Research reveals how allocations to different thematic ETFs and bitcoin could affect a balanced portfolio

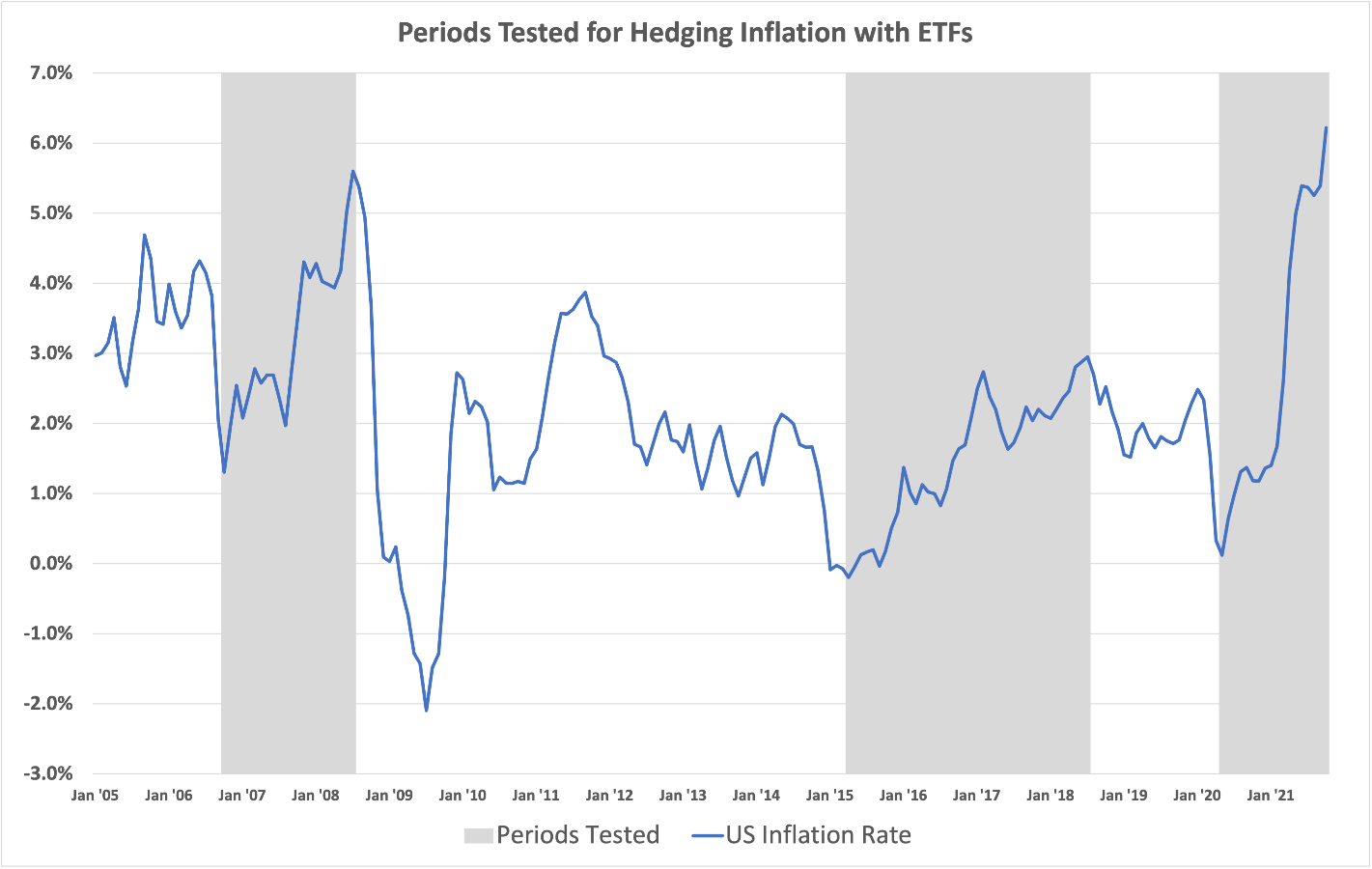

With the threat of inflation looming as large as it ever has in recent memory, advisors are looking harder than ever at their toolbox for vehicles that could help hedge their clients’ portfolios against a runaway rise in prices. And while it’s impossible to predict what kind of performance any given investment vehicle might exhibit in a high-inflation scenario, new research from YCharts could give an idea.

“YCharts is a very powerful tool,” says Connor Kitko, Director of Product Marketing at YCharts. “It's capable of running advanced analyses and modelling hypothetical strategies, visualizing what could have happened if someone had invested in a certain ETF, among other types of products and investable securities.”

That’s the exercise the firm went through in its latest paper, titled Can You Hedge It with an ETF? In a nutshell, the firm sought to determine how applying a particular ETF to a traditional balanced 60-40 portfolio could have helped – or hurt – its performance during specific historical periods when different kinds of risks ran rampant.

“A lot of the ETFs we looked at are part of a growing cohort of thematic ETFs. They’re very purpose-built to do a particular job by having very specific exposures, like climate-change ETFs or Treasury inflation-protected security ETFs,” Kitko says. “So we wanted to put these ETFs through the wringer.”

For its inflation backtesting process, the paper examined three different periods of historically significant inflation. And during each of those periods, Kitko says, the firm saw some mixed results.

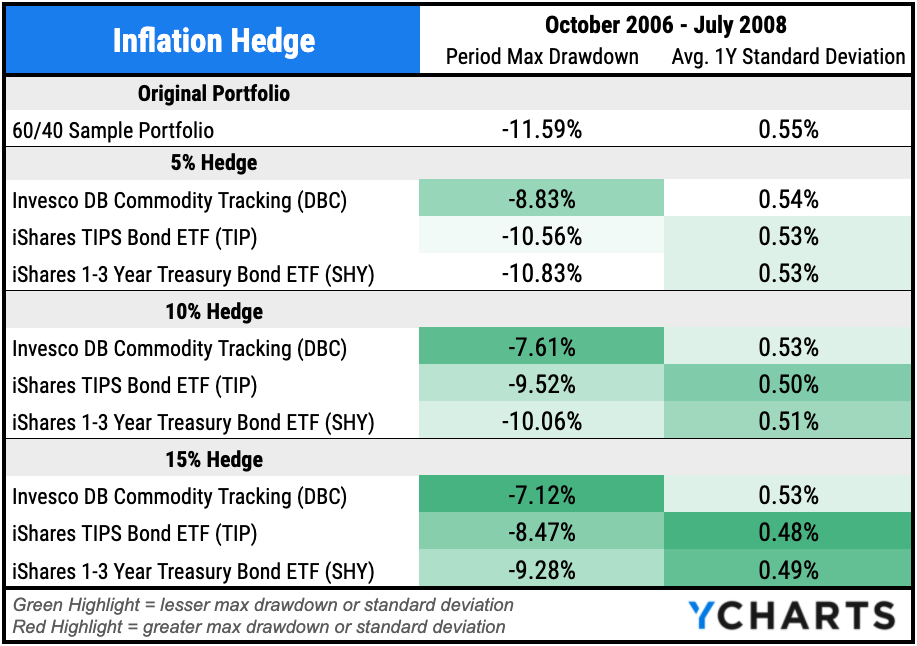

Source: YCharts

The first period, from October 2006 to July 2008, was significant not just because of the rising prices, but also because it was leading up to the global financial crisis. According to Kitko, the crisis didn’t start to take hold until late 2007; at that point, stock markets went through an acutely painful period that stretched into mid-2008.

“That 60-40 portfolio itself was already holding up pretty well. But hedging with commodities, TIPS, and short-term bonds proved effective at preserving portfolio value during this time,” Kitko says. “The commodity-tracking ETF we used also did really well as it both added performance and protected from drawdowns.”

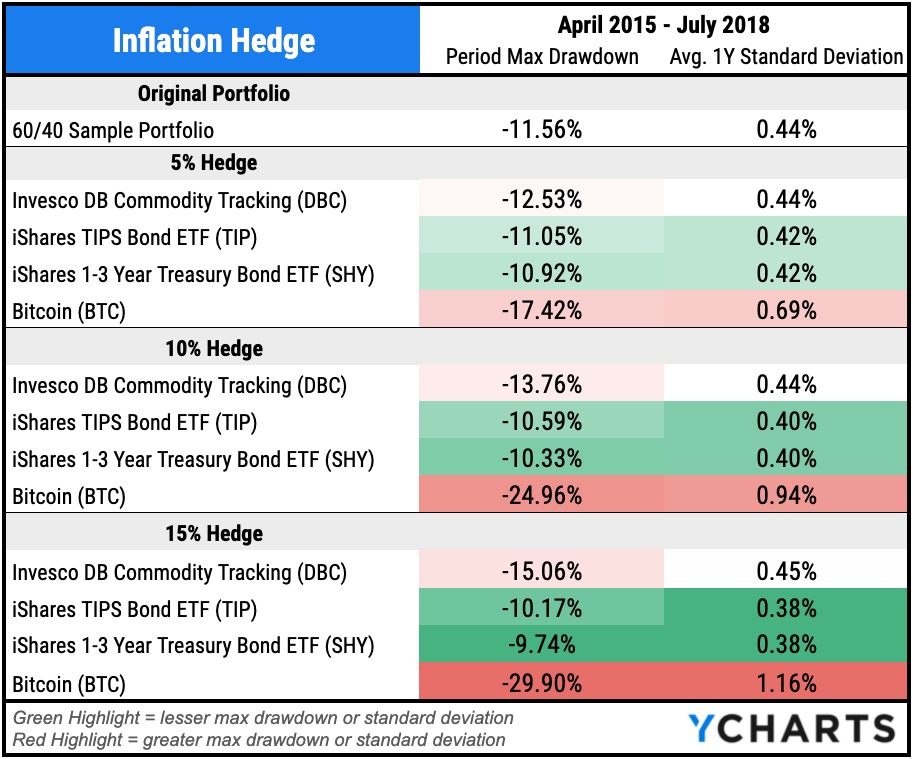

Source: YCharts

During the second high-inflation period from April 2015 to July 2018 – inflation was moving from 0% to 3% during the period, he says – stocks were doing fine. While the long-term average performance of stocks stood at 10% per year, he says stocks turned in a 12% annualized performance during the period.

While commodities, TIPS, and short-term Treasury ETFs were able to limit portfolio drawdowns, Kitko says they didn’t do that to a significant degree.

During this phase, Kitko says, the firm also began its back-testing of bitcoin performance in the face of inflation. What they found during the period was that the cryptocurrency added significant performance to the portfolio – but that’s not all.

“It was also much more volatile. So if your point was to bring stability, bitcoin did not do the job,” he says. “But with a 10% allocation to bitcoin the portfolio would have reaped 37% annualized returns over the two-and-a-half-year period, which could appeal to someone looking to preserve portfolio value over the longer term or maybe even grow their portfolio.”

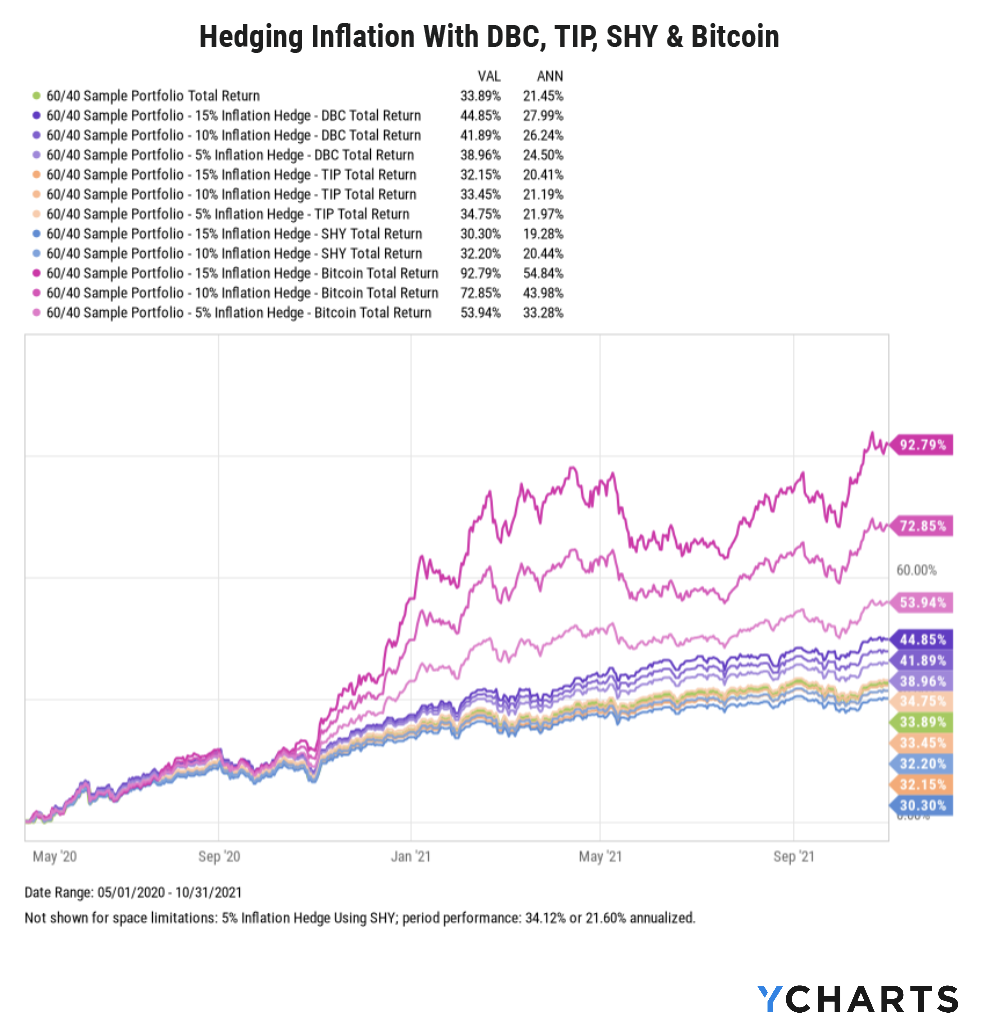

Source: YCharts

The final inflationary window, which lasted from May 2020 to October 2021, saw the S&P 500 post a 40% annualized return.

During that timeframe, YCharts found that adding a commodity-linked ETF provided some benefit relative to a naked 60-40 portfolio. Neither adding the TIPS ETF nor the short-term Treasury ETF, Kitko says, was able to boost the portfolio’s performance; in terms of protecting against drawdowns and mitigating volatility within the portfolio, he says the two hedging strategies offered negligible benefits.

“For our 60-40 portfolio, the max drawdown was 4.57%. Even with a 15% portfolio allocation to the short-term Treasury ETF, the portfolio still would have drawn down by 4.24%, he says. “I don't think any investor would be calling their advisor to say thank you for shaving off that 0.33%.”

Source: YCharts

And when it came to the bitcoin treatment, YCharts found mixed results. While they found adding a 5% bitcoin hedge to the balanced portfolio slightly improved its performance, adding 10% or 15% exposure actually lifted the 60-40 portfolio beyond the S&P 500’s performance in the period.

“So is it really an inflation hedge? Or is it just gaining that reputation?” Kitko says. “It looks almost as if being more willing to follow the crowd into Bitcoin would have worked out as a strategy. But because it adds so much volatility to portfolios, it’s hard to say it’s a hedge more than it is a speculative investment decision.”