Accounting professionals recognize importance of non-financial information, though

As the push for ESG spreads across the world, there’s a growing demand for company reports to step outside the box of traditional financial metrics. Fortunately, accounting the majority of professionals are up to the challenge, if a new report from Chartered Professional Accountants of Ontario (CPA Ontario) is anything to go by.

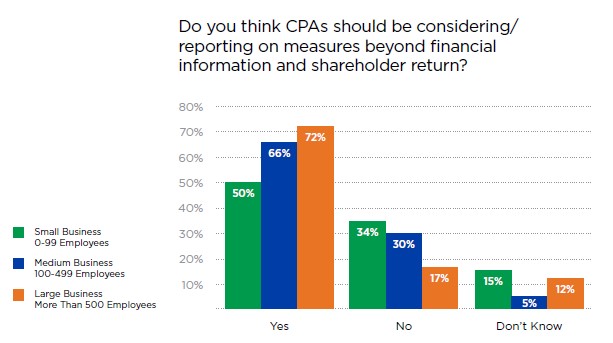

Drawing from a survey of CPA Ontario members conducted between August and October 2020, the report titled CPAs and the New Social Contract: The Rise of the Warrior Accountant found a majority agreed that CPAs should consider and report on information beyond shareholder return.

Respondents working in large businesses with more than 500 employees were the most likely to agree (72%), and those in small businesses with fewer than 100 employees were the least likely to do so (50%).

Source: CPA Ontario survey

Source: CPA Ontario survey

“Ontario’s small and medium enterprises will often be reluctant to pick up the ESG mantle unless their business and retail customers demand it,” Bill Murphy, FCPA, FCA, and National Climate Change and Sustainability Leader at KPMG said in the report.

While some may be reluctant to support the cause of ESG, the writing is on the wall. The report noted ESG reporting is increasingly being embraced by the business community, with the most enthusiastic adoption in Europe, the United Kingdom, and Australia; Canada is in a middle position between those countries and the U.S. Much of that has been powered by a focus on climate risk, although interest in social factors has undergone a recent exponential rise as politicians and economists start to view systemic inequality as a hindrance to growth.

CPA Ontario also cited a raft of push and pull factors that are strengthening the case for ESG disclosure. As institutional and retail investors exhibit a rising appetite for ESG-focused strategies and products, index and ratings providers are coming out with ranking and scoring systems to reward “top ESG performers” and “most sustainable companies.” Regulators across the world are moving to turn voluntary ESG disclosures into mandatory reporting requirements, and community groups are putting pressure on large corporations as they voice their respective social frustrations.

While the clamour for ESG is clear, CPAs will certainly find it hard to parse the signals from the noise. As businesses face increasing demands to measure and report on their ESG performance, an “alphabet soup” of voluntary frameworks and guidelines has emerged, including ones from the Global Reporting Initiative (GRI), the U.S.-based Sustainability Accounting Standards Board (SASB), Canada’s Taskforce on Climate-related Financial Disclosures (TCFD), and the United Nations-supported Principles for Responsible Investment (PRI). And while there’s broad agreement that standards need to be harmonized, multiple standardization projects are afoot, frustrating efforts to establish one widely-adopted reporting standard.

“Investors have had a ‘Goldilocks problem with ESG standards,’” said Sarah Takaki, senior director, Sustainable Investing, Healthcare of Ontario Pension Plan. “At first, there was a lack of them, and then there were too many, which effectively means there is no standard.”