Why this strategy thrives in current environment and how CI GAM's suite of covered-call ETFs stands out

This article was produced in partnership with CI Global Asset Management.

Another week, another major market move. Investors could be forgiven for feeling a little beaten up by 2022 at this stage. Not only have inflation and rising interest rates increased volatility but geopolitical issues have compounded these challenges. Yet covered call strategies thrive in this type of environment and have garnered strong sales traction this year.

Veronika Popova, Director, ETF Strategist, at CI Global Asset Management (CI GAM), believes their popularity is understandable given how they perform relative to uncovered strategies in flat or bear markets. This is exactly what CI GAM, which has a suite of covered-call ETF solutions, has seen. The premiums received from the call options have been further enhanced by volatility, offsetting some of the declines experienced in the market.

“Investors have always been faced with challenges and this has been elevated by the decline in returns so far this year, along with the fear of continued downside,” Popova said. “Rising geopolitical and macroeconomic issues such as inflation have made markets highly volatile and investors should be able to capitalize on that volatility.

“Option premiums are a function of volatility, and the volatility in the market has helped boost those option premiums. That being said, a covered call strategy allows investors to use the income received to offset any downside they are experiencing as well.”

What are the main features of the ETF?

A covered call strategy is implemented by selling a call option contract while owning an equivalent number of shares of the underlying stock, essentially selling someone the option to buy your shares at a predetermined price at a predetermined time. This is generally considered to be a conservative strategy for the seller because it decreases some of the risks of stock ownership by providing additional income from the option premiums on top of any dividend income earned.

However, less risk can equal less return. Writing call options caps upside potential on stock price increases above the strike price. Popova said because CI GAM writes call options on approximately 25% of the portfolio, investors still have equity exposure but with some downside protection and an enhanced tax-efficient yield, since the call option premiums are considered capital gains instead of income.

This can sound complex to the average investor, but in breaking down the strategy, advisors can explain to clients how this is a great way to get paid for the volatility they are experiencing, instead of losing out because of it.

Popova explained: “Investors are able to complement their existing income-oriented or tactical portfolio holdings by providing enhanced income and risk mitigation, particularly for any respective uncovered strategies they may already hold, all while still maintaining the opportunity to participate in any upside as they wait for the markets to turn around again.”

Common pitfalls

For advisors, while this strategy can add significant benefits to a client’s portfolio, there are potential misconceptions to consider. The biggest is that covered-call strategies are completely immune to downside risk, so are risk-free. This is not true because the call options are written on just a percentage of the portfolio; therefore, the underlying equity remains the dominant driver of returns. However, the riskiness of the ETF is dependent on the volatility of the underlying sector used for the strategy, which can vary from a higher-risk energy or tech covered-call strategy versus a less volatile one based on Canadian banks.

Popova said: “It’s important to understand how these strategies perform in different market environment. When prices rise, the shares with call options written on them are often called away, thereby forfeiting some of the upside participation in a stock. However, in return for forfeiting potential capital gains, you are receiving a degree of risk mitigation and income diversification.”

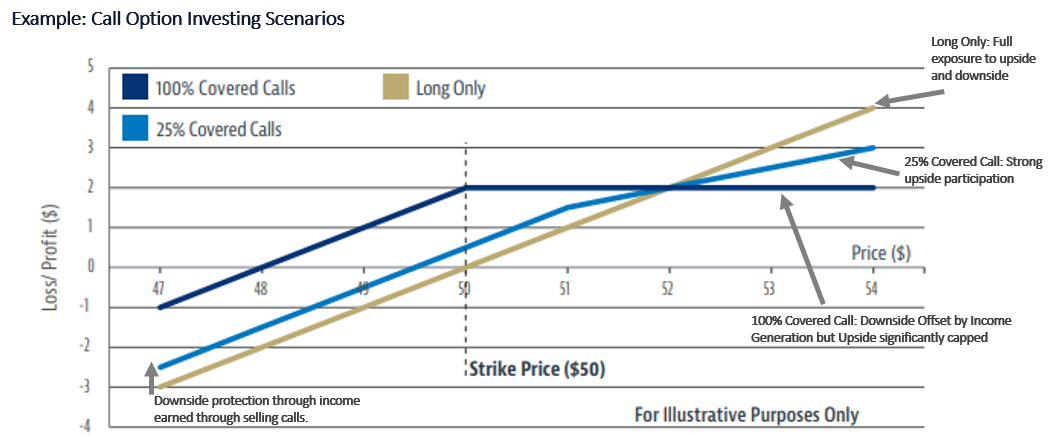

The below chart visualizes how a covered-call strategy works and the balance between income and risk mitigation versus upside potential, depending on how much of the portfolio is subject to call options.

How does CI GAM stand out from other covered-call ETFs?

While Popova said its yields “speak for themselves,” she explained that it’s how CI GAM achieves those results that separate it from the pack. There are three considerations that make up a covered-call strategy that investors should examine to understand how much premium they can expect to receive: the underlying market itself; the percentage of covered calls written on the portfolio; and the “moneyness” of those options.

With a strategy based on a naturally volatile sector, including those with a robust options market, writing a higher percentage of call options and writing those call options “closer to the money,” all contribute to a higher option premium. However, there is a trade-off between achieving a higher option premium by writing more call options as close to the money (as close to the current market price) as possible, and the amount of upside participation you have in the underlying stocks.

She explained: “CI GAM writes options on approximately 25% of the shares within the portfolio, as we believe if an investor is looking for exposure to a sector or target market, then they are bullish and want to participate in the upside. Nevertheless, we are still able to achieve attractive yields since we are writing these options very close to the money. This is where our portfolio managers’ expertise comes into play in determining where to write those options and on how many shares.”

While covered call strategies may sound complex to the average investor, CI Global Asset Management has a suite of covered call ETF solutions that give investors convenient access to professionally managed strategies backed by in-depth expertise in covered call writing.

If you are interested in learning more about them and how they can complement your portfolio, please visit www.ci.com.

The opinion and information provided in this discussion are solely those of the speaker(s) and are not to be used or construed as personal, legal, accounting, taxation or investment advice, or as an endorsement or recommendation of any entity or security discussed or provided by CI Global Asset Management. Individuals should seek the advice of professionals, as appropriate, regarding any particular investment.

Commissions, management fees and expenses all may be associated with an investment in exchange-traded funds (ETFs). You will usually pay brokerage fees to your dealer if you purchase or sell units of an ETF on recognized Canadian exchanges. If the units are purchased or sold on these Canadian exchanges, investors may pay more than the current net asset value when buying units of the ETF and may receive less than the current net asset value when selling them. Please read the prospectus before investing. Important information about an exchange-traded fund is contained in its prospectus. ETFs are not guaranteed; their values change frequently, and past performance may not be repeated.

The CI Exchange-Traded Funds (ETFs) are managed by CI Global Asset Management, a wholly-owned subsidiary of CI Financial Corp. (TSX: CIX; NYSE: CIXX). CI Global Asset Management is a registered business name of CI Investments Inc.

©CI Investments Inc. 2022. All rights reserved.