New rankings show transparency of Canada’s senior governments

The federal and provincial governments expect us to be completely open when filing taxes and other information but how good are they at transparency?

A new CD Howe Institute report ranks the country’s for transparency and and reliability in their budgets and financial reports – and proposes some easy steps to improve them.

“Governments’ extraordinary powers to tax and coerce citizens make monitoring their behavior particularly important,” commented William B.P. Robson, who alongside Farah Omran has authored the report. “Canadians need budgets and financial reports they can understand and use to hold governments accountable.”

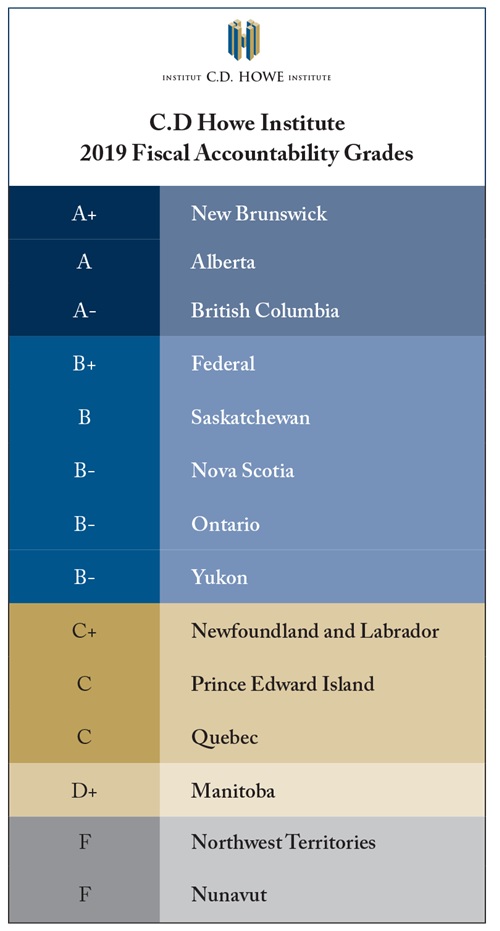

Topping the list with an A+ rating is New Brunswick with Alberta and British Columbia ranking A and A- respectively. The federal government trails in fourth place with a B+.

The report, which looked at budgets for the fiscal year 2018/19 and financial statements for 2017/18, found that Manitoba is near the bottom of the list with a D+ while the Northwest Territories and Nunavut scored F.

“We are glad to report that, over time, the fiscal transparency of Canada’s senior governments has improved. Two decades ago, none of them presented budgets you could compare to their results; today, consistent accounting is the rule,” said Robson. “The remaining deficiencies and instances of backsliding are fixable, as the examples of the leading jurisdictions show.”

The authors said that the federal government (B+) and the provincial governments of Saskatchewan (B), and Ontario, Nova Scotia and Yukon (B-) could join the top rank with relatively small improvements, such as making key numbers easier to find, more timely presentation and publication, and helping legislators understand how their votes on programs reconcile – or not – with budget plans.

Key recommendations

There are several ways that governments could improve their financial reporting, the report concludes:

- Financial Statements Should Reflect Public Sector Accounting Standards - represented by an unqualified opinion from the relevant auditor general – as should in-year updates on the evolving situation. Public accounts should as well include reconciliation tables explaining differences between projections and outcomes.

- Budgets Should Match Financial Statements. Governments should not confuse users of their financial documents with more than one set of headline figures, or inconsistent aggregating and netting that make what should be a simple comparison of projections and results practically impossible.

- Budgets Should Precede the Start of the Fiscal Year. It is an affront to accountability to ask legislatures to approve a plan after money has already been spent.

- Estimates Should Be Timely and Easily Reconciled with Budgets. Legislators often get, and vote on, estimates after the financial horses have already started leaving the barn, and may have no idea whether their votes are consistent with the budget plan

- Key Numbers Should Be Accessible and Recognizable. Relevant and accurate numbers are less useful if potential users cannot find them or recognize them.

- Year-End Results Should Be Timely. Legislators and citizens need timely information about whether the government fulfilled its promises, and to understand the size of, and reasons for, deviations from targets.

“If Canadians demanded better financial reporting from their governments, they could get it,” said Omran.