It's not how much money you make, it's how much money you keep. Segregated funds offer investors the ability to do both.

This article is sponsored by Canada Life

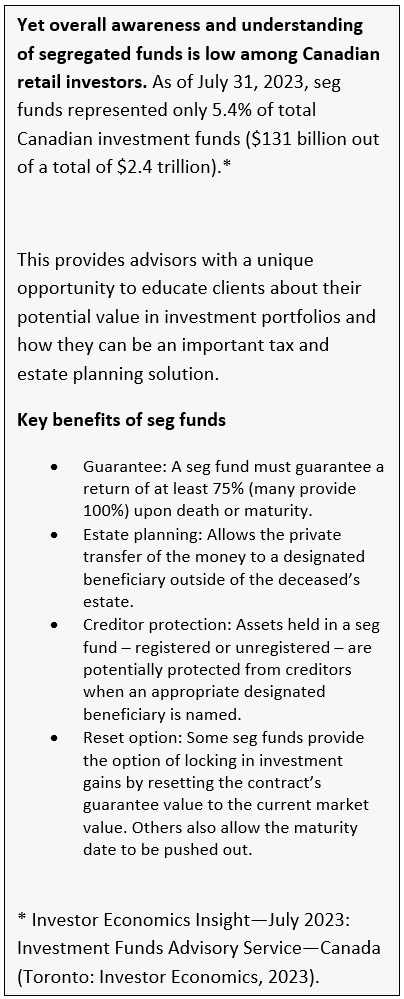

With the ongoing turbulence in global economic markets, investors are increasingly searching for ways to protect their investments. Segregated funds can help. Whether investors are seeking to protect their portfolios from market volatility, in the estate planning process or are business owners, segregated funds offer a unique combination of growth potential and insurance protection. Segregated funds have long been misunderstood by many Canadians and these misunderstandings have kept some investors at bay. In this article, we’ll debunk some of these myths and explain why segregated funds are a compelling option for investors in todays market.

Myth 1: Segregated funds are only for clients in their retirement years.

One common myth about segregated funds is that they’re exclusively for clients in or close to retirement. It's true that segregated funds offer principal protection and estate planning benefits, making them a suitable choice for those who want to safeguard their investments. However, segregated funds also offer a broad array of investments which include a variety of asset classes, including equities, allowing for growth potential while maintaining a level of protection. This makes them a versatile planning solution not only for retirees but also for pre-retirees and younger clients that are more risk conscious. Business owners can also benefit from the unique investment planning features offered by segregated funds.

“Risk-conscious portfolio construction is critical. This makes seg funds more relevant than ever. The guarantees offered by this product can help investors comfortably navigate volatile markets. They can also provide clients with estate planning support, and for business owners potential creditor protection. The benefits of segregated funds are multifaceted! This makes them a valuable solution to serve the needs of many clients.” – Steve Fiorelli, Senior Vice President Wealth Solutions, Canada Life.

In today's market conditions, where uncertainty is the norm, having a balance between growth and protection is invaluable. Investors can use segregated funds as part of a diversified portfolio to manage risk effectively.

Myth 2: Segregated funds lack investment flexibility.

Some advisors believe that segregated funds are restrictive in terms of investment choices, but this is far from the truth. More comprehensive segregated fund lineups have been introduced that include a variety of management styles, provide broader geographic coverage and are available in most major asset classes.

“Today’s segregated funds provide access to well-known, institutional-quality investment managers who are building and overseeing diversified portfolios. From standalone segregated funds to managed solutions, advisors can curate a portfolio to fit their clients’ needs at every stage of life. We’re also providing more unique asset classes, such as private credit and direct real estate, within our segregated fund offering to provide investors greater diversification and more avenues for risk-adjusted returns” Steve Fiorelli, Senior Vice-President, Wealth Solutions, Canada Life

With this broader lineup of investment solutions users can construct robust, well diversified portfolios capable of adapting to various market conditions. In the current market environment characterized by economic uncertainty, finding investment options that offer growth potential and diversification is crucial.

Myth 3: Segregated funds are expensive.

The misconception that segregated funds come with exorbitant fees can deter potential investors. While it’s true that segregated funds typically have higher management fees than mutual funds and exchange traded funds, it’s essential to consider the added value they provide, such as insurance protection and estate planning benefits. Segregated fund policies offer maturity and death benefit guarantees at different levels and additional features such as the opportunity to lock in investment growth through regular resets.

“Over time, the discrepancy between fees for segregated funds and mutual funds has decreased significantly. We’re seeing fee compression across most products within the industry.” Steve Fiorelli, Senior Vice President Wealth Solutions, Canada Life.

In addition to the insurance protection provided by segregated funds, there are also many estates planning benefits which advisors should consider as important characteristics of this solution. Estate planning is an important conversation most Canadians families should have. The total amount expected to be transferred from one generation to the next within Canadian households over the decade ending 2030 is projected by Investor Economics to be $1,640 billion* This has cast a new spotlight on segregated funds due to their unique advantages when it comes to intergenerational wealth transfer. Features like quick settlement with named beneficiaries help you bypass the estate and probate fees and simplify the distribution and transfer of assets. Segregated funds also may offer privacy during the distribution of assets.

In the current economic climate, where preserving and growing wealth is paramount, the insurance component of segregated funds can offset the slightly higher fees. In addition to estate planning benefits, segregated funds also offer a unique combination of professional management, diversification, and protection against market downturns, making them a cost-effective solution for many investors.

With today's uncertain market conditions, segregated funds can provide a compelling solution for investors.

At Canada Life, with 175 years of experience under our belt, we’ve built one of the strongest segregated fund shelves in the industry. Our shelf brings you access to a leading market share, diverse selection and among top performing products. We know these are the metrics that matter to you when building portfolios that offer financial growth and protection for your clients. Contact your Canada Life wealth wholesaling team if you have any questions about our segregated fund shelf or the resources available to you.

Want to learn more about the opportunity and how to communicate the benefits of segregated funds to your clients? Download Canada Life’s report, The Case and Space for Segregated Funds.

Disclaimers:

*Investor Economics Insight—July 2022: Investment Funds Advisory Service—Canada (Toronto: Investor Economics, 2022)

This material is for advisors only and is not intended for use with clients. This commentary is presented only as a general source of information and is not intended as a solicitation to buy or sell specific investments, nor is it intended to provide tax or legal advice.

Guarantees are less a proportional reduction for withdrawals, including taxes, short-term trading fees and any other applicable charges. In Saskatchewan, executors must disclose all known life insurance policies owned by the deceased, including segregated fund policies. They must list the insurance company, policy number, designated beneficiaries and the value at the date of death. Creditor protection depends on court decisions and applicable legislation, which can be subject to change and can vary for each province; it can never be guaranteed. Talk to your legal advisor to find out more about the potential for creditor protection for your specific situation.

A description of the key features of the segregated fund policy is contained in the information folder. Any amount that is allocated to a segregated fund is invested at the risk of the policyowner and may increase or decrease in value.

Canada Life and design, and design are trademarks of The Canada Life Assurance Company.