When attempting to achieve higher returns, there are “no guarantees” except that you will be taking greater risks

One of the core pieces of information in the financial planning process is the assumption of what the future return for a portfolio could be. Certainly, higher returns are more desirable as they generate greater spending power and/or the potential to achiever goals sooner. Of course, the standard caveat is that higher returns come with higher risks or in other words, the greater possibility of losing money for some period of time.

.png) When attempting to achieve higher returns, there are “no guarantees” except that you will be taking greater risks. So, selecting realistic expected returns is critical. However, just because we expect something, does not mean it is going to happen; as the financial markets seem to go out of their way to prove most prognosticators wrong.

When attempting to achieve higher returns, there are “no guarantees” except that you will be taking greater risks. So, selecting realistic expected returns is critical. However, just because we expect something, does not mean it is going to happen; as the financial markets seem to go out of their way to prove most prognosticators wrong.

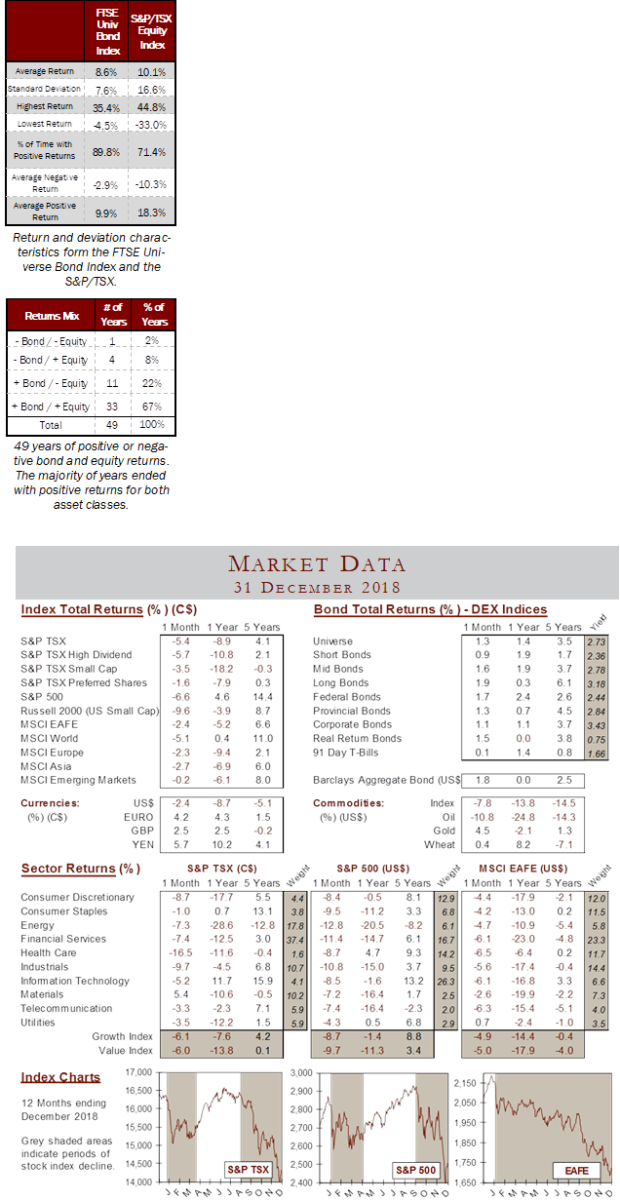

The best reward versus risk mix is one that gives you the highest possibility of achieving your objectives through all market conditions. This is much better than just picking expected returns based upon historical results. As the chart below and the data to the left show, historical results are all over the map. So, looking for a landing spot going forward is not easy.

The annual returns for Canadian stocks and bonds between 1970 and 2018 show some interesting information. Over the past 49 years there has been only one year with negative Canadian stock and bond returns, 1974; and only four other years with negative Canadian bonds returns at all (the worst annual decline for bonds was -4.5% in 1974). So, bonds are not really a problem.

Canadian equities have been down for 11 other years (excluding 1974) since 1970 or have declined 22% of this time. This implies that Canadian stocks and bonds have generated positive results simultaneously 67% of the time. Two out of every three years! On the equity side of the equation there has been remarkably ONLY one instance of Canadian Equities being down two years in a row (2001-2002), at the height of one of the biggest recessions of the past 100 years. This is definitely positive news after the declines of last year.

Equities have taken a hit in 2018 despite solid earnings growth, with the main culprits being: uncertainty over trade disputes, tighter financial conditions and late-cycle market concerns. While growth may moderate, there is little near term risk of a recession. Corporate earnings growth is slowing but still reasonable and bonds are looking more appealing.

Overly defensive positioning can undermine investors’ long term goals. With the potential for upside investors should focus on building resilient portfolios and not just dialling down risk. Resisting the urge to remove all risk in portfolios and concentrating on carefully balancing risk and reward for your own particular long term objectives is paramount.

Expectations are everything. To a large degree your expectation of future returns is a major contributor to whether you experience positive or negative surprises. While history is an important guide, it is the future that is vital. So, do not live in the past, but prepare for what is down the road.

For more information, visit provisus.ca. Financial advisors can visit provisus.ca/advisors.

SPONSORED BY:

.jpg "Provisus Wealth Management")