Portfolio Management & Trading Technology for Canadian Advisors

AI strategy is ready – the planning stack is not

Rather than arriving at a greenfield, AI in wealth planning software is colliding with one of the most complex, regulated, and fragmented industries in the economy. Wealth management sits at the intersection of aging technology stacks, shifting client expectations, compressed margins, and a looming generational transfer of assets.

Over the next few years, those forces will compound, and the sector faces the equivalent of several industrial revolutions happening at once.

The structural failure mode of “digital transformation”

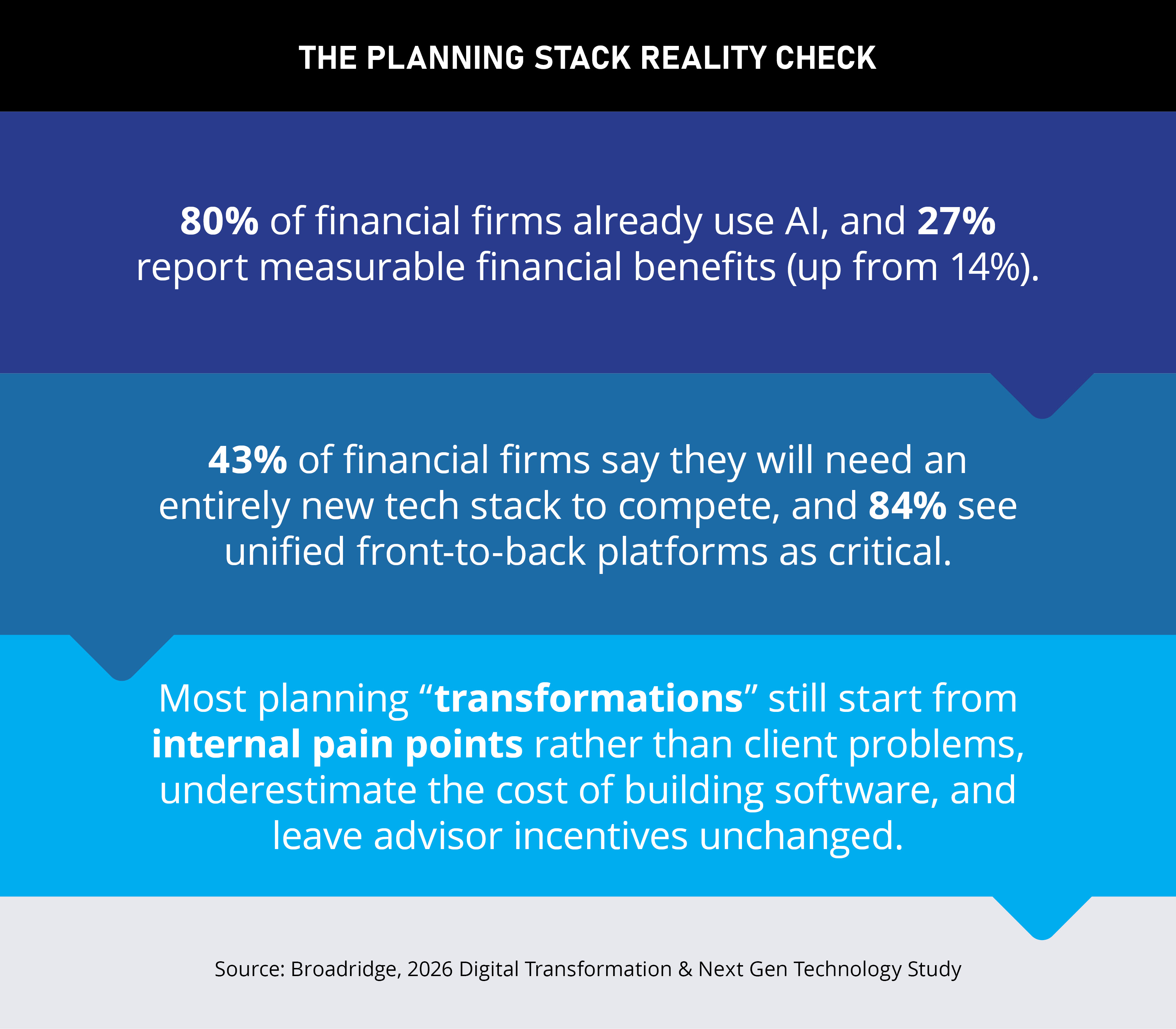

Broadridge’s 2026 Digital Transformation & Next Gen Technology study found that 80 percent of financial firms are already using AI in some form, and executives now rank AI as the single most impactful technology, ahead of cloud. Roughly one-third of technology budgets are going to innovation and next-gen capabilities, and 27 percent of firms report measurable financial benefits from AI, up from 14 percent the year before. At the same time, 43 percent of leaders believe they will need an entirely new tech stack to compete in an AI world, and 84 percent say integrating front, middle, and back office into a unified platform is critical.

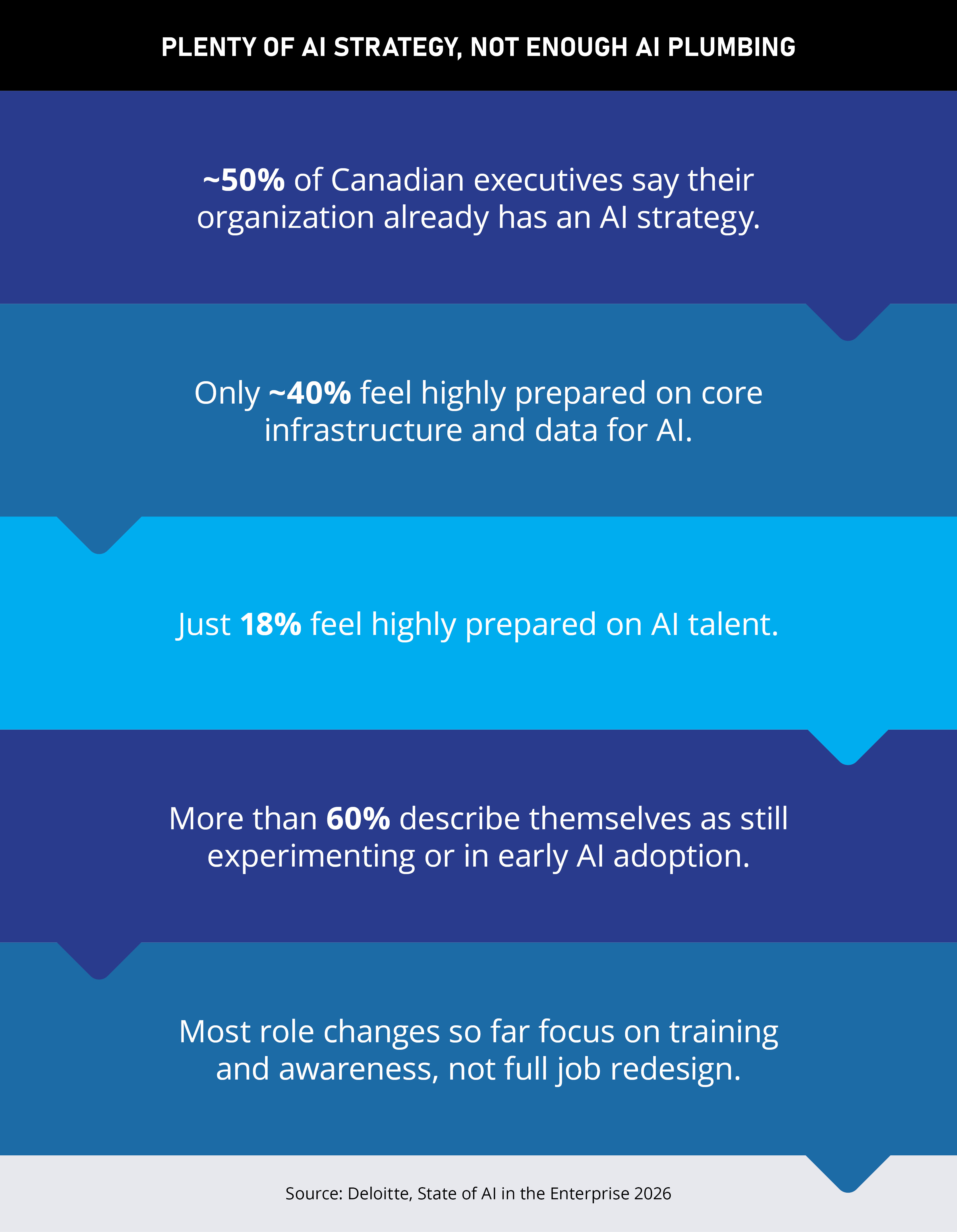

Deloitte’s 2026 State of AI in the Enterprise report paints a similar picture for Canadian institutions. Nearly half of Canadian executives say they have a defined AI strategy, and many have rolled out access to AI tools to 40 percent or more of their workforce. Yet only about four in ten feel highly prepared on infrastructure or data, and fewer than one in five say they have the AI talent they need.

Planning and wealth software sits squarely inside that contradiction. Most planning programs fail in one of three ways.

1. They begin with internal pain points, not client problems.

The project charter usually opens with issues the institution feels most acutely: fragmented KYC data, inconsistent suitability files, siloed product recommendations, and audit findings. All legitimate concerns. But they are not what clients experience when they sit down to talk about retirement, selling a business, or supporting family members.

When planning systems are architected around internal control first, the result is predictable: a platform that produces tidy reports and satisfies committees but does little to change the speed, clarity, or relevance of the planning conversation.

2. Firms underestimate the cost and complexity of building software.

Turning real-world planning practice into production-grade software is not a one-off capital project. It is a continuous R&D commitment across engineering, product, and domain experts. Most financial institutions are not organized or staffed for that.

Jeremy Fehr, who has spent decades building portfolio and risk automation at SIA Wealth, has been brought into more than one large institution after a failed in-house build. Leadership teams had already spent nine-figure sums on proprietary platforms that still were not usable. His rule of thumb is deliberately conservative: if a board thinks a new platform will cost five million, it should behave as if the real exposure could be 50 times that once overruns, integration work, and organizational drag are counted.

It is the same basic pattern the macro data hints at: heavy investment, ambitious intent, and a stack that still is not “AI-ready” in practice.

Jeremy FehrSIA Wealth

3. Incentives and workflows stay the same.

Even the best-engineered planning platform goes nowhere if it makes advisors’ days longer. They already face more documentation, monitoring, and supervisory review than they did a decade ago. If a new system demands extra data entry without visibly reducing other work, they revert to whatever lets them serve clients and hit targets.

Dan Rosen, CEO and co-founder of d1g1t, describes this pattern. “Most digital transformation efforts in wealth management don’t fail because of the technology,” he says. “They fail due to the lack of effective change management practices and principles.”

In other words, firms underestimate what it will take to change behaviour and then treat go-live as the finish line. Put those three issues together – inside-out scoping, misjudged build complexity, and static incentives – and you get the structural failure mode that keeps repeating. It is not unique to planning, but planning makes the failures visible to clients.

Technology companies are no longer circling the sector from the outside. As Fehr puts it, “Big Tech is already in the room, talking about how they will integrate into a regulated environment. They’re not looking to partner with the incumbents; they’re looking to replace them.” If incumbents cannot modernize their planning and advice infrastructure, they risk becoming distribution channels for someone else’s platform rather than principals in their own right.

Dan Rosend1g1t

The new competitive exposures for advisors

While institutions wrestle with architecture, advisors face a different set of pressures, all of which touch financial planning.

More responsibility, less usable time. Regulators and firms have both pushed more responsibility for suitability, documentation, and monitoring down to the advisor level. Tax rules and product sets have grown more complex. Every new form or review is justifiable on its own. Collectively, they compress the part of the week that can be spent thinking about client problems instead of process.

A stronger direct-to-retail planning baseline. Self-directed platforms once focused purely on execution. Many now include goal tracking, cash flow projections, and basic advice journeys built into the interface. During the COVID-19 period, a large cohort of affluent investors used extra time to familiarize themselves with these tools.

Generative AI has amplified that behaviour. With a few prompts, a motivated client can ask for a retirement scenario, an options explanation, or a tax rough cut at any hour. The output is not a full plan, but it frames expectations. Advisors are no longer the only ones who arrive at a meeting with numbers.

Asset leakage through relocation and inheritance. More high-net-worth households are considering relocating their residence or business activity for tax and lifestyle reasons. That causes assets to leave local advice channels irrespective of performance. At the same time, ownership is shifting to beneficiaries who evaluate advisors through very different lenses: digital responsiveness, clarity of interface, and perceived technological competence.

When planners have to toggle across several systems just to get a current view, that disconnect is obvious. A younger beneficiary who can see a consolidated picture of their life on a phone will not understand why their advisor cannot do the same in a meeting.

Fehr’s summary of the timing reflects those combined forces: “This whole game is going to be played out in the next 24–36 months.”

What a credible AI strategy in wealth actually requires

An AI strategy for planning and advice has to be more than a list of pilots. It has to specify how planning software, data, and people will work together in a way that clients can feel. Several elements stand out.

1. A single, reliable information spine

AI cannot compensate for inconsistent data. When 84 percent of firms in Broadridge’s survey say unified platforms are critical, they are pointing to a basic requirement: whatever mix of systems a firm uses, there needs to be an authoritative, up-to-date version of each client’s positions, goals, and constraints that every application reads from and writes to.

Without that spine, AI-enabled planning amplifies chaos: one model is using stale holdings, another is based on a different risk profile, and the CRM has yet another view of household composition. Consolidation does not have to mean one monolithic system, but it does require a deliberate data architecture.

2. Planning engines that encode rules, not just run calculations

Most planning tools already crunch numbers. What differentiates an AI-ready platform is how much of the firm’s actual decision logic is expressed in machine-readable form: how risk tolerance maps to portfolios, how debt pay-down competes with investing, how pensions and government benefits are treated, and how liquidity buffers are set.

Once those rules are explicit, AI can test them, explain them, and apply them consistently. Human planners can then spend time on edge cases and genuinely conflicting objectives rather than re-creating the same structure in each file.

3. Automation that produces compliance evidence by default

The more planning decisions are made inside a system that knows the rules, the easier it is to show that advice meets those rules. The output of a planning engine should therefore include not just a client-friendly summary but also a structured record of why recommendations were made and how constraints were honoured.

Done properly, this both reduces manual documentation for advisors and improves the quality of information available to risk and compliance compared with scanned PDFs and notes.

4. Deliberate redeployment of time

If planning automation works, it will release capacity. Broadridge’s study reports that firms investing in AI and workflow automation are already seeing measurable productivity gains. In specific deployments, SIA’s automation around portfolios and reviews has freed up on the order of 40 percent of an advisory team’s time.

A credible strategy has to state, in advance, what freed-up time is for: more systematic outreach to clients in transition, deeper planning sessions on complex cases, and proactive engagement with the next generation in key households. Without that, “productivity gains from AI” remain theoretical.

5. A clear stance on build, buy, and partner

With 43 percent of firms telling Broadridge they expect to rebuild large chunks of their stack, the temptation is to own more than is realistic. The more pragmatic approach is to decide where the firm truly needs proprietary differentiation and where it should integrate specialist platforms.

6. A non-negotiable client lens

Finally, any AI roadmap for planning should be testable at the level of a single household. If you cannot tell a client, in concrete terms, how the new system will change the speed, clarity, or relevance of their planning conversations, the strategy is not yet specific enough.

There is a phrase that has become almost a reflex in every panel and trade publication: “Advisors will still matter.” It is repeated so often that it risks losing its meaning.

The honest version of the line is this. Advisors will still matter, but only the ones whose firms give them the infrastructure to be visibly better than a chatbot. A planner who can sit with a business owner facing a sale, a couple navigating a divorce, or a family weighing how to support a parent will always have a role that software cannot fill. The empathy, the judgment, the willingness to say, “Let’s slow down and rethink this” – none of that is being automated away.

Clients are not asking advisors to become technologists – they are asking firms to provide planning systems that match the calibre of the human sitting across the desk.

Related Stories:

AI is not a feature: Why wealth management has 36 months to rethink itself

d1g1t: the integrated wealth management platform delivering speed, scale, and deeper client engagement