With interest rates rising and market volatility, it's time to revisit an old dilemma

With interest rates rising and volatility in the market, you might be debating whether to recommend value investing or growth investing to your clients. It’s a dilemma as old as the markets. Based on market dynamics, we think now is an ideal time to ensure they have the right allocation to each investing style depending on their risk tolerance.

But first, we need to explain these two ends of the investment style spectrum. As the name implies, growth stocks are expected to grow faster than the overall market. Returns from value stocks, on the other hand, come from being undervalued by the market and trading below what they could be worth, known as a stock’s “intrinsic” or “fair” value.

Growth investing

Growth stocks really took the limelight over the last ten years. Following the 2008-2009 Great Financial Crisis, low interest rates and a rising tide of market growth meant that many companies could cheaply access money to invest in expansion. This was a great time for growth, since these companies often trade based on their expected future value and at prices that are a much higher multiple of their earnings or book value than value companies.

They don’t usually pay dividends since they require capital to grow. Instead, they reinvest earnings to grow. You’re more likely to find them in sectors such as technology, discretionary consumption and healthcare.

Value investing

Value stocks are often less volatile than growth stocks for two reasons. Firstly, they’re not as cyclical, meaning they don’t follow economic trends as closely. When market sentiment turns sour and interest rates rise, they’re less likely to lose access to capital. Secondly, they’re more defensive than growth stocks. They’re often more mature companies with a proven track record of success, a stable business model and dependable revenues.

Value stocks are less focused on future growth and tend to pay more dividends, which adds to value’s returns over time. You can find value companies in the financial, industrial, energy and basic materials sectors.

Value investors often look long term, searching for companies with durable competitive advantages. These include moats like a high barrier to enter an industry, or attributes like a strong brand or a large and loyal customer base. The value investor then invests at a price that provides a margin of safety. The market can often undervalue the health of these companies when the going’s good, which gives value investors opportunities when rates rise.

Growth or value?

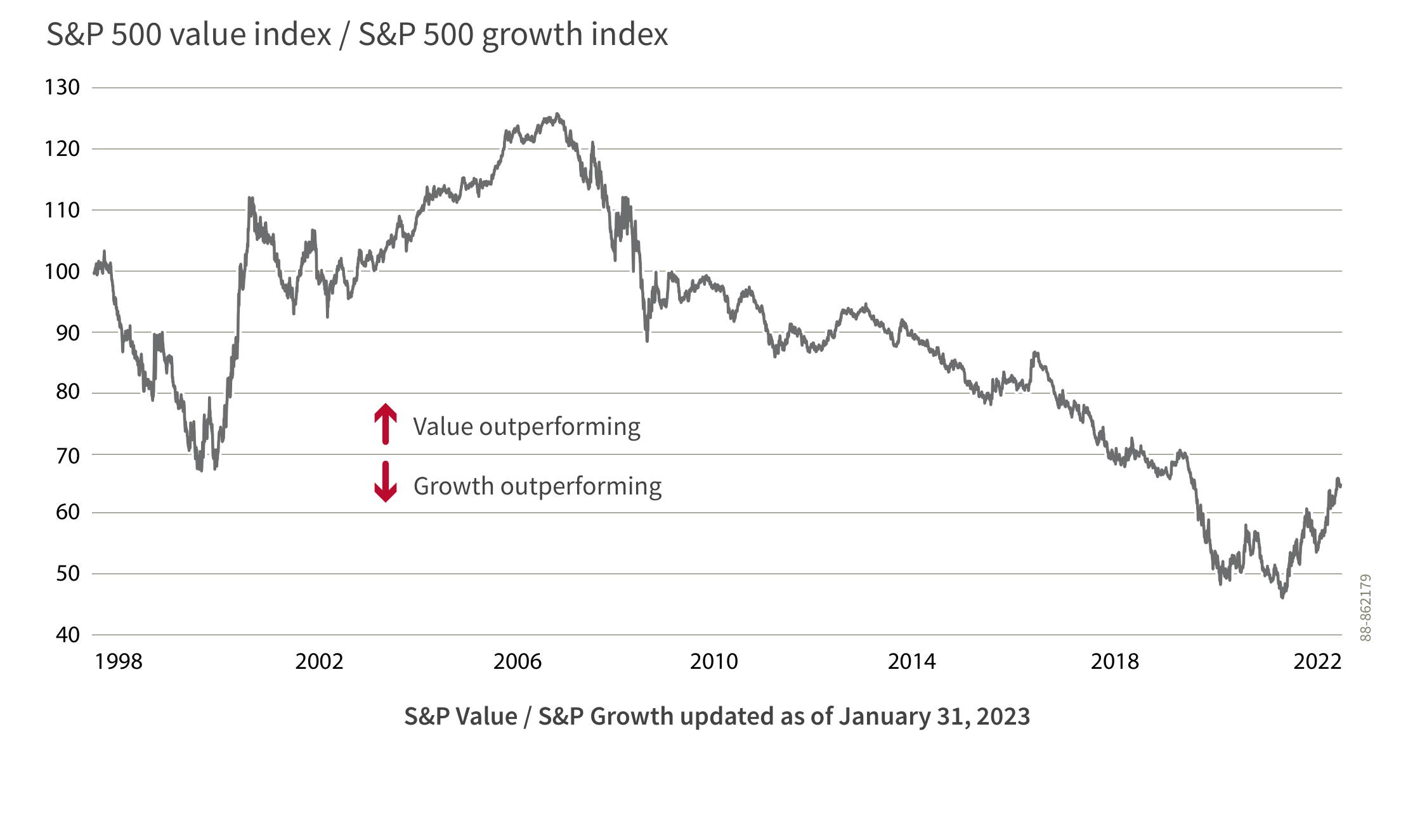

Will value stocks outperform in 2023? Even within one business cycle, we can see “rotations” from one style to the other as they fall into and out of favour. For the S&P 500, the contribution of each style to total returns is split almost down the middle:

Similar to the low-rate era that followed 2008, a dynamic of rapid growth and low interest rates after the COVID-19 pandemic helped growth companies outperform value in the short term. More recently, excitement about artificial intelligence has given growth – specifically, megacap technology stocks – the edge. In fact, the market’s growth this year is mostly thanks to growth.

But since the market has now marked up the price of these growth stocks even more, how much is left for investors? It’s this question that’s led some analysts to believe value investing could soon have the edge, since less of the style’s fair value has been recognized by the market.1 Benjamin Graham, a legendary investor who is often regarded as the “father of value investing,” wrote that “a great company is not a great investment if you pay too much for the stock.”2

And it’s not just the limited boost that AI or other secular trends can provide in the short term. The uncertain economic outlook is more painful for growth than value. Monetary policy, tightened at the fastest pace in decades, is making it more expensive for companies to borrow money and grow. These shifts from central banks take time to show up in the market, which is why value could start to outperform if volatility ratchets back up and the market sputters.

For most investors, the question of value. vs. growth remains a rhetorical one. A balanced and properly diversified portfolio will help to capture returns no matter which style is in favour. But now is the time to make sure clients have the right allocation to value that aligns with current economic conditions, their risk tolerance and their long-term goals.

Visit our investment spotlight to learn more about value investing

1 Sarah Dziubinski and David Sekera, “Should You Invest in Growth Stocks or Value Stocks Now?,” Morningstar, April 10, 2023, https://www.morningstar.com/stocks/should-you-invest-growth-stocks-or-value-stocks-now-2.

2 Benjamin Graham, The Intelligent Investor, 1949.

Disclaimer:

This material is presented only as a general source of information and is not intended as a solicitation to buy or sell specific investments, nor is it intended to provide tax or legal advice. This material may contain forward-looking information that reflects our or third-party current expectations or forecasts of future events. Forward-looking information is inherently subject to, among other things, risks, uncertainties and assumptions that could cause actual results to differ materially from those expressed herein. These risks, uncertainties and assumptions include, without limitation, general economic, political and market factors, interest and foreign exchange rates, the volatility of equity and capital markets, business competition, technological change, changes in government regulations, changes in tax laws, unexpected judicial or regulatory proceedings and catastrophic events. Please consider these and other factors carefully and not place undue reliance on forward-looking information.

Canada Life and design and Canada Life Investment Management and design are trademarks of The Canada Life Assurance Company.