In this special guest article, Garrett DeSimone outlines an approach that emphasizes the value of a solid options strategy

In this special guest article, Garrett DeSimone, PhD, Head of Quantitative Research, OptionMetrics, outlines an approach that emphasizes the value of an options strategy.

Late last year, Sears Canada filed bankruptcy with thousands of workers potentially impacted by a shortage in benefit pension plans. And other Canadian corporations may have underfunded workers’ pension plans, according to a report from the Canadian Centre for Policy Alternatives.

Many state retirement systems face systemic yearly funding shortfalls as a remnant from the 2008 financial crisis. The severity of this underfunding is expressed in the trillions, with state plans disclosing assets of $2.6 trillion to cover $4 trillion in liabilities. The central source of this giant gap is lackluster investment returns that fell far short of manager expectations (The median public pension plan’s investments returned about 1 percent in 2016, well below the median assumption of 7.5 percent).

At OptionMetrics, we have seen increased interest, from public and private pension funds in Canada and other areas, to pursue strategies involving exchange listed options.

Fund managers are looking to new strategies involving alternative investments in search of higher yield. The incorporation of equity options into a traditional portfolio can significantly enhance its risk-return tradeoff. The benefits of options include the ability to protect from tail-risk events and reduce overall correlation within a portfolio, generate consistent income from investments, and enhance risk-adjusted returns.

As an example, I present a strategy that emphasizes the value of an options strategy to a potential fund manager. A split synthetic strategy is used to replicate the payoff of an underlying stock using a long call and short put option. A key benefit of this strategy is it takes advantage of the leverage contained within the options to avoid tying up capital, as well as the relative expensiveness of puts compared to calls.

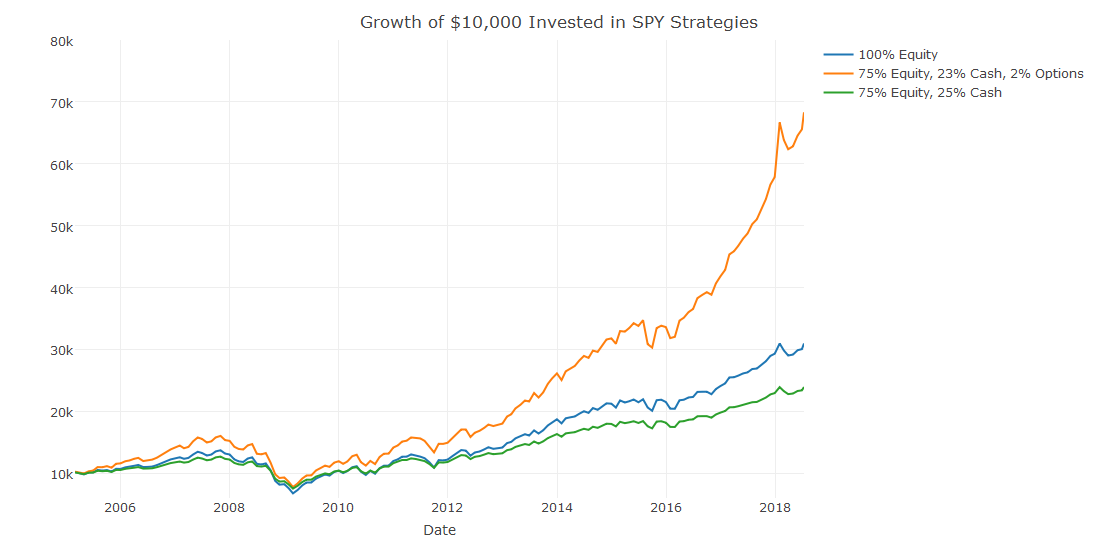

At the beginning of each month, I select a call and put option that is 5% out-of-the-money and has between 40 and 60 days to expiration. Typically, the out-of-the-money put option is more expensive than the corresponding call, generating a net credit. At the end of the month, the positions are closed and rolled over. We demonstrate how truly powerful the leverage of the option is by only setting a target allocation of 2% to the split-strike synthetic, 23% in cash, and the rest in the SPDR S&P 500 ETF (SPY).

Source: OptionMetrics

The graph presented above shows returns to an all-equity portfolio, 75% equity portfolio plus cash, and 75% equity, 2% options plus cash. The portfolio enhanced with options (as shown in orange) is clearly the dominant strategy, earning a whopping 683% percent over the sample. In comparison, the all equity portfolio (blue) earns 310% percent.

The only small sacrifice for the massive enhancement in returns of the options-enhanced strategy is a small increase in annualized volatility (15.28% vs. 13.6%). The key to this strategy is that earnings from the options strategy are reinvested in the underlying ETF at the end of every month, creating a powerful compounding effect.

It should be noted that this strategy does contain risk. The naked put option exposes the holder to skewness risk in the event of a large drawdown which may result in the put option landing in the money, and the possibility of a margin call. However, the 23% cash position acts as a buffer in these market conditions, cushioning the portfolio in market downturns. Even with this factor considered, the inclusion of options in a portfolio creates a dominant strategy with many possibilities.

While I primarily focus on a strategy used to enhance returns through leverage, there are many other ways options can assist institutional investors in meeting their investment goals. While investing in derivatives can be risky overall, they are a valuable alternative asset class with convex risk and return characteristics that are different from linear assets like stocks and bonds. Options could be a good way to further diversify portfolios and increase the potential for increased returns, alongside other investment strategies.