The coronavirus pandemic is causing global concern about financial system stability but has Canada got it right?

After the global financial crisis more than a decade ago, the interrelated financial systems of the world’s largest economies were under the microscope.

Now, as we face an increasingly challenging economic crisis driven by the COVID-19 pandemic, questions are being asked about the stability of financial systems.

Canada’s reputation for a strong, resilient, banking sector will be tested alongside its peers, but the sector’s regulator says that it is confident the measures in place are adequate.

The Office of the Superintendent of Financial Institutions (OSFI) says that the country is respected for its adherence to international banking standards and measures which go beyond the minimum requirements of the Basel Committee on Banking Supervision (BCBS).

In an overview of the existing regime in Canada, the regulator says that two third-party reviews of the regime in the past decade have both resulted in the highest rating.

“This balanced approach has served Canada well in the past and will continue to serve us well in the future,” OSFI says.

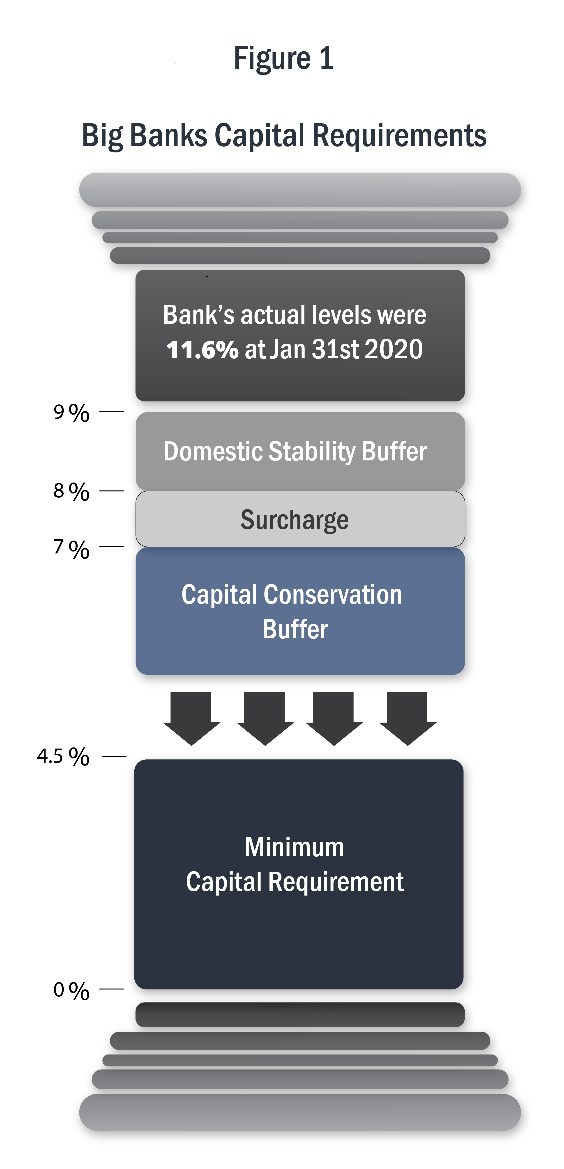

What’s in place?

Canada’s biggest banks are required to maintain a capital buffer to protect liquidity during a downturn.

When OSFI released the buffer last month to allow banks to draw on these funds, it was set at 2.25% but has been eased to 1.0%. Even at the reduced level, OSFI says that it is one of the largest of its kind among global regulatory requirements.

For smaller banks, there is also a requirement to maintain a level of capital.

The regulator is also able to require banks to restrict disbursements such as dividends and share buybacks.

With the measures that are in place, the regulator says that banks should have the liquidity they need to navigate the treacherous waters of an economic downturn.