The Canadian luxury tax is here—are your clients prepared? Find out how what vehicles are affected and what this means for your business

On September 1, 2022, the federal government introduced a tax targeting several high-value vehicles. The tax is intended to have high-net-worth individuals who splurge on lavish items contribute more to the tax system.

What exactly is covered by the luxury tax? What are the exemptions? Who is responsible for making tax payments? This guide will walk you through what you need to know about the Canadian luxury tax.

How does Canada’s luxury tax work and why was it implemented?

With the country reeling from the economic impact of the COVID-19 pandemic, the government proposed the introduction of a luxury tax as part of the 2021 Federal Budget. In March 2022, a draft bill was released for the Select Luxury Items Act, which imposed a tax on the sale of luxury vehicles.

The luxury tax targets wealthy Canadians purchasing high-value cars, aircraft, and boats. It also affects vendors and manufacturers involved in the production and sale of luxury vehicles.

According to official documents, the luxury tax is intended to make “those who can afford to buy luxury goods contribute a little bit more” to the tax system.

Canadian luxury tax, however, acts as a form of indirect tax. This places the responsibility of paying taxes on the vendors with the understanding that they will pass on the tax burden to their ultra-rich clients. They do this by incorporating the tax in the price of the luxury vehicle.

What is subject to the Canadian luxury tax?

The luxury tax applies to certain vehicles that exceed these price thresholds:

- $100,000 for motor vehicles and aircraft

- $250,000 for vessels

“The tax calculated is either 10 percent of the taxable amount or 20 percent of the amount above the $100,000 and $250,000 thresholds, whichever is less,” explains Tim Brisibe, vice-president of tax and estate planning at the investment management firm Mackenzie Investments.

“The taxable amount is the value of the consideration for the sale of the subject vehicle and value of the consideration for any improvements made by the vendor to the subject vehicle in connection with the sale that is not included in the above.”

Apart from the price thresholds, there are specific criteria that luxury vehicles must meet before they become subject to taxes. Let’s go over the requirements for each category.

Motor vehicles subject to Canadian luxury tax

A “subject vehicle,” according to the tax rules, can include:

- convertibles

- coupes

- hatchbacks

- light‑duty pickup trucks

- sedans

- sports cars

- sport utility vehicles (SUVs)

A motor vehicle will be subject to the luxury tax if it meets all these criteria:

- its price exceeds $100,000

- it must be designed primarily to transport people on streets and highways

- the seating capacity is less than 10

- its gross weight doesn’t exceed 3,856 kilograms

- it was manufactured after 2018

- it’s designed to travel with at least four wheels touching the ground

Aircraft subject to Canadian luxury tax

A “subject aircraft” can be an airplane, glider, or helicopter as defined by the Canadian Aviation Regulations (CAR).

The luxury tax applies if the aircraft’s price exceeds the $100,000 threshold, it was manufactured after 2018, and it meets any of the following:

-

it has at least one pilot seat and cannot have any other seating configuration

-

it has at least one pilot seat or doesn’t have any seats, and cannot have a seating configuration of 40 or more, excluding pilot seats

-

it has at least one pilot seat and one passenger seat, and has a seating configuration of 39 or fewer, excluding pilot seats

Vessels subject to Canadian luxury tax

The Luxury Items Tax Act defines a vessel as a “boat, ship or craft that is designed, or is capable of being used, solely or partly for navigation in, on, through or immediately above water, without regard to the method or lack of propulsion.”

This includes:

- cruisers

- deck boats

- houseboats

- sailboats

- waterskiing boats

- yachts

For one to become a “subject vessel,” it must meet all of the following:

- its price exceeds $250,000

- it must be designed for recreational or sports activities

- it was manufactured after 2018

What is exempt from the luxury tax?

The luxury tax doesn’t apply to high-value vehicles that fall into the following categories:

Motor vehicles exempt from the luxury tax

The following aren’t considered subject vehicles even if they exceed the price threshold:

- ambulance

- hearse

- marked vehicle designed for law enforcement activities

- marked vehicle designed for medical emergencies and fire response

- recreational vehicle that functions as residential accommodation and has at least four of the following:

- kitchen or facilities for cooking

- ice box or refrigerator

- heating or air-conditioning system that doesn’t rely on the vehicle’s engine to operate

- self-contained toilet

- portable water supply system with sink and faucet

- 110V to 125V electric power supply or liquified petroleum gas (LPG) supply that doesn’t rely on the vehicle engine to function

- motor vehicle registered with a government (federal or provincial) and delivered before September 2022

Aircraft exempt from the luxury tax

The Canadian luxury tax doesn’t apply to an aircraft if it’s:

- designed and equipped for military activities

- designed only for the transport of goods

- registered with a government and delivered before September 2022

Vessels exempt from the luxury tax

The following are excluded from the law’s list of subject vessels:

- floating home that meets the definition in subsection 123(1) of the Excise Tax Act

- commercial fishing vessel

- commercial vessel designed for ferrying passengers or vehicles on a fixed schedule

- vessel with sleeping facilities for more than 100 non-crew members

- vessel registered with a government and delivered before September 2022

“In most cases, the luxury tax will not apply to sales of subject vehicles priced above the price threshold that have been previously registered with the Government of Canada or a province, as set out in subsection 19(2),” Brisibe says.

“However, the luxury tax will apply if the subject vehicle was registered only because of the sale and has never otherwise been registered with the Government of Canada or a province.”

What triggers the luxury tax?

If a vehicle is subject to luxury tax, the vendor must register with the Canada Revenue Agency (CRA). They must then report and remit all applicable taxes on the subject vehicles. It’s understood that the vendor will pass the cost of the luxury tax to their wealthy buyers.

There are several scenarios that can trigger luxury taxes on high-value vehicles. Let’s go over each one.

Sale of a subject vehicle

When a subject vehicle, aircraft, or vessel is sold, the luxury tax becomes payable once the buyer takes possession or ownership, whichever comes first.

Importation of subject vehicles

If a motor vehicle, aircraft, or boat priced beyond the threshold is imported to the country, the Canadian luxury tax applies. Note that GST/HST and provincial sales taxes are excluded from the threshold. This means that these taxes are included only after the total value of the vehicle has been calculated.

Leasing of subject vehicles

If a vendor leases out a subject vehicle that’s not previously registered with a government, they are liable for paying the luxury tax. They must pay the tax once the lessee receives the right to use the vehicle as stipulated in the contract.

Pre-sale improvements made to subject vehicles

Any upgrades made on a subject vehicle are taxable if they cost more than $5,000. The luxury tax is payable a day after the improvement period ends, usually a year. For a vehicle sold on May 9, 2025, for example, the improvement period runs until May 9, 2026. So, the luxury tax will be payable on May 10, 2026.

However, if the modifications are made specifically to sell the vehicle, the luxury tax and the improvement costs are payable upon the sale’s completion.

Post-selling improvements made to subject vehicles

If the upgrades are made post-sale, the owner is responsible for paying the luxury tax.

Vendor no longer registered with the CRA

An unregistered vendor is liable for paying Canadian luxury tax if they are still holding tax-free subject vehicles.

How is the luxury tax calculated?

The Canadian luxury tax is determined as the lesser of:

- 10 percent of the taxable amount

- 20 percent of the difference between the taxable amount and the price threshold

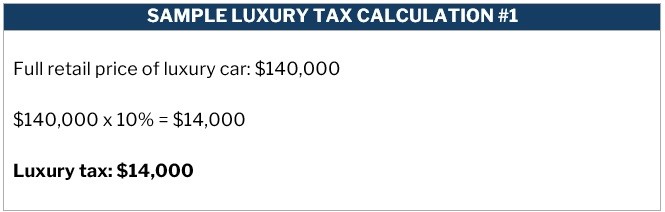

Here’s a sample luxury tax calculation for a registered vendor selling a $140,000 luxury car to a non-registered client.

Clearly, the second calculation is lower and applies to the hypothetical sale above.

Note that improvement costs and fees and charges incurred in the delivery or importation of the subject vehicle are included in the retail price. The luxury tax is then added to the total amount for the purpose of calculating GST/HST and other provincial taxes.

What are the penalties for missing luxury tax payments?

Luxury tax returns follow a quarterly reporting. The deadline for filing is the last day of the month after the last day of the reporting period. If your reporting period is in the second quarter (between April 1 and June 30), then you must pay the luxury tax by July 31.

“Your payment is due at the same time as your return,” Brisibe says. “The CRA will charge you interest if you have an overdue amount on your return or make a late or insufficient payment.

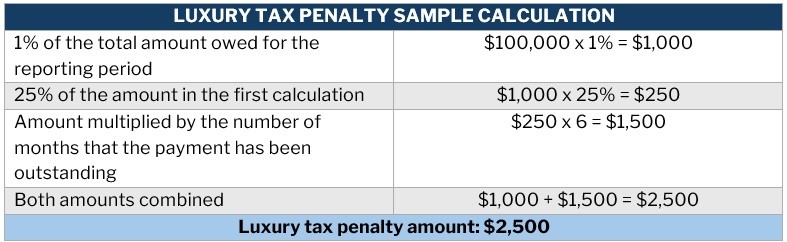

“The penalty will be the sum of 1 percent of the amount that was required to be paid for the reporting period and 25 percent of that amount multiplied by the number of months – not exceeding 12 months – from the day on which the return was required to be filed.”

Here’s a sample calculation for a vendor who missed paying $100,000 in luxury taxes for six months.

While this amount may seem small, a business selling a large number of luxury vehicles can easily incur a huge sum.

To avoid penalties, Brisibe shared this piece of advice: “To ensure compliance, set up an automatic notification system for when your sale prices surpass the luxury thresholds ($100,000 for vehicles and aircraft, and $250,000 for vessels), and pay the luxury tax as required.”

Vendors can also access exemptions to alleviate the tax burden. If you’re in the business of selling luxury vehicles, an experienced tax and wealth advisor can help provide guidance.

Visit our Industry News Section if you want to keep abreast of the latest in Canadian luxury tax. Bookmark this page for easy access to breaking news, expert interviews, and the latest industry updates