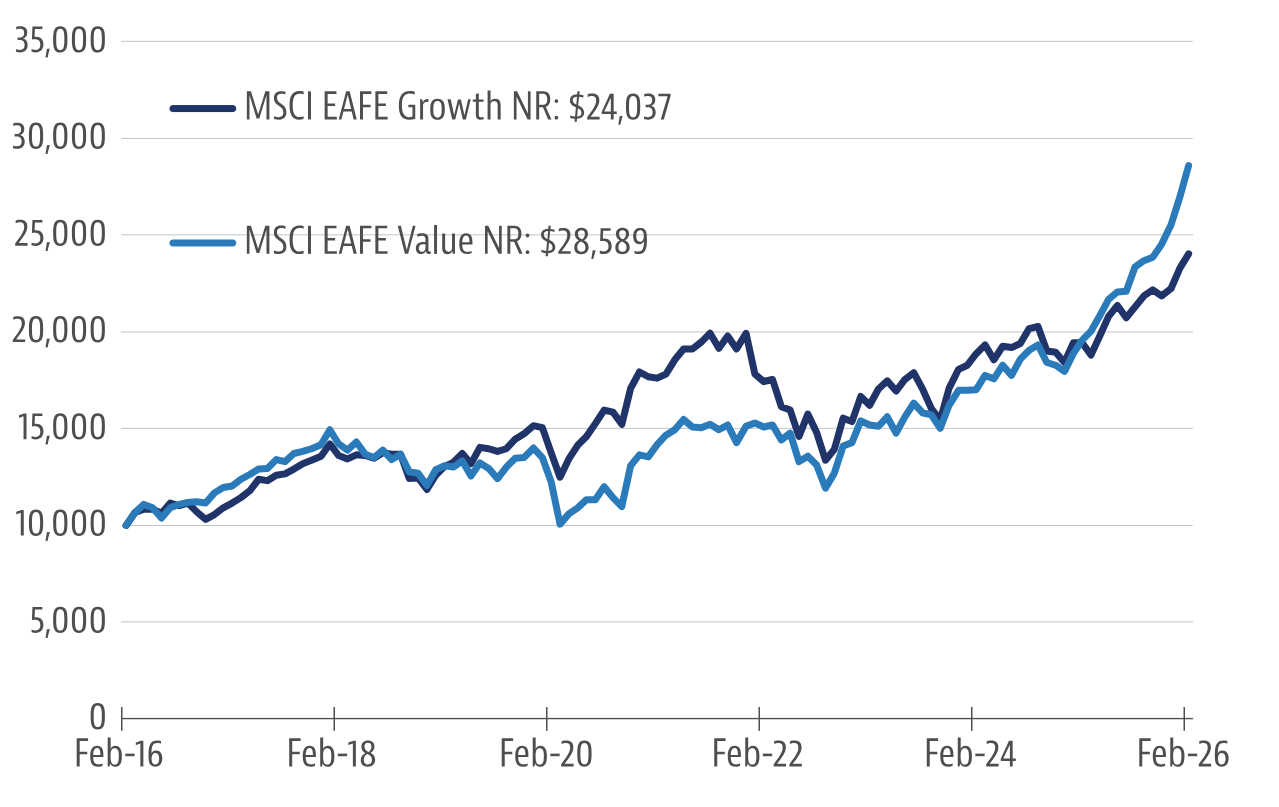

By contrast, developed international markets such as those captured in the MSCI EAFE Index have a very different composition. Financials, industrials and healthcare play a much larger role, and these sectors have historically aligned more closely with value-style characteristics.

MSCI EAFE GROWTH VS VALUE

Source: Morningstar Direct, as at February 28, 2026.

That structural difference helps explain why value has been more effective outside the U.S. Over longer periods, value has outperformed growth across international markets, particularly in Europe and Asia.

For advisors allocating to an international equity ETF, this creates a case for being deliberate about factor exposure rather than defaulting to broad market cap-weighted approaches.

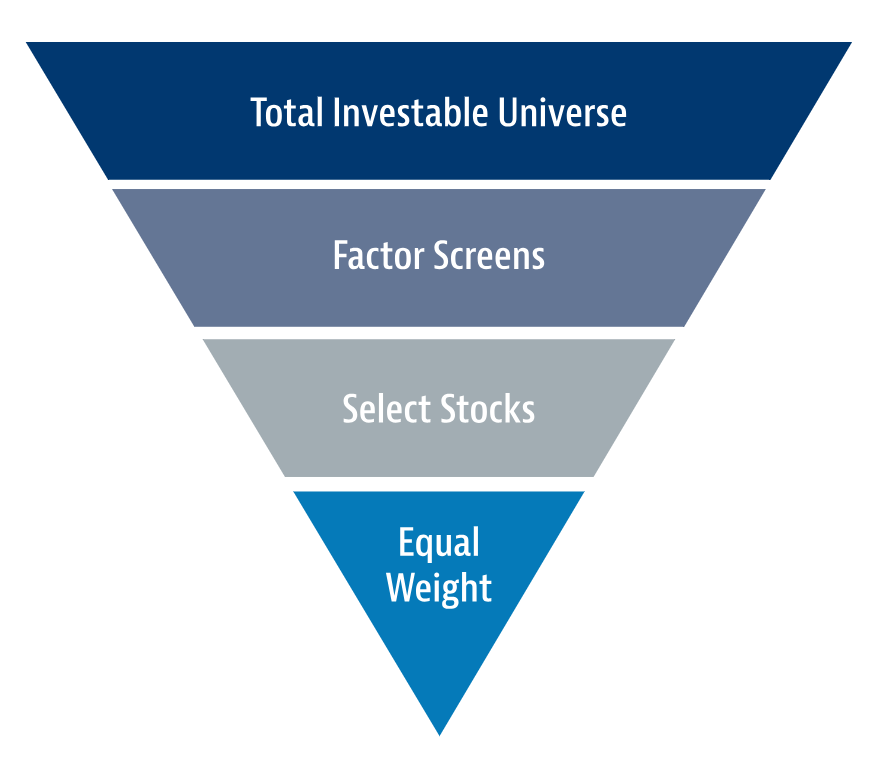

A rules-based approach to international value investing

VXM is built on Morningstar’s Target Value Index methodology. This benchmark uses a disciplined scoring system that blends traditional valuation metrics with forward-looking earnings signals:

- Price-to-earnings (20%): Compares a company’s share price to its trailing 12-month earnings. Lower ratios indicate more attractive valuations.

- Price-to-cash flow (20%): Measures price relative to operating cash flow over the past four quarters. Lower values are preferred.

- Price-to-book (20%): Evaluates market price against the accounting value of equity. Lower ratios suggest cheaper valuations.

- Price-to-sales (20%): Compares price to revenue over the last four quarters. Lower values indicate lower valuation relative to sales.

- Three-month earnings estimate revisions (20%): Tracks changes in forward-looking analyst earnings forecasts over the past three months. Higher revisions signal improving fundamentals.

Each component is equally weighted, resulting in a balanced approach that combines valuation discipline with momentum in earnings expectations. This also reduces concentration in large-cap names and introduces a size tilt, which has historically been associated with different return drivers than traditional market cap-weighted indices.

VXM’s methodology combines traditional valuation metrics such as price-to-earnings, price-to-book and price-to-sales with forward-looking earnings revisions. This helps avoid allocating to companies that appear inexpensive but lack improving fundamentals (“value traps”).

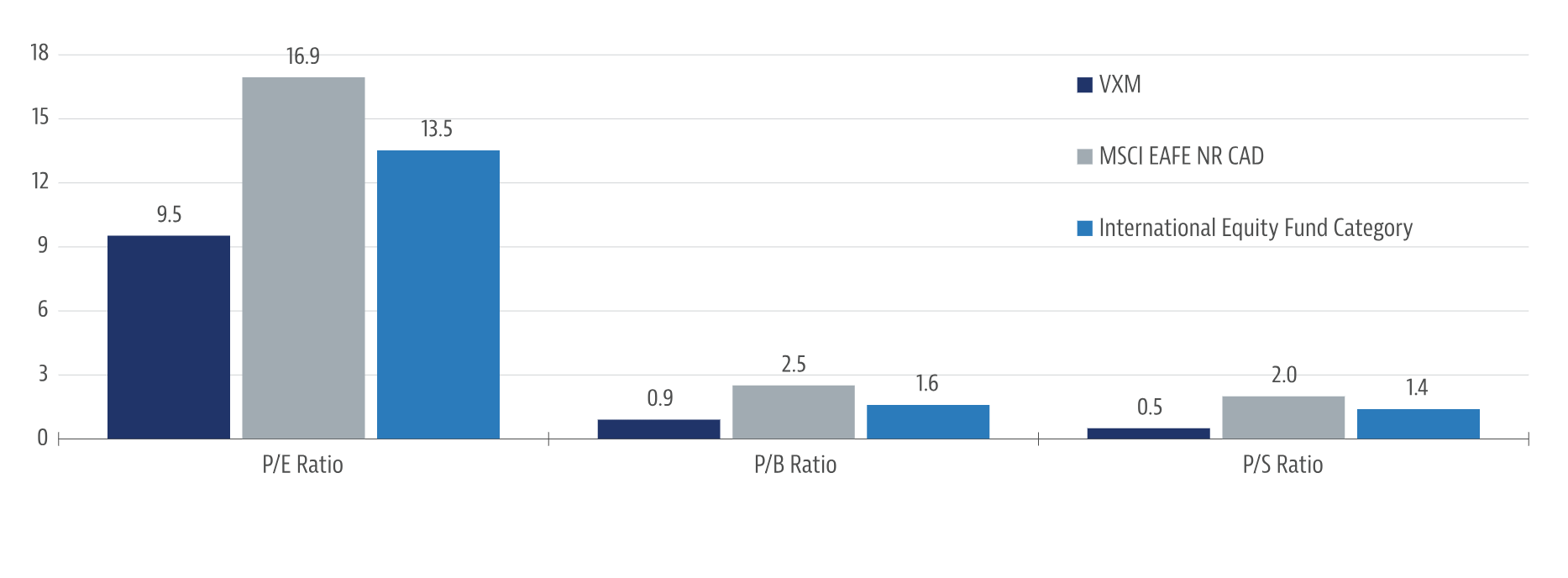

As a result, the portfolio has historically screened at lower valuation multiples than both the MSCI EAFE benchmark and the broader international equity fund category, based on Morningstar data. This positioning reflects a more selective approach to value investing, with an emphasis on companies where earnings expectations are trending upward.

VALUATION METRICS

Source: Morningstar Direct, as at February 28, 2026.

Finally, the benchmark’s equal-weighted methodology reduces concentration in large-cap names and introduces a size tilt, which has historically been associated with different return drivers than traditional market cap-weighted indices.

The result is a meaningful allocation to mid- and smaller-cap companies, while sector weights differ from traditional benchmarks. This combination has contributed to differentiated performance characteristics.

Using an international value ETF to support portfolio diversification

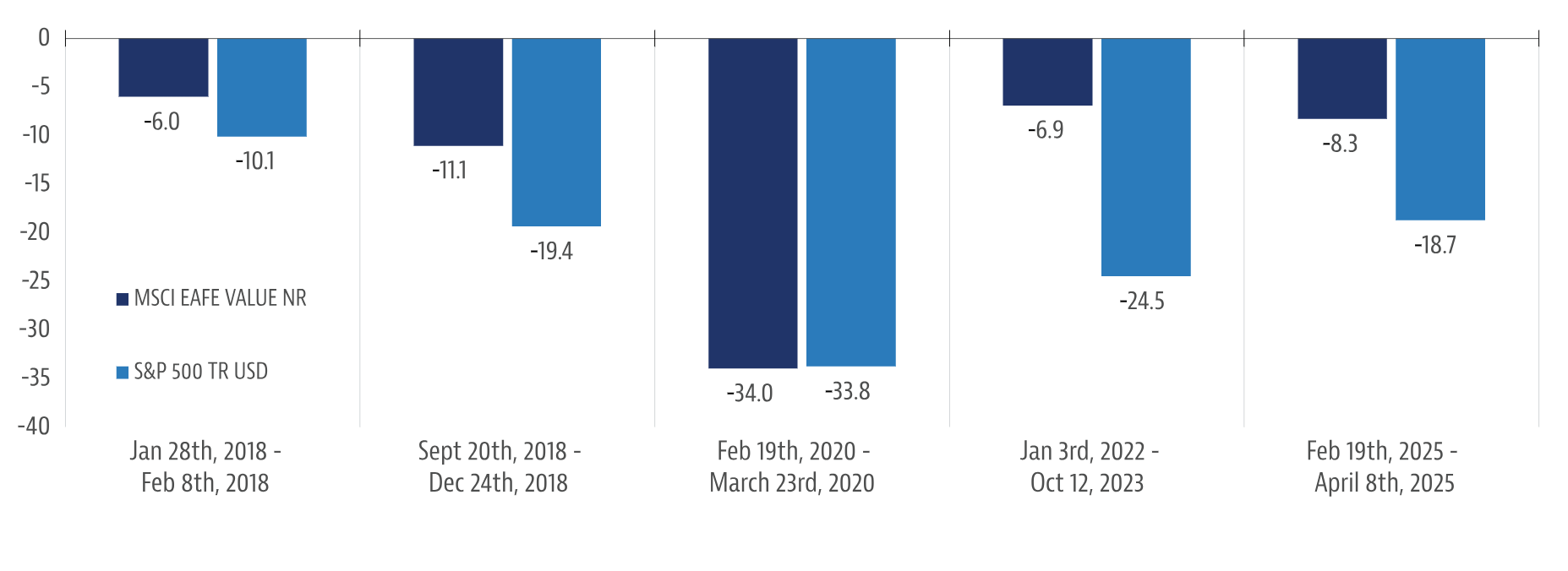

During periods of market stress, international value benchmarks such as the MSCI EAFE Value Index have historically exhibited different behaviour across regions and factors. During recent S&P 500 drawdowns of 10% or more, this differentiation has been observable. For advisors focused on diversification, volatility awareness, and drawdown management, such patterns can support a more balanced allocation across regions and factors.

LAST 5 DRAWDOWNS OF 10% OF THE S&P 500

Source: Morningstar Direct, as at February 28, 2026.

The case for VXM is less about replacing existing exposures and more about complementing them. Within a broader allocation that may already include U.S.-focused strategies, an international ETF with a value tilt can provide a different set of return drivers, with potential benefits for both diversification and risk management.

Where an International Value ETF fits in client portfolios

For advisors building or adjusting international allocations, VXM can be accessed in multiple ways depending on portfolio objectives and client preferences.

The ETF itself is available in different currency exposures. The standard Canadian dollar version offers hedged exposure, while VXM.B provides unhedged exposure and VXM.U provides a U.S. dollar-denominated option. This allows advisors to express currency-specific views.

While the ETF structure offers intraday liquidity, transparency and typically lower costs, it is not always the preferred vehicle in every account. Some advisors continue to favour mutual funds for operational or platform-related reasons. In response, we recently introduced CI Morningstar International Value Hedged Index Fund, which provides access to the same underlying strategy at a 0.55% management fee.

Across both structures, the core investment approach remains consistent. The focus stays on developed international equities, with a rules-based process that combines valuation metrics and earnings revisions. For advisors, that consistency allows the strategy to be applied across different client accounts while maintaining alignment in factor exposure, sector positioning and overall portfolio role.

Within a broader asset allocation, VXM or its mutual fund equivalent can serve as a complement to U.S.-heavy portfolios, helping diversify return drivers and manage valuation risk. The availability of multiple access points simply makes it easier to implement that view in practice.

This article was produced in partnership with CI Global Asset Management

IMPORTANT DISCLAIMERS

FOR ADVISOR USE ONLY. No portion of this communication may be reproduced or distributed to clients as it may not comply with Sales Communications requirements.

Commissions, trailing commissions, management fees and expenses all may be associated with an investment in mutual funds and exchange-traded funds (ETFs). Please read the prospectus before investing. Important information about mutual funds and ETFs is contained in their respective prospectus. Mutual funds and ETFs are not guaranteed; their values change frequently, and past performance may not be repeated. You will usually pay brokerage fees to your dealer if you purchase or sell units of an ETF on recognized Canadian exchanges. If the units are purchased or sold on these Canadian exchanges, investors may pay more than the current net asset value when buying units of the ETF and may receive less than the current net asset value when selling them.

The opinion and information provided in this discussion are solely those of the speaker(s) and are not to be used or construed as personal, legal, accounting, taxation or investment advice, or as an endorsement or recommendation of any entity or security discussed or provided by CI Global Asset Management. Individuals should seek the advice of professionals, as appropriate, regarding any particular investment.

This document is provided as a general source of information and should not be considered personal, legal, accounting, tax or investment advice, or construed as an endorsement or recommendation of any entity or security discussed. Every effort has been made to ensure that the material contained in this document is accurate at the time of publication. Market conditions may change which may impact the information contained in this document. All charts and illustrations in this document are for illustrative purposes only. They are not intended to predict or project investment results. Individuals should seek the advice of professionals, as appropriate, regarding any particular investment. Investors should consult their professional advisors prior to implementing any changes to their investment strategies.

Certain statements in this document are forward-looking. Forward- looking statements (“FLS”) are statements that are predictive in nature, depend upon or refer to future events or conditions, or thatinclude words such as “may,” “will,” “should,” “could,” “expect,” “anticipate,” “intend,” “plan,” “believe,” or “estimate,” or other similar expressions. Statements that look forward in time or include anything other than historical information are subject to risks and uncertainties, and actual results, actions or events could differ materially from those set forth in the FLS. FLS are not guarantees of future performance and are by their nature based on numerous assumptions. Although the FLS contained herein are based upon what CI Global Asset Management and the portfolio manager believe to be reasonable assumptions, neither CI Global Asset Management nor the portfolio manager can assure that actual results will be consistent with these FLS. The reader is cautioned to consider the FLS carefully and not to place undue reliance on FLS. Unless required by applicable law, it is not undertaken, and specifically disclaimed that there is any intention or obligation to update or revise FLS, whether as a result of new information, future events or otherwise.

Morningstar® is a registered trademark of Morningstar, Inc. (“Morningstar”) Morningstar Target Value Index (the “Index”) is a service mark of Morningstar and has been licensed for use for certain purposes by CI Global Asset Management (“CI GAM”). The securities of each CI Morningstar ETFs (the “ETFs”) are not in any way sponsored, endorsed, sold or promoted by Morningstar or any of its affiliates (collectively, ‘‘Morningstar’’), and Morningstar makes no representation or warranty, express or implied regarding the advisability of investing in securities generally or in the ETFs particularly or the ability of the Index to track general market performance.

Certain statements contained in this communication are based in whole or in part on information provided by third parties and CI Global Asset Management has taken reasonable steps to ensure their accuracy. Market conditions may change which may impact the information contained in this document. Certain names, words, titles, phrases, logos, icons, graphics, or designs in this document may constitute trade names, registered or unregistered trademarks or service marks of CI Investments Inc., its subsidiaries, or affiliates, used with permission. All other marks are the property of their respective owners and are used with permission.

The comparison presented is intended to illustrate the mutual fund’s historical performance as compared with the historical performance of widely quoted market indices or a weighted blend of widely quoted market indices or another investment fund. There are various important differences that may exist between the mutual fund and the stated indices or investment fund, that may affect the performance of each. The objectives and strategies of the mutual fund result in holdings that do not necessarily reflect the constituents of and their weights within the comparable indices or investment fund. Indices are unmanaged and their returns do not include any sales charges or fees. It is not possible to invest directly in market indices.

©2026 Morningstar Research Inc. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete, or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.

The CI Exchange-Traded funds (ETFs) are managed by CI Global Asset Management, a wholly-owned subsidiary of CI Financial Corp. CI Global Asset Management is a registered business name of CI Investments Inc. ©CI Investments Inc. 2026. All rights reserved.