CMHC report says that the risk of rising defaults remains in the third and fourth quarters of 2020

Every month, more than $1 billion mortgage payments are deferred thanks to lender programs to assist those impacted by the pandemic.

But as these programs reach the end of their 6-month limits, there remains a risk that defaults will rise according to a new report from the Canada Mortgage and Housing Corporation (CMHC) based on available data at the end of the second quarter of 2020.

The average monthly payment being deferred is $1,300, a sizeable sum for households where incomes has dropped due to reduced hours or complete loss of employment.

Around 760,000 payments are deferred or skipped across chartered bank customers but the report notes that non-bank lenders are also offering deferrals, so the total number of payments that will become payable again is likely to be higher.

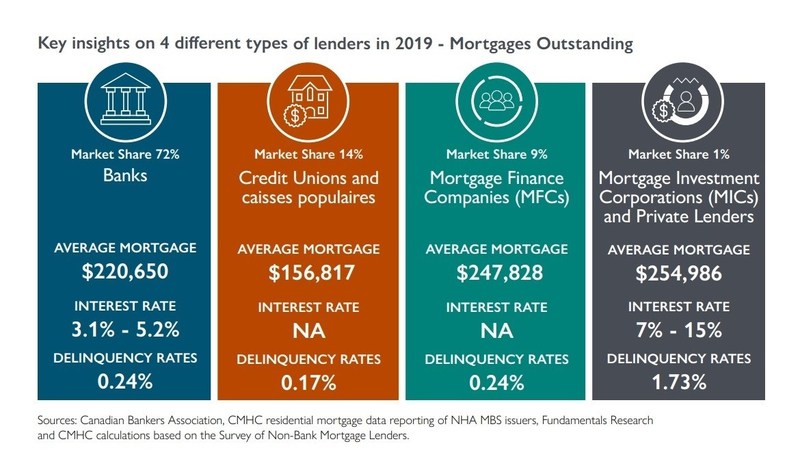

Mortgage delinquencies of 90 days or more remained at low levels for all mortgage lender types in the first half of the year which suggests that a steady share of mortgage holders continued to be able to make their payments or were able to defer their mortgage payments.

Rise in uninsured loans

There has been a trend towards higher levels of uninsured mortgage loans and this reached 63% in the first quarter of 2020.

''We observed a surge in outstanding residential mortgage credit in the first five months of 2020. This mortgage credit acceleration is a result of an increase in newly extended mortgages, given residential property sales were up late last year and early this year, and a record number of homeowners deferring their mortgage payments from impacts of pandemic-related economic shutdowns,” said Tania Bourassa-Ochoa, CMHC, Senior Specialist, Housing Research.

Portfolio-insured mortgages accounted for 31% of all insured mortgages from chartered banks at the end of 2019, down from 35% in 2018. Across non-bank mortgage lenders, the value of insured mortgages decreased slightly (1%) during the last quarter of 2019 compared to a year earlier.

The report shows that deposits continued to be the primary source of mortgage funding for the big six banks (66%) and credit unions (77%); covered bonds made up 17% of total mortgage funding for Canada's big six banks at the end of the first quarter of 2020, representing an increase of 4% from 2019; and private securitization, continued to account for a very small share of the mortgage funding mix in Canada, with just 1.1%.

However, the residential mortgage-backed securities market appears to be expanding.

![]()