Wealth Professional Canada takes a look back at all the topics that dominated headlines in the financial services industry in 2019, from recession worries to the rise of liquid alternatives

Advisors had plenty to keep an eye on in 2019. While a variety of stories dominated the headlines, many revolved around the overall theme of global uncertainty caused by the Trump administration and its trade dispute with China. The standoff between these two economic superpowers has bled into all areas of the global economy, affecting growth, interest rates and the business cycle.

Yet despite all the negatives surrounding the trade war, there were other areas that made positive news in 2019: New sectors garnered investor interest, updated regulations allowed alternative investments to hit the retail channel, ESG continued to make its presence felt in portfolio conversations, and the ETF industry remained on a path of impressive growth and performance.

Much has transpired in the financial services field over the past year, but uncertainty is still a common theme. There are many questions that remain unanswered – but perhaps 2020 will bring some clarity.

We partner with advisors and the investors they work with by bringing them innovative investment solutions, excellent asset management and superb service. Our team delivers innovation and expertise through mutual funds, ETFs, alternative investments, private wealth pools and managed solutions. We also offer a charitable giving program and solutions for saving for a child’s education and giving financial assistance to people with disabilities. We strive to bring insights, data and tools to advisors to help them support their clients. For more information, visit mackenzieinvestments.com.

Uncertainty rules the economy

In 2019, issues such as the US-China trade tensions, Brexit and slowing growth worldwide took their toll not only on the global economy, but on Canada’s as well – uncertainty has trickled down to business investment and the demand for Canadian exports.

“I think the biggest impact on global economic activity, and by extension the Canadian economy, has come from the uncertainty and erratic trade policy pursued by the Trump White House,” says Brett House, vice-president and deputy chief economist at Scotiabank. “We are seeing a worsening sentiment hold back business decisions, including purchasing, investing and hiring. This is being driven principally by the uncertainty caused by the White House, their erratic trade war and very equivocal policy-making. We are really looking at a Trump slowdown at this stage.”

House notes that slowing growth in both Canada and the US was expected in 2019, but not at this level. While it’s hard to say where things are headed from here, the tariff situation is something House has been watching.

“We crossed many lines that we didn’t think the Trump presidency was likely to cross,” he says. “On August 1, Trump indicated the US would go ahead with tariffs on the remaining half of imports from China that had not been affected by his special taxes in order to force changes on Chinese trade industrial and intellectual property policies. That was an important line for the White House to cross because the three rounds of tariffs that had been imposed to that point were designed to hit capital and intermediate goods and avoid hitting consumer goods.”

That was a big step, he explains, because it showed that Trump wasn’t afraid to impact consumers by imposing tariffs on items like clothing, shoes, sporting goods, toys and electronics – although he did scale back by postponing the tariffs until December 15, mitigating their effect on the Christmas shopping season.

“The White House is aware of the potential backlash with price increases on consumer goods,” House says. “At the same time, they are showing they are willing to take that risk. It’s hard to predict where things will go when policy is being written by tweet, because some of the limits we thought would govern that policy by tweet have been breached.”

Another issue adding to the uncertainty is Brexit. While House says the UK’s messy divorce from the European Union shouldn’t have a direct impact on Canada, it does contribute to the international climate of uncertainty and could dampen business demands and decisions to purchase goods, hire or invest.

“As an open trade economy, Canada relies on global demand for resources and things we produce,” he explains. “Brexit increases uncertainty around it; it dampens demand for our goods. It may mean that we could see rate cuts from the Bank of Canada to try to insure against spillover into Canada from the Trump-induced slowdown south of the border.”

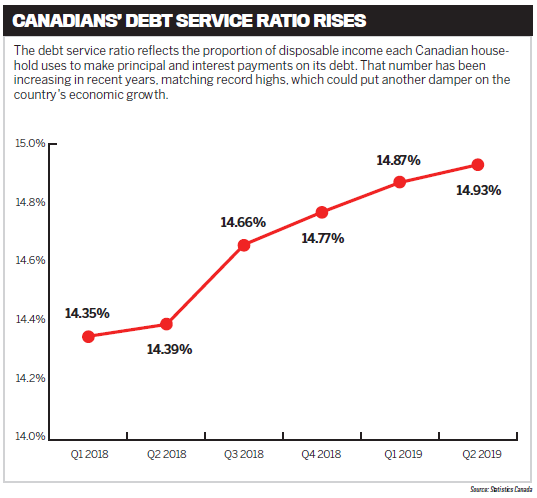

While interest rates in Canada have remained low and Canadians continue to borrow to support the domestic economy, that pattern is unsustainable, House says. Canadians’ debt service ratio is at its highest point in a decade, and the proportion of debt to disposable income is also nearing record highs. Given the high levels of household debt, House says the Canadian economy needs that business investment and demand for exports in order to sustain growth.

Yet even amid the slowdown, he doesn’t foresee a recession because Canadians continue to borrow money to purchase houses, and the country’s major housing markets remain strong. “You look at most of the country, most major cities have markets that are fairly balanced,” he says. “They are not particularly buyer’s or seller’s markets, except for Calgary and Edmonton, where there is supply overhang from the last oil downturn. Toronto and Vancouver are still pretty balanced, but they have low inventory, so you still have supply problems.”

That strength in the housing market, along with a tight labour market, historically low unemployment rates, growing wages and a manageable level of inflation, are all reasons why House doesn’t think Canada is flirting with a recession. However, moving forward, growth will remain muted unless the uncertainty around global events gets resolved.

He notes that it’s difficult to predict what will happen with US trade policy, particularly since 2020 is an election year. As for Brexit, he does believe a resolution is coming, and fiscal stimulus could be applied in Europe to boost growth, which might help to quell some of the uncertainty and get global economic growth back on track.

Alternatives enter the retail market

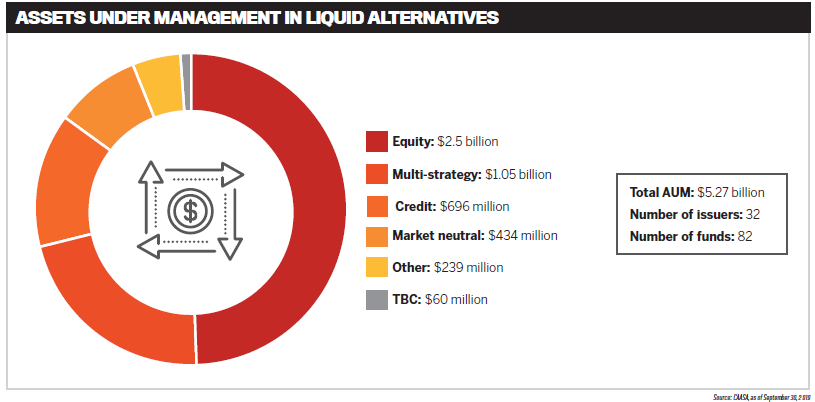

ON JANUARY 3, updates to regulation 81-102 opened the door for alternative strategy products to be offered by prospectus to retail investors. A slew of products subsequently hit the market, and it didn’t take long for them to gain traction with investors. By the end of September, the Canadian Association of Alternative Strategies & Assets [CAASA] had tallied 82 alternative funds on the market with AUM of $5.3 billion.

While 2019 marked the official launch of many of these products, it was something that had been in the works for a while, according to CAASA president James Burron.

“We have been working on this for about six years,” he says. “The predecessor, 81-104 funds, didn’t really get any traction. It was hard to sell, and people really didn’t catch onto it. So they needed a new way to get the strategies out to the market. As well, selling via offering memorandum limited the market to the top 1% of Canadians, which stymied AUM growth for decades. Some funds came out early, and they hit the ground running.

“When the products came out on January 3, there were a couple of big changes. One was that 300% leverage – both long and short – was available to managers, which allowed the funds to produce true hedged strategies. It also excluded the MFDA from it. So right now, it is only the money in the IIROC channel, although that might change shortly.”

Burron notes that AUM in liquid alternative funds doubled between May and September, and he sees assets in these products (both mutual funds and ETFs) reaching at least $20 billion in AUM by June 2020.

“It will gather more steam because advisors, investors and wholesalers will keep buying until something happens,” he says. “Why wouldn’t you buy zero-duration credit funds for your clients? Why would you take any interest rate risk? The equity funds have lower volatility and are less correlated with stocks than traditional mutual fund also.”

As for the timing, Burron says it was simply the culmination of regulators doing their due diligence. “The nice thing is the regulators didn’t want to throw something out there and see how the market would react – they took a lot of care. There were two rounds of comments and letters, and even after all that, the regulators are open to exemptions that would allow structures not explicitly permitted in the rules. It is an open, flexible regulatory regime built to protect investors and get them access to diversifying product.”

Burron says liquid alternative funds and their strategies offer numerous benefits for investors. “Overall, the products have low correlation to the market and low volatility. It’s a good thing for investors to use, and in a crisis, they can make money. There is a restriction on cash shorting, so if the strategy requires more long or short exposure, they can do so with derivatives, such as options, which are a tried-and-true method and exchange-traded, so counterparty risk is taken off the table.”

Right now, Burron believes the biggest impact of liquid alternatives is on advisors who were already familiar with hedge funds, whom he believes will be the early adopters of these products. After that, he believes they’ll move down the line and reach more advisors as they become more familiar.

“When I explain the products, I don’t just position it as, ‘Let’s buy a hedge fund,’” Burron explains. “Instead, I ask, ‘If you have something in your portfolio that should do better in times of market crisis or reduced risk or volatility, isn’t that something you want to have or at least look at?’”

Keeping the conversation simple is key, not only at the product and advisor level, but also when advisors discuss the products with clients.

“I think most advisors don’t talk about the product, but rather what it can do for the client: defence, income and growth,” Burron says. “That is what clients can digest more readily. I think that is the correct positioning – talking about the benefits of how it works and not getting too bogged down in the structure that much.”

Burron acknowledges that part of the conversation has to be about the risks involved. “People should know that there is shorting involved – shorting by itself, just like using derivatives and leverage, can be risky,” he says. “But when used in a portfolio setting with many securities, you generally get lower volatility at the portfolio level for the fund, and the fund has a lower correlation to other assets – that’s what most people are after. In 2008, when markets were down 40% to 45%, hedge fund indices were only down 20%, just when this protection was needed most.”

Burron adds that it’s also important for advisors to understand that unlike mutual funds, which generally track the market and each other, “between alternative strategies there is low correlation, and even within strategies, the individual funds have different return characteristics. Two managers in the same strategy may have very low correlation, which you just don’t find in long-only worlds.”

Moving forward, in addition to a goal of hitting $20 billion in AUM by June, Burron also believes there will be more liquid alternative products developed – particularly products issued by Canadian distributors using foreign asset managers. The market hasn’t seen much in that area yet, but he thinks that could change in 2020.

And as the economic cycle enters its later stages, liquid alternatives are poised to showcase their worth. “If we have a crisis and they don’t lose as much – which I think will happen – and advisors see them holding up, then you’ll see more allocation to them,” Burron says. “Advisors will move into strategies they are most comfortable with and branch out from there.”

Central banks reverse course

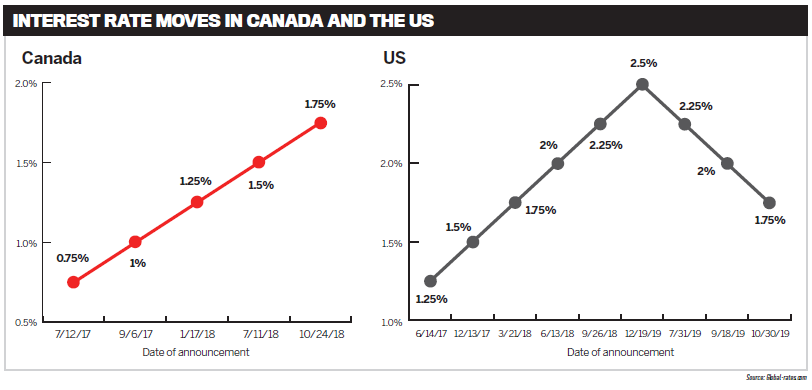

Back in the summer of 2018, the US Federal Reserve announced plans to raise interest rates a couple more times that year and then up to three times in 2019. That had many experts anticipating that rates in the US would reach 3% to 3.5% and the trickle-down effect would cause rates in Canada to jump to 2.5% to 3%. But as trade disputes raged on and global growth slowed, the Fed reversed its decision in mid-2019 and began cutting rates in an effort to calm the market.

Meanwhile, the Bank of Canada stuck to its guns, believing that stimulus needed to be removed from the market. However, as trade and economic issues started to take hold, the timing of the removal of stimulus was up for debate.

In 2019, the Fed made three interest rate cuts for a total of 75 basis points. While the Fed indicated at its October 30 meeting that it might put a hold on monetary policy, there could be more cuts in 2020. And while the BoC has held its rate at 1.75% for the entire year, if the impact of slowing growth begins to seep deeper into the national economy, Canada could also see a cut or two in the next year.

“Both the Canadian and US bond markets have priced in cuts,” says Brian D’Costa, founding partner and president of Algonquin Capital. “The big issue is trade because it is resulting in weaker business confidence. The drag on growth is real – as long as the trade issue lingers, the cuts will come. If there is a deal [between the US and China], then you could see it slowly go the other way. Also, a deal between the UK and EU could help a recovery in business confidence. Central banks are being patient – we are not likely to see hikes until we see the yields back up to 2% in the US and 1.75% to 2% in Canada.”

While D’Costa was surprised by the Fed’s rate cuts, he says the speed at which business confidence has weakened was more of a shock. “I thought we would see price pressure in the [Consumer Price Index], but we saw very little. So I was a little caught off guard by how global growth tailed off.”

A trend that has become more apparent recently is central banks’ proactive stance in their policy decisions, which D’Costa attributes to their sensitivity to deflation.

“The bias now with central banks has shifted since the 2008 crisis,” he says. “They are more sensitive towards deflation than inflation. It means they are quicker to ease and slower to hike. Conditions to achieve high inflation are now more difficult.”

As for why the BoC failed to mirror its US counterpart and cut rates here in Canada, D’Costa believes it’s because the Canadian economy is largely buoyant.

“I wasn’t too surprised they didn’t follow suit,” he says. “The Canadian economic numbers are not tremendous, but they are stronger than forecasted. The drag is mainly on the oil sector. The BoC is essentially saying they can’t make rate cuts just for one sector. Right now, we have an overindebted consumer and high housing prices. If there were more cuts, it could add to those risks.”

Still, the BoC might not have a choice in 2020 if the economic slowdown extends past the oil sector. “[The BoC’s] story for a while has been that it’s not too bad,” D’Costa says. “However, the risk is that Canada could be sideswiped by the trade disputes, which could result in the rest of the economy slowing. A BoC cut could offset a slowdown in other sectors. I think the main thing to watch is currency – the Canadian dollar has been pretty consistent, but if it were to strengthen, we could see rates rise again.”

Heading into 2020, D’Costa sees a couple of potential scenarios. “I think if we see a trade deal reached, just any deal that adds clarity, you won’t see more rate cuts here or in the US. If no deal is reached, the Fed will probably cut twice in 2020. I think the BoC will probably have one or maybe even two cuts in 2020. It all comes back to business confidence. It’s hard for companies to make decisions when they don’t know what the rules are going to be. Any clarity will bring that confidence back up.”

ETFs continue to dominate

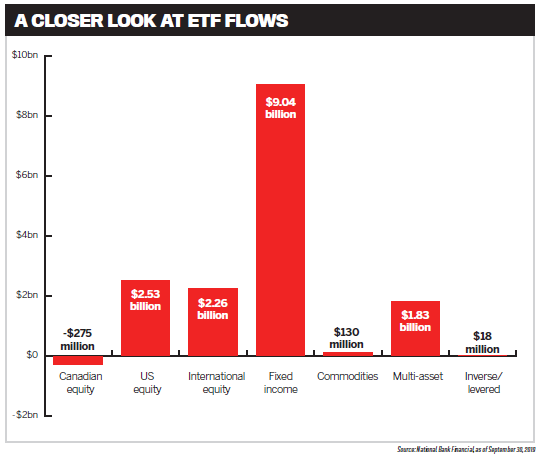

It was a big deal in 2018 when Canadian ETFs outsold mutual funds for the first time in a decade. As ETFs continue to gain popularity with investors who want lower fees, DIY strategies and access to different sectors, the preference for ETFs shows no signs of waning. As of September 30, ETF inflows had already reached $16 billion, compared to $9.1 billion for mutual funds, according to National Bank Financial and the IFIC.

“There were a lot of events going on for the ETF industry in 2019,” says Steve Hawkins, president and CEO of Horizons ETFs and current chair of the Canadian ETF Association. “We had RBC and iShares announce a partnership, the federal budget wanting to change how ETFs were taxed, a call to action with respect to fees, a significant move of new ETFs into the active management space – more than 50% of ETFs launched in the past year have actively managed mandates – and now you have every bank and large asset management company in the ETF space.”

While Hawkins is pleased to see ETFs continue to outsell mutual funds, he points out that Canada has been a laggard compared to the rest of the world – ETFs have been outselling mutual funds for years in the US and globally.

“Here in Canada, we have a longstanding, entrenched mindset of mutual fund investors because of the banks,” he explains. “The banks control a significant portion of distribution in Canada, and being able to sell mutual funds in a bank branch makes it easy. As long as we have banks selling mutual funds actively, the outselling of ETFs over mutual funds won’t be as large in Canada, from a spread perspective, as it is globally.”

Still, Hawkins does believe ETFs will continue to gain ground on mutual funds because of their lower fees. “We have also seen a huge trend that Canadian investors are taking charge of their own investments more,” he says. “We have seen a big shift of Canadian investors to the self-directed channels. There have been huge increases of ETF assets in these channels themselves, as these self-directed channels are now very actively buying ETFs.”

The RBC/BlackRock iShares partnership kicked the year off with a bang. While the announcement itself surprised Hawkins, the partnership didn’t.

“It wasn’t a surprise because BlackRock had, from our perspective, changed the way they were doing business in Canada with iShares,” he says. “They weren’t actively selling their ETFs into the retail channel. It looked like they were looking for a partner in Canada to help with their business. They found RBC, the largest investment advisor channel, who were in ETFs already but created this partnership.”

Hawkins notes that the partnership reaffirmed BlackRock’s position as the top ETF provider by AUM and, at the same time, opened the door for more partnerships of this kind in Canada.

“The banks, outside of BMO, have been slow to enter the Canadian ETF marketplace,” he says. “CIBC and National only entered in the past 12 months. Fidelity only entered in the past 12 months. These are large asset management companies with huge client bases. So now the question is whether they want to solely grow their asset base organically or potentially partner with or acquire ETF providers. That is something that remains to be seen. I would not put it out of the realm of possibility.”

In terms of ETF asset classes, 2019 saw a big push toward fixed income. As of September 30, fixed income ETFs alone had racked up inflows of more than $9 billion.

“There has been a lot of uncertainty in the capital markets with respect to interest rates,” Hawkins says. “With interest rates and the prospect of more cuts, there have been significant assets moving into long-term bonds that pay higher interest rates and can take some credit exposure while earning a nice yield. I don’t think that trend will change, either, unless we see significant changes in interest rates or the marketplace.”

Now that the ETF industry has more than $188 billion in assets and 35 providers, Hawkins has his eye on the bottom tier of providers going forward. He says the industry doesn’t need a glut of similar products, but as more large financial institutions enter the space, duplication is likely. So will the smaller firms be able to remain profitable, or are there more acquisitions and partnerships in the cards?

“It is difficult for asset managers to enter the space without the backing of a large asset management company,” Hawkins says. “Their ability to sustain their operations becomes difficult. We always welcome new entrants but are very cautious with respect to who they are.”

'

'

The market cycle enters the later stages

It was another interesting year in the markets. A decade after the 2008–09 financial crisis, the longest bull run in history raged on. Yet 2019 was also marked by volatility, stemming from the ongoing trade dispute between the US and China. Being in the later stages of the cycle means things in the markets could change quickly – something investors had plenty of chances to witness in 2019.

“The past 12 months, even dating back to Q4 of 2018, saw high volatility,” says Francis Sabourin, director of wealth management, portfolio manager and investment advisor at Richardson GMP. “The systems in place now were trading out and down on everything. Now, there is no debt in the market, as market makers are staying away. That’s just normal in the end of a business cycle. This type of market can change quickly, so you need to be diversified in many sectors. You must also stick to your investment objectives and conform to your investor profiles. Trying to time the market is one of the worst things you can do.”

With 27 years in the business under his belt, Sabourin has seen many cycles come and go, but he says this one is different. “This is not a regular business cycle; it is very unpredictable. What has been unique is the rebound has been slower. Central banks and their quantitative easing policies have tried to extend this run. It hasn’t been a boom and bust, like in the past. This time, there was a little boom that kept going. There are many new tools, such as alternative approaches and buybacks, that have also helped keep the cycle alive."

Sabourin also points to the speed at which information is consumed as a unique element of this market cycle. “In this cycle, the news is so fast, it is very impactful,” he says. “Before, we used to get the data, analyze it, write about it, read it and then implement our conclusion. Now, it happens in a nanosecond. If there is a tweet, there is new data. The world is faster than before.”

Even with the volatility in 2019, Sabourin says the year has brought some pleasant surprises in the markets. “I was surprised by the returns of the TSX and S&P 500,” he says. “Also, the bond market did quite well. Last year, we were expecting interest rates to be higher, which resulted in a negative or flat curve in some areas. This year, we were caught off guard because the bond yields have been higher than we thought, especially when you consider the negative yields we have seen in European countries. Canadian and US bonds have still been strong – maybe that has been because Europe has had to look to North American bonds to find decent returns.”

Still, Sabourin sees the late stage in the cycle for what it is and knows things can turn on a dime. And, he says, all the noise out there only increases the possibility of a recession.

“Unless a resolution to the trade situation is found, this global noise is getting heavy on companies and governments,” he says. “It is forcing them to prop up their economies and make sure people have jobs, consume and spend. Employment rates and consumer confidence were still positive as of September, but manufacturing has slowed down. I am not sure if this is just a blip or a trend. You can be in a recession quickly, and it takes time to get out. Sometimes you may already be in a recession but don’t realize it until later.”

Sabourin will be watching closely over the next few months, as events in the near future could determine which way the cycle goes. If a trade agreement can be reached, for instance, it could bring back confidence in the economy; otherwise, it could get quite negative.

“Everything will be slowing down; overall, we feel the economy is slowing down,” he says. “It all goes back to trade. The US really needs to get serious about this – it has been volatile for both sides. That means right now we obviously need to be cautious and be able to deploy money to take advantage of any sell-off in market. We are in a situation where it’s not time to be a hero – we need to be cautious of the reality we are facing. But it could all change on a dime. A trade agreement could re-establish positive sentiment of the economy and the market to extend the run.”

Multiple sectors make the news

Unlike in 2018, when the investment world was obsessed with what was happening in the cannabis sector, 2019 provided a more diverse set of headlines. Cannabis remained in the news, but more for the fluctuation of stock prices as companies adapted to legalization. Technology remained top of mind as the major players kept pilling up cash, resulting in dividends and buybacks. Cryptocurrencies also continued their rollercoaster ride, while sectors like healthcare and energy took hits.

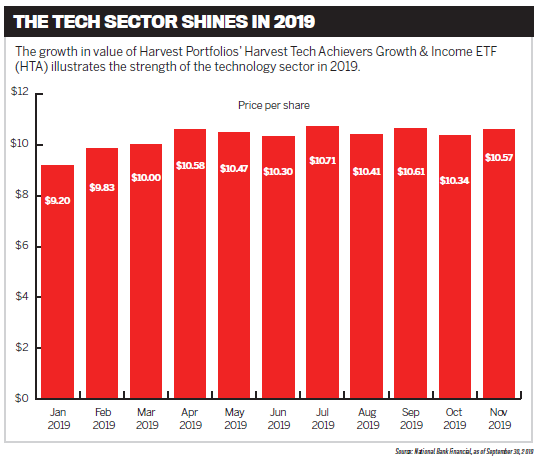

“It has been an interesting year for sectors,” says Michael Kovacs, president and CEO of Harvest Portfolios. “The top three were tech, REITs and utilities. For REITs and utilities, it was caused by interest rate sensitivity, with many investors moving to more secure, or at least perceived more secure, sectors. Technology was a star in 2019, with goodquality companies generating dividends. We never thought, years ago, that they would turn into the dividend payers that they have.”

Kovacs notes that it’s not uncommon to see such movement in various sectors; that’s why his company takes a long-term approach by owning solid companies. That philosophy has paid off, as Harvest continued to see flows into its funds. Yet Kovacs says it’s been more interesting to see which sectors struggled in 2019.

“Healthcare and energy got hit hard, while materials were beaten up,” he says. “People turned away from energy as a less desirable sector to own in portfolios. For healthcare, we still think it is a fantastic sector and a global phenomenon, but there has been so much rhetoric surrounding the US election – it may take a year or so until it gets back on track.”

Oil also proved to be an interesting sector to watch in 2019. OPEC announced it was extending production cuts, which are set to continue into 2020. In September, there were attacks on a Saudi oil facility and oil fields, which affected global supply. Yet Kovacs still sees potential for energy, at least in the short term.

“Long term, I think oil production will top out,” he says. “Saudi Arabia and other oil producers are looking to max their oil price and production while they can. The attacks were a sign of the geopolitical climate, but there wasn’t a sustained jump in prices that resulted from it, which shows the amount of supply. Even in Canada, our biggest customer for oil, the US, has gone from a net importer to a net exporter. So, we see the prices remaining around $50 to $60 a barrel for the near future.”

Another sector Kovacs sees staying around is cannabis, despite its ups and downs during the year. Canopy Growth, for instance, saw its stock rise to almost $70 in May before plunging to the high $20s and low $30s in the fall. While Harvest’s funds don’t directly hold cannabis companies, Kovacs has been keeping an eye on the sector.

“It is definitely a developing area, but it’s still in its early days,” he says. “There are legislation and political risks in the US, but it is not going to go away and should continue to grow. I think it may have just gotten a little ahead of itself based on legal changes in Canada.”

One sector that saw even more fluctuation was cryptocurrency, illustrated by Bitcoin, which was valued at just over $3,300 in February, skyrocketed to nearly $13,000 in June and then dropped to the $8,000 range in the fall. Harvest does have a blockchain fund, and Kovacs says it has seen some fluctuation because the two tend to get lumped together.

“Blockchain as a digital technology will continue to grow, which we have seen within the companies of our fund,” he says. “Crypto uses the blockchain technology, so the two are coupled. I think there were too many cryptocurrencies too quickly, and eventually we will end with a few, Bitcoin and maybe Ethereum being two of those, and there will be additional regulation and standardization. I do see a future for it, but much like any new technology, it takes time to work out the kinks.”

Based on where the economic cycle is, Kovacs believes quality companies will continue to see interest in the near future – along with an old staple. “One sector that also did well in 2019 is gold, up 17% to 18% for the year,” he says. “The fact that we are in the later stages of the economic cycle and gold is up is something that should continue next year. With a US election next year, I think investors will continue to be cautious. Many investors are waiting on the sidelines, being conservative and holding more cash until they see what happens.”

Over the past year, Canadians have seen several significant tax developments. While not all advisors put tax planning front and centre in their practice, it is an essential area that can help increase an advisor’s overall value proposition.

Aaron Hector, vice-president and financial consultant at Doherty & Bryant Financial Strategists, is one advisor who believes in putting tax at the forefront. While he has observed numerous developments in this area over the past few years, there were a few that stood out for him in 2019.

“In my mind, the most significant changes introduced in the 2019 federal budget were an annual cap of $200,000 to employee stock option grants, the introduction of advanced life deferred annuities [ALDAs], an increase in the Home Buyers’ Plan from $25,000 to $35,000, and the introduction of minor tax credits such as the Canada Training Credit and a tax credit for digital news subscriptions.”

When it comes to the stock options grants, Hector says he’s still waiting on some of the fine details but expects the rules to be finalized before the changes are effective in January. As for the ALDAs, he notes that this will allow Canadians to transfer up to 25% of their RRSP/RRIF into the purchase of an ALDA, which allows the income to be postponed out to age 85.

“There is no question that ALDAs will add further flexibility and tax planning options into the retirement income planning landscape he says. “I see ALDAs as a tool that could be used to potentially plan around OAS clawbacks. If priced fairly, these new annuities do have the potential to be a significant planning tool going forward.”

Hector is a big proponent of taking an involved approach to clients’ tax situations. His firm also prepares tax returns for clients, giving him insights into their marginal tax rates, RRSP contribution room, TFSA room, carry-forward losses from other years, repayment obligations under programs such as the Home Buyers’ Plan or Lifelong Learning Plan, their philanthropic interests, and any other credits they’re eligible for.

“You really need to have a solid understanding of where the client is heading in the future,” he explains. “If I know that someone is going to be in a higher or lower tax bracket in the future, then that’s going to have an impact on my recommendations for when to make RRSP contributions and whether to proactively trigger capital gains or losses. Knowing the long-term income and tax situation is also important for advisors who are talking to their clients about modelling how best to map out their retirement income. There are lots of decisions that inter-relate, such as when to start CPP, OAS or draw down RRSP/RRIF assets.”

One area that Hector highlights is TFSAs; he says many investors aren’t fully using them or are simply using them as a high interest savings account and aren’t buying securities within them.

“Quite often, employees who participate in a stock matching program will forget about their shares and leave them in the plan,” he says. “When the shares vest, they should be moving them into a TFSA – if they have room and they want to continue to hold the shares – instead of leaving them inside the nonregistered plan set up by their company.”

Hector attributes this to a lack of tax knowledge on the part of investors, making it even more important for advisors to familiarize themselves with strategies for constructing tax-efficient portfolios. Hector and his team use a wide range of strategies to address the ever-evolving tax landscape, including tax splitting between spouses, keeping tabs on the age of their clients so they can implement new credits as necessary, examining the best ways to achieve philanthropic goals, finding ways to help convert non-tax-deductible debt into tax-deductible debt, and reviewing overall situations annually.

Hector foresees 2020 being just as eventful as 2019 in terms of tax changes. In the run-up to the election, the Liberals outlined a plan that included increasing the basic tax credit from $12,069 to $15,000, imposing a federal tax on non-residents who own vacant real estate, increasing OAS benefits by 10% for seniors over 75, increasing the CPP survivor benefit by 25%, expanding the Canada Child Benefit to add another $1,000 benefit for children under age 1, and decreasing before- and after-school care costs.

As with any election, it’s anyone’s guess as to whether these campaign promises will be put into action, but with so many plans in the works that directly affect tax, 2020 should be an interesting year for advisors on this front.

Data leads to strides in ESG

Investors are increasingly putting their money into funds that focus on companies with positive environmental, social and governance criteria: Responsible investment assets in Canada surpassed $2 trillion in 2018, up from $1.5 trillion in 2015. The area has seen significant momentum as ESG moves from being simply a thematic or satellite position in portfolios to the core itself. While Europe was an early adopter of this type of investing (at the start of 2018, assets in sustainable and responsible investing in Europe were at $14.1 trillion), ESG is becoming central in North America as investors realize they don’t need to give up returns to integrate it into their portfolios.

"There have been more pushes and drivers to make ESG investing more mainstream,” explains Mona Naqvi, senior director of ESG indices at S&P Dow Jones Indices. “Corporate data is one way that it has been made more transparent.”

Naqvi believes this increased access to data has been key in the growth of ESG investing, as it makes it easier to analyze the activities of a company so investors can determine whether they agree with that company and want to include it in their portfolio. The data also makes it easier to adjust weightings or tilt in a given direction.

The demand for ESG, Naqvi says, is largely being driven by asset owners. “When you look at European public pension funds, they require ESG mandates,” she explains. “The ecosystem is creating a trickle-down effect. More investment mandates lead to demands for transparency from companies, which leads to corporate disclosure and results in ESG integration. That has been the trend of the last five years.”

The rise in ESG growth can also be attributed to factors outside of just the investment world. As more governments sign on to things like carbon reduction agreements, it impacts individual companies – when heavy carbon users face significant taxes, it makes them more costly to own.

Although it’s gaining popularity, Naqvi notes that ESG investing isn’t mainstream among retail investors yet, which she chalks up to a lack of education and awareness.

“Many people interchange ESG with socially responsible investing,” she says. “Yet SRI is associated with values and implies you need to give something up with the return. ESG encompasses SRI but is much more. It’s a combination of values and financial material. Many people still believe to do good with investments, you need to give something up. However, with the data available today, it’s not the case anymore."

Moving forward, Naqvi believes ESG has a long way to go. She says a new concept has begun to gain traction in the space: social impact, which refers to investments made into companies, organizations and funds with the intention to generate a measurable, beneficial social or environmental impact alongside a financial return. However, she feels this concept is still a few years away from becoming mainstream.

In the short term, exciting developments in the ESG space include artificial intelligence and Big Data, which are providing even more information as to how companies are valued. Naqvi adds that tools and products such as the S&P 500 ESG Index are also helping to make ESG more popular.

“I think we will see deeper integration of ESG in areas, and in some areas, we may even see social impact,” she says. “Overall, I think we will see deeper ESG integration thanks to the availability of data.”