Morningstar reports on US and Canadian banks point to 'manageable' exposure to flagging real estate assets

US banks have been underexposed to office real estate since the 2008 financial crisis and right now, that position is helping many of these banks manage risk from a real estate sector with bleak forward prospects. A recent report from DBRS Morningstar highlighted some of the challenges facing US banks emerging from their loans to office real estate.

Since 2019 office real estate vacancies in the US have spiked from 9.5% to 13.1%. That pain is at its most acute in major cities like New York, San Francisco, and Los Angeles which have vacancy rates of 17.3%, 23.2%, and 22.5% respectively. While these vacancy rates, and the underlying trend of remote work driving them, could present a structural risk for commercial real estate and the institutions lending them money.

Rather than the catalyst for another small financial crisis — akin to the collapse of Silicon Valley Bank — in March of this year, the DBRS Morningstar report found that US banks’ exposure was relatively manageable. The outlook mirrors an earlier report, too, which found Canadian banks could handle their commercial real estate loans, despite similar risks.

“We've seen the banks that we follow, have fairly diversified portfolios, so they're not overweighted in any commercial real estate sector, per se. They do seem to be underweight office, which is the area of most concern currently, although, higher rates do impact the entire commercial real estate portfolio and refinancing scenario,” says John Mackerey, senior VP North American Financial Institution Ratings for DBRS Morningstar. “Since the great financial crisis office properties have been financed outside of the banking system, maybe to a greater extent than other types of property. We've also learned that not all offices are the same. Some banks have exposure to medical office, which is has different vacancy scenarios than commercial offices. We are seeing differences in cities as well as differences in in types of properties.

“I would say the areas of most concern now, are the class B, and C properties in in non-prime locations.”

US Banks, as the below graphic shows, are relatively lightly exposed to office loans in general and, according to Mackerey, their exposure to those riskier class B and C properties is even lower.

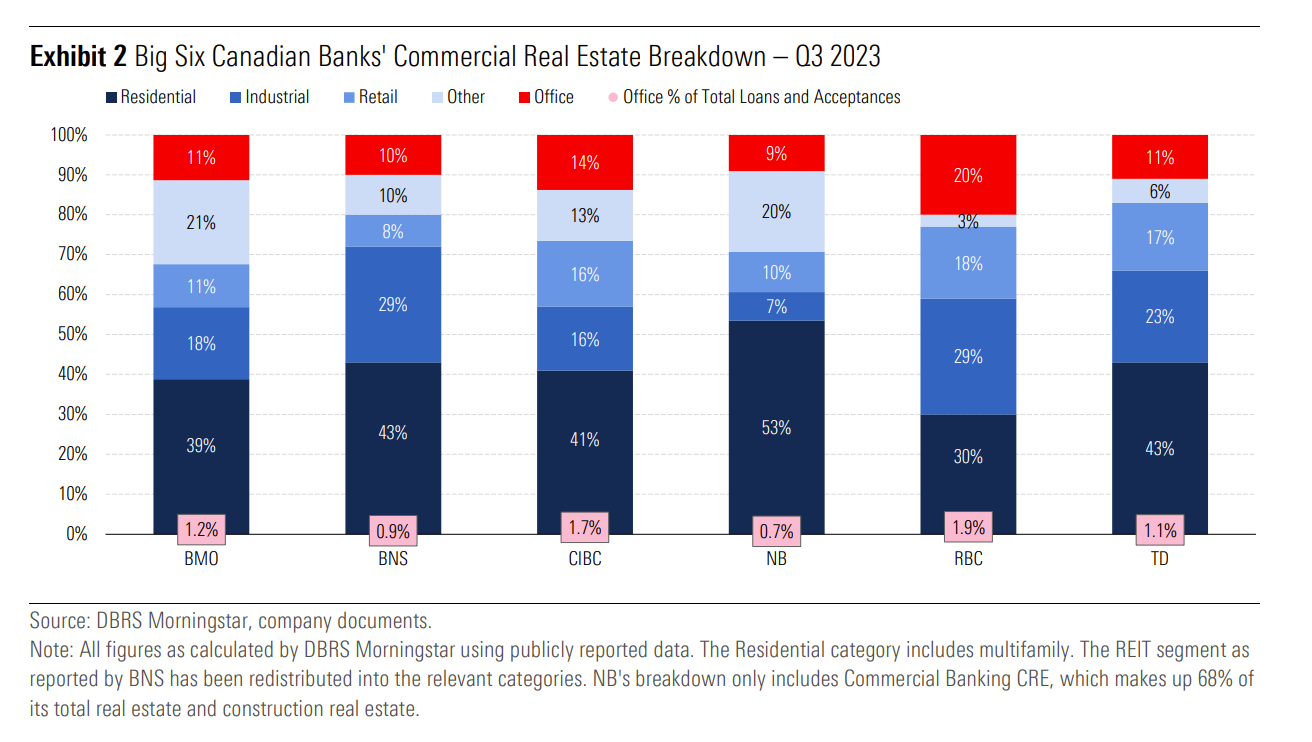

Canadian banks, Mackerey says, have a similar level of office exposure – sitting around the 2% mark. It’s a level that he believes to be ‘manageable.’ Nevertheless in both Canada and the US we will likely start to see a rise in delinquencies as higher interest rates, high vacancy rates, and a slowing economy begin to make significant impacts on the commercial real estate space.

One key stage that banks on both sides of the border will have to navigate is the valuation impact on these properties as they come up for renewal. With cashflows down from the levels at the time of these initial loans, either the owner or the sponsor will have to put up more capital to make these loans acceptable to the banks. At the same time, valuations may be hard to ascertain because very few of these properties have been trading hands since the onset of the pandemic, outside of fire sale situations.

Mackerey’s prediction of resilience is due, in part, to Federal Reserve stress tests. The central bank has run simulations of a severe downturn in commercial real estate prices — drops as significant as 40% — while US banks would lose hundreds of billions in this scenario, the Fed found they would be “sufficiently capitalized” after taking those hits.

Canadian banks have a relatively higher exposure to office real estate, but according to DBRS Morningstar their exposure is largely focused on class A offices, which have significantly lower vacancy rates than the overall averages.

Some of the big six, however, have more exposure to US office real estate. Notably BMO, CIBC, RBC, and TD have more than 50% of their total office portfolios in US loans. However, these banks have limited their lending to offices since the pandemic and their conservative underwriting practices and strong cash reserves should buffer against what Mackerey expects will be a rough period for US and Canadian banks, despite their relative resilience.

“The exposure is manageable, there's likely to be some pain, but we think it's absorbable,” Mackerey says. “Especially for the banks we rate, which tend to be the large regionals and large banks. It's certainly in the scheme of their overall risk profile. It's an area that they're focused on, where they're spending a lot a lot of time, but it's not an area of great concentration.”