From rising interest rates to headline-grabbing cannabis stocks, 2018 had no shortage of events that impacted the financial world

In 2018, every day seemed to bring new developments to the financial industry. Advisors had to navigate numerous issues on both the national and international level to ensure they were doing the most for their clients.

Here in Canada, the CSA proposed a ban on deferred sales charges, forcing some advisors to re-evaluate their own practices. The country’s greying population prompted an increased focus on retirement preparation. Cannabis legalization, which became official on October 17, also made its presence felt in the market, as Canadian cannabis stocks frequently posted huge gains and losses overnight.

Advisors were also forced to contend with volatility in 2018’s other hot sector: cryptocurrency. In both the US and Canada, interest rates continued to rise and fund providers continued to try to outdo each other by lowering management fees. Meanwhile, outside of North America, emerging market economies took a hit. As a backdrop to all of this, the bull market raged on, prompting experts to try to predict when it will end.

On the following pages, Wealth Professional Canada talks to experts from across the wealth management spectrum to get their insights on the trends that defined 2018 and how they might continue to reverberate in the year ahead.

The race to slash fees intensifies

Fees were at the forefront of the investment industry in 2018. After years of evaluation, the CSA released a report in June outlining a proposal to eliminate deferred sales charges, among other things, sparking intense debate among advisors about the merits and pitfalls of DSCs. In September, the Ontario government came out with a statement against the CSA’s proposals, further stoking the flames of the debate.

Meanwhile, fund managers continued to slash their own management fees. Companies such as Vanguard, BlackRock, Fidelity. Horizons and others kept moving their fees lower and lower in anticipation of more advisors switching to fee-based models. In August, both Fidelity and Horizons launched products boasting 0% management fees, changing the way investors look at funds.

Atul Tiwari, managing director at Vanguard Investments Canada, has been monitoring the situation throughout the year from both a product and investment standpoint. He welcomes the CSA’s proposal, calling it “a positive sign for the investment industry in terms of improving fee transparency and making investment fees more aligned with the interests of Canadian investors.”

Tiwari notes that Canadians pay some of the highest investment fees in the developed world and believes the CSA’s proposal will not only provide greater fee transparency, but also address certain conflicts of interest related to the sale of funds in Canada. “We feel strongly that investors are best served in an environment in which fees are clear so that they can properly assess the true cost and suitability of each investment,” Tiwari says.

As more advisors move toward fee-based models, Tiwari believes this will bode well for low-cost ETFs and mutual funds. “The investment industry, particularly ETFs, has experienced exceptional growth over the past few years,” he says, “and while the proposals stopped short of an outright ban on embedded commissions, there is already a strong organic shift towards fee-based rather than commission-based financial advice models. It’s clear that Canadian investors and regulators are becoming more aware of investment fees, which is positive, since research has shown that one of the best predictors of future investment performance is the cost of the fees you pay. This will continue the drive to lower-cost ETFs and mutual funds.”

One thing that could offset the current direction is the position of the Ontario government. Tiwari believes it’s still too early to comment on the government’s statement as Vanguard, along with others in the industry, assess the impact. While some in the industry are against the banning of embedded commissions on the basis of making financial advice accessible to all Canadians, if more products at or near a 0% fee continue to come to market, the industry could be looking at a sea change.

ETFs keep the momentum going

It was another strong year for the Canadian ETF industry, which has grown by leaps and bounds in recent years. Over the last six years, the number of ETF providers in Canada has jumped from five to 30, and ETFs continue to rake in assets – the Canadian ETF industry now boasts more than $163 billion in AUM.

Pat Dunwoody, executive director of the Canadian ETF Association [CETFA], is understandably pleased with the increasing popularity of ETFs. “The growth in 2018 has been tremendous,” she says. “The year-overyear growth continues to be 20%, so we can’t complain about growth.”

One initiative the CETFA undertook in 2018 was an investor research study, which found that many investors still are not aware of ETFs and what they can offer.

“We need to make a greater effort to raise awareness and inform them about the product,” Dunwoody says. “The industry is still quite small compared to the mutual fund industry. If clients’ accounts have done well with mutual funds, they have been reluctant to switch to ETFs. Until all advisors switch to fee-based accounts, it won’t really be an option. As the investment population begins to understand the impact of costs and fees, ETFs will become more of an option, but in a bull market, there is less necessity to look at the products.”

A major trend in 2018 was an increase in actively managed ETFs, something that wasn’t surprising to Dunwoody. “The firms that have been launching active products have a background in actively managed mutual funds, so it was a natural progression,” she says. “I hope the AUM growth continues so that ETFs can get to more investors.”

She also notes that fixed-income ETFs saw increased inflows in 2018 as investors began to view them as an easy way to incorporate fixed income into their portfolios.

One dark cloud for Canada’s ETF industry in 2018 was a decline in sales between the first and second quarter. However, Dunwoody attributes this to rebalancing and money moving between ETFs, and is optimistic that sales will rebound before the end of the year.

Heading into 2019, Dunwoody believes at least one more provider will enter the market, perhaps a bank. “I believe we will see the banks that haven’t already launched products do so either before the end of the year or in 2019 so that they can have them on their shelf,” she says.

All signs point to more growth for ETFs going forward. “The ETF industry is still only 10% the size of the mutual fund industry,” Dunwoody says. “If and when advisors start to switch to a fee-based model, ETFs will become more of an option. I think we will see more transfers to ETFs, and new money coming into the system will go into ETFs. As market growth slows, cost will become an issue, and that’s where there is opportunity for ETFs.”

Dunwoody also believes the next generation of investors will continue to propel interest in ETFs. The largest wealth transfer in history between baby boomers and millennials is on the horizon, which could make ETFs the primary vehicle for investing. However, Dunwoody thinks that shift still may be a few years off.

“People are living longer, so the [wealth transfer] is not only coming later, but will be smaller,” she says. “One thing we have noticed is that when we speak at universities, close to 100% of the students who invest say they invest in ETFs, and only a small percentage in mutual funds. That leads to the assumption that the transfer of inheritance will be to ETFs.”

Part of the reason Dunwoody sees new investors gravitating toward ETFs is their simplicity – a benefit that she believes will help awareness of ETFs continue to spread. Dunwoody also believes 2019 could bring MFDA involvement in ETFs, which she thinks will help on the distribution side.

“Now the industry has enough firms, and with mutual fund companies getting involved, they have the ability to market the products,” she says. “ETFs need to be marketed differently to advisors. The more firms that are talking about ETFs, the more it will help the industry.”

Cannabis sector commands headlines

You couldn't look at anywhere in 2018 without finding news of developments in the cannabis sector. As Canada’s October 17 legalization date drew near, the subject became more mainstream, leading to more institutions and corporations entering the industry to work with growth companies.

As CFO and portfolio manager at Faircourt Asset Management, Doug Waterson oversees the Ninepoint Alternative Health Fund, which was the first mutual fund in Canada to incorporate cannabis- sector investments. He acknowledges that 2018 was an eventful year, adding that the elimination of the stigma around marijuana has been integral to its success.

“I think 2018 can be looked at as the year cannabis became mainstream,” Waterson says. “We have had a variety of things that happened – full legalization on October 17, [which means] 39 countries now have some form of legalization, including 20 of 28 in the European Union; increased interest from investors, including those in the US, since US companies can’t list; pressure for pharmaceuticals, alcohol and tobacco to get involved; and even more research into what the plant can do.”

Canopy Growth Corp. grabbed the bulk of headlines in 2018. In January, the cannabis producer reached an agreement with BMO to co-finance the company. “This was significant,” Waterson says. “BMO was the first major bank to participate in a cannabis company. I think you will see more banks follow.”

Canopy also listed on the New York Stock Exchange in August, providing US investors with access to the sector. The company followed that with a $5 billion investment from Constellation Brands, the maker of Corona, which was the first of many partnerships in the sector – other links include Molson Coors and Hydropothecary Corporation, as well as Coca-Cola and Aurora Cannabis.

“All of [Canopy’s] developments have really energized the sector and led to speculation about who’s next,” Waterson says. “I think it all opened people’s eyes, and many investors are interested.”

In a sector that has so many moving parts, Waterson says the only thing that really surprised him in 2018 was the pace at which things happened. In particular, he points to the example of producer Tilray, whose stock shot up to $214.06 in September, only to sink to $100 days later.

“The speed of changes and regulation was pretty staggering – not just in Canada or the US, but everywhere,” Waterson says. “In certain cases, such as Tilray, there was also some degree of surprise. That trade price was just a perfect storm, combined with positive press in the US and a really thin float.”

Even with the volatility the cannabis sector has exhibited, Waterson still sees opportunity, but he believes investors need to be on the lookout for certain things.

“First, look at where we are,” he says. “We are out of the startup phase and in a more developed market. Management is important because there are a variety of factors to look at such as regulation, branding, opportunity and supply chains. The other thing is to carefully understand a company’s business. Investors need to understand what boxes they have checked off with things like supply contracts, branding, etc. The market won’t pay for just production much longer.”

That thinking is something Waterson incorporates in the Ninepoint Alternative Health Fund, which has grown significantly in 2018 as more advisors become interested in the cannabis sector. He adds that active management has been key to successfully navigating the shifting fortunes of this industry.

“Actively managing it allows us to be more specific than an index and avoids overvaluing something,” Waterson says. “When you look at a Canopy or Aurora, they trade at a premium. We see value in smaller companies and can overweight those names. I still think there is room for investors to make money, but perhaps not by buying and waiting. You need to be active and participate in new things like emerging extraction companies retail and labs.”

With so much activity in the sector, Waterson expects a lot to happen in 2019. “I think trends ... like strategic investing by alcohol, tobacco and pharmaceuticals companies will continue. We will see more medical legalization and further movements in the US towards not full legalization, but Band-Aids around the national/state system. Here at home, I think the rollout will be underwhelming; I don’t think the provinces are truly ready – 2019 will sort out the issues, and the market will evolve, but there will be hiccups. I think technology is also going to help grow the industry and bring costs down.”

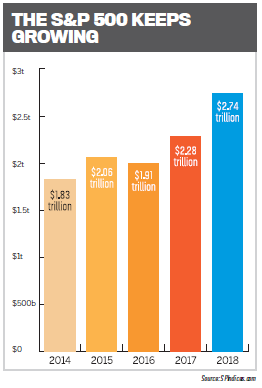

The bull market rages on

Despite news of trade wars, political investigations and a flattening yield curve, the bull market persists. While experts continue to debate when the current run will finally end, Wolfgang Klein, SVP and senior investment advisor at Canaccord Genuity Wealth Management, believes we’re not there yet.

Despite news of trade wars, political investigations and a flattening yield curve, the bull market persists. While experts continue to debate when the current run will finally end, Wolfgang Klein, SVP and senior investment advisor at Canaccord Genuity Wealth Management, believes we’re not there yet.

“It tends to end when earnings roll over,” he says. “Earnings are rising, so we have positive earnings growth, not negative. More importantly. it ends when people take money out of the system by inverting short-term interest rates above long-term rates, inverting the yield curve, and we are not there yet.”

The yield curve did flatten in 2018 as 10-year bond yields moved higher than 30-year bonds, sparking fears that a recession was on the way. However, Klein disagreed. “The flattening was between the 10- and 30-year bonds, but the two- and 10-years still had some steepness to them, although the spread was narrowing,” he says.

And, he points out, the flattened yield curve eventually corrected itself. “Equity markets continue to rise,” he says. “Interest rates are still very low, and they aren’t going to run away on us. There may be a few more rate hikes, but even when you factor them in, earnings yield is still higher than the 10-year Treasury, giving equity premium, so it justifies why you can own stocks.”

Klein believes the market will finish the year with a late rally, but he isn’t overly concerned about the short term, as he’s more focused on investing his clients’ money over the long term. “If you look at a long chart of the S&P 500, the 1987 crash is blip on the screen – the market is very resilient,” he says.

Klein does admit the market holds surprises every day, and he observed a few in 2018. “Manulife was a surprise recently with a new case of a hedge fund going after one of their products,” he says. “Donald Trump surprised me every couple weeks, and the marijuana craze is interesting. At the end of the day, what I need to do is buy quality businesses for my clients that will grow revenue, grow earnings and appreciate in value over time. Good things happen to good companies.”

Predicting when the current bull market will end is nothing but a guess for Klein, although he does have a mathematical approach to making such a prediction.

“To put the economy into recession takes time,” he says. “For them to flatten the yield curve would probably take three rate hikes. To invert it could take another two or three. So you have five or six rate hikes to invert the yield curve. You don’t go into recession right when the yield curve inverts. The market continues to rally after because shadow banking kicks in. With that kind of math, you could suggest 18 months to three years.”

While Klein leans towards the two-year mark, he adds that anything could stop the economy. But no matter the situation, Klein believes his strategy of cutting through the noise is the best way to prepare for whatever the market has in store.

“We focus on buying quality businesses with good balance sheets – businesses we understand and hold through the noisy periods,” he says. “If you have a value buy, you’ll never ... have trouble making money.”

For 2019, Klein believes the best days of this bull market might be yet to come. “There has been no euphoric buying – a few sectors have, but overall, the stock market is not overly loved,” he says. “That leads me to believe that perhaps the best is still in front.”

Interest rates continue to climb

Both the US and Canadian economies remained strong in 2018, leading both the Bank of Canada and the US Federal Reserve to raise their interest rates. In Canada, the first 0.25% hike happened in January, followed by an additional 0.25% in both July and October to bring the rate to 1.75%. Meanwhile, in the US, the Federal Reserve raised rates for the third time in 2018 in September, bringing their short-term rate to 2.25%. More rate hikes are expected in the near future in both countries, leading some experts to wonder when consumers will begin to feel the pinch and how much it will affect the economy.

“We thought two hikes at most would be delivered by the Bank of Canada,” says Aubrey Basdeo, head of Canadian fixed income at BlackRock Asset Management. “We were a bit surprised about the change from the first half of the year to the second. We are worried about the removal of accommodation because the economy is operating above capacity, all of which is from the second-quarter growth.”

Basdeo believes the BoC should exercise more caution because as the US removes accommodation, it will affect global economies. “When you look at emerging markets, and to some extent Europe, the liquidity drain initiated by the US Federal Reserve – not just in hiking rates but in quantitative tightening – is setting off trip wires because they must wait and see how the economy reacts before instituting another rate hike.

“They aren’t trying to slay the consumer,” he adds, “just have growth continue without triggering an inflation outbreak, but it is a delicate balance. One too many hikes could have negative consequence if it affects consumption, and ultimately you’ll see real estate asset prices have a negative reaction. That feeds into confidence and is the negative loop that happens.”

In the short term, Basdeo believes that rates will rise to 2% in Canada in January 2019. He also believes the US will see one or two more hikes in 2019 before a pause. “Our forecast, when we look at GDP globally, is it has been slowing since earlier this year,” he says. “That would suggest the economy can withstand these modest rate increases. When you parse the global growth number, it is mainly the US contributing to the strong outlook. The rest of the world has been struggling. So will the world drag the US down, or will the US pull the rest of world up?”

The answer, for Basdeo, lies what happens in terms of free trade, open markets, free flow of goods, trade wars and geopolitical uncertainty. If trade wars, tariffs and uncertainty prevail, Basdeo says that will lead to portfolio construction that’s focused on resilience rather than aggressive growth.

Moving forward, Basdeo continues to stress caution for investors as rates increase. He advises a ‘wait and see’ approach as rate hikes spill into other parts of the economy – in particular, the Canadian housing market and the US auto and student loan spaces.

“The removal of accommodation has the potential to set off unintended consequences, and that’s our point about portfolio resiliency,” he says. “Even though we see relatively strong growth and the US being a driver, the distribution around the profile has widened based on how much uncertainty has risen in the last six months.”

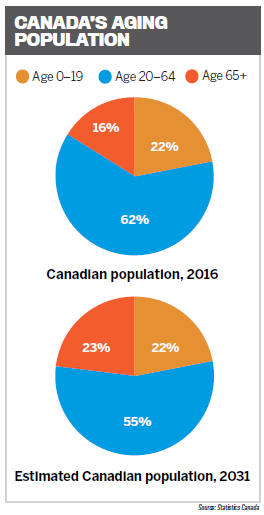

Retirement dominates financial planning

The importance of planning for the full duration of retirement has never been greater. While most clients don’t underestimate the planning itself, Chris Poole, a financial planner with Sun Life Financial, has noticed that people are underestimating just how long they will live. As such, he says it’s critical for advisors to have conversations that allow them to fully understand their clients’ goals and needs.

The importance of planning for the full duration of retirement has never been greater. While most clients don’t underestimate the planning itself, Chris Poole, a financial planner with Sun Life Financial, has noticed that people are underestimating just how long they will live. As such, he says it’s critical for advisors to have conversations that allow them to fully understand their clients’ goals and needs.

“There are lots of risks that come from underestimating the duration of retirement,” Poole says. “Looking at Statistics Canada or FP Canada, we realize that the statistical longevity for a couple currently in their 60s is that one of them will probably live to 95. This really changes things because it’s not about planning until one spouse passes away – it’s planning for the spouse who’s sticking around the longest.”

For these reasons, Poole says it’s important to have conversations about expectations. For some, this conversation might not be easy to have, but it’s vital because it helps an advisor plan for all outcomes.

“Clients have had income streams coming in, filling up that bag of money that they are planning on for retirement,” Poole says. “They spent their life paying down debt and saving. Come retirement, all that money they have saved, they are spending. In a perfect world, people are living off the interest, but we know that’s not always the case. They use the interest and erode some capital.”

Poole breaks retirement down into three phases: go-go, slow-go and no-go. Go-go is when people are spending their money doing the things they’ve always wanted to do. Slow-go is when they start to slow down, and no-go is the later stage when they may have different needs, such as long-term care.

“We encourage clients to take advantage of the assets they have accumulated – they should be excited about spending that money,” he says. “That being said, what we spend in the go-go phase affects what we have in our slow-go and no-go phases. As people start to think about the longevity risk, they realize what they want their lifestyle to look like on the back end of retirement.”

Sometimes clients need to make trade-offs later in retirement, so it’s important for that to be part of the initial conversation. Poole says running out of money is a real danger because it can have a ripple effect on an entire family. Because the dynamics of retirement have changed, so too must an advisor’s approach to income – and Poole believes it’s up to advisors to understand their clients and provide the best solution.

“With interest rates increasing, annuities can start to look favourable,” he says. “In other cases, segregated funds with steady streams of income look favourable. In others, bonds themselves may be a good solution. It’s understanding what a client wants and helping them determine what they need.

“The reality is, we are living longer, and we need to have conversations about money and health,” he adds. “There are all sorts of products to supplement the need for capital throughout all phases. While the money is available in the go-go phase, let’s slice off a little bit of income and invest into possible downside when we might need it on the back end.”

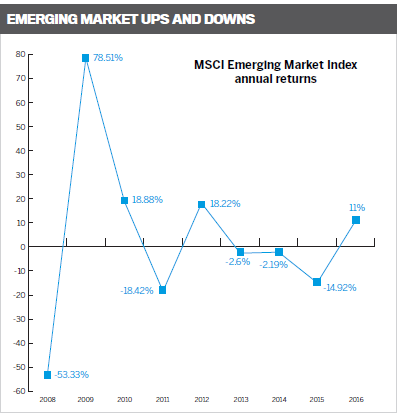

Emerging markets weather a rough year

THE PAST 12 months have been rough for emerging markets, which investors viewed as vulnerable in part due to US protectionism, a strong US dollar, trade war risks and moderating growth. Those factors, along with issues in Argentina and Turkey, led many investors to act emotionally, selling off emerging market stocks.

But some, including Tyler Mordy, president and CIO of Forstrong Global Asset Management, believe the future of emerging markets might not be so negative.

“I think extrapolating the emerging markets of the 1980s and 1990s to the present is a mistake,” Mordy says. “[Today], emerging market economies are much more shockresistant thanks to macroeconomic factors such as the emergence of domestic pensions, less reliance on foreign funding, improved trade balances, better fiscal balances and other strong secular growth drivers.”

Mordy believes there has been a misconception that EMs have huge amounts of debt in US dollars. Headlines from specific cases such as Turkey and Argentina have added to the perception.

“I don’t think those cases are a microcosm,” Mordy says. “Their circumstances are very different. Political dysfunction is one thing, but they are running big deficits, fiscal imbalances and don’t have the same structural reform that took place in other EMs.”

Thanks to past events, today’s emerging markets have implemented measures to avoid similar issues. “Most EMs, especially in Asia, learned from the Asian crisis,” Mordy says. “They reformed and implemented things like domestic pensions and social welfare. The conditions in Asia right now are so remarkably robust – you look at household incomes going up, the way corporations are moving to stronger governance, and policymakers bringing in things Western economies have.”

For Mordy, the biggest influencer on the performance of emerging markets in 2018 has been the US-led trade wars. “The US has not created many friends,” he says. “The main point is, we live in a globalized world with a globalized supply chain. Since the US has gone around it, we are left with China. Their strategy is tried and true – divide and conquer. Because US business is so intertwined with China, they are pitting corporate America against the administration.”

Mordy stresses that maintaining a longterm view of emerging markets is important. “By definition, these economies are emerging into the global economy and are going to be more volatile,” he says. “The biggest story we are noticing is the emergence of the Asian consumer for the next couple decades. Never have we seen 3 billion consumers enter the global marketplace. It is shifting how global demand and growth works.”

That should cause emerging markets to have a huge impact for investors in the next few years. The World Bank projects emerging markets will account for 60% of the global economy by 2035, but Mordy still sees value in certain areas, including “Asian stock markets and EM debt as a whole. If you compare bonds in the emerging markets versus the Western debt universe, we are starting from yields at 7% in the former, with EM currencies 20% to 40% undervalued compared to the US dollar,” he says. “When we look five years out at that income, plus the currency appreciation, the potential is there for at least a 50% total return in five years. So we see opportunity in that debt and in Asian countries.”

In the short term, Mordy also believes that emerging markets will re-establish their fundamentals. While trade-war uncertainty will likely continue into 2019, once investors realize that emerging markets are not going into recessions and the risks are limited, they will reassert themselves.

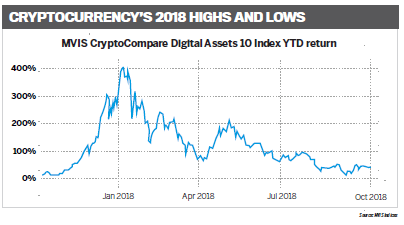

Cryptocurrency sees sharp decline

Cryptocurrency prices were on a roller-coaster in 2018. The ride began with a steep incline in late 2017/early 2018, followed by a sharp drop. As of September, the MVIS CryptoCompare Digital Assets 10 Index showed an 80% decline for the year. Experts have cited multiple potential reasons for the decline, including security, regulation and market manipulation. Yet for some, the decline was simply a matter of normalization.

As president and portfolio manager at Rivemont Investments, Martin Lalonde oversees Canada’s only actively managed cryptocurrency fund. He notes that 2018 was mostly a down year, but he remains bullish on the sector’s long-term potential.

“We think 2018 was normal; 2016 and 2017 were very good,” Lalonde says. “Cryptocurrency is a very volatile asset class. Even though [Bitcoin] has dropped to about $6,500, we hope it can hold and are bullish it can have another increase either later this year or next. We view the volatility as a good thing because there is a correlation between volatility and returns. It means you can achieve returns that you might not be able to in other sectors.”

At this point, Lalonde has seen enough to believe that cryptocurrency is more than just a fad. “I think the sector is still growing,” he says. “More people are using cryptocurrency – it is becoming more accepted and moving in the right direction.”

Lalonde has tried to balance out some of the risk in his fund by allocating a large portion of it to cash – the fund is currently 39.6% Bitcoin and 60.4% cash in order to protect capital. “Because we believe we are in a bear market [for cryptocurrency], the leaders will lose less,” Lalonde explains. “For Bitcoin, they dropped from $20,000 to $6,500, but other cryptocurrencies lost much more. So we have a high portion of cash to protect capital.”

Despite the recent decline, Lalonde believes that Bitcoin will rebound, just as it has in the past. He also notes that the investors currently in the fund are aware of its volatility – something that all cryptocurrency investors need to be willing to shoulder.

“Our investors know it’s a volatile sector, but they want to be exposed to it,” Lalonde says. “For us, we try to capture the uptrend. Our goal is to technically analyze the trend and trade to run returns as high as possible.”

The potential to catch that upswing is why Lalonde still believes now is a good time to get into cryptocurrency. “We still have a longterm view on cryptocurrency and especially Bitcoin – any moment is a good time to invest in it,” he says.

Because cryptocurrency is so volatile, it can be difficult to predict the future, but Lalonde says nothing will surprise him.

“I wouldn’t be surprised if Bitcoin’s value reached half a million, but you just never know,” he says. “I do still see growth for it. We believe that you might see something like 2017 again in a couple years. Long-term, we remain bullish because I think many currencies have found their bottom. Still, it could stay sideways for a year.”