Satisfaction with banks is declining according to JD Power

When you’re already trying to manage higher costs the last thing you need is an unexpected one, especially when it’s from an organization that’s looking after your money.

Canadian bank customers say they are paying more fees now than a year ago including account maintenance/minimum balance (18%); overdraft or insufficient funds (14%); and ABM fees (12%) according to the latest J.D. Power 2023 Canada Retail Banking Satisfaction Study, released this week.

While no one likes paying fees, the dissatisfaction is driven not so much by having to pay them but by not expecting them with 80% of respondents saying banks can do more to let them know how to avoid fees.

Rather than finding out through an account statement, advance warning of fees produces a higher level of overall satisfaction, the study reveals. And there are further takeaways for financial institutions about how communication is the key to better customer relationships.

“Customers are under increasing economic stress and express a declining feeling that banks are addressing their concerns and financial challenges,” said Paul McAdam, senior director of banking and payments intelligence at J.D. Power. “Customers want banks to communicate how to avoid paying fees; provide advice on how to build savings and reduce debt; and resolve problems efficiently—especially when it comes to tackling fraud on a chequing account.”

Declining financial health

The report also shows how economic conditions are eroding Canadians’ financial health with 50% considered financially vulnerable or stressed, an increase from 44% a year ago.

With customers not feeling that their banks’ account offerings meet their needs, overall satisfaction is weakened.

With fraud increasing, there has also been a decrease in satisfaction with how banks handle fraud-related problem resolution.

Generally, communication channels are not providing what customers need and satisfaction is down for branch service, online banking, and mobile app. Concern for customer needs and courtesy of staff are leading reasons for lower satisfaction for branches while ease of navigation is an issue for digital channel users.

“The financial institutions that rank highest are those that effectively communicated about fees, fraud, and savings; that provided tools and information about budgeting and debt reduction; and addressed security and fraud problems in a timely manner,” noted McAdam.

Customers may not be happy with their banks but are still unlikely to switch and may even use them for new accounts and products. But they are also less likely to recommend their bank to a friend or family member.

Who’s doing better?

The report says that banks can do better by meeting customer expectations of support in three key areas:

- alerts about suspicious account activity (56%)

- information on how to reduce fees (50%)

- advice on ways to save money and earn more interest (35%)

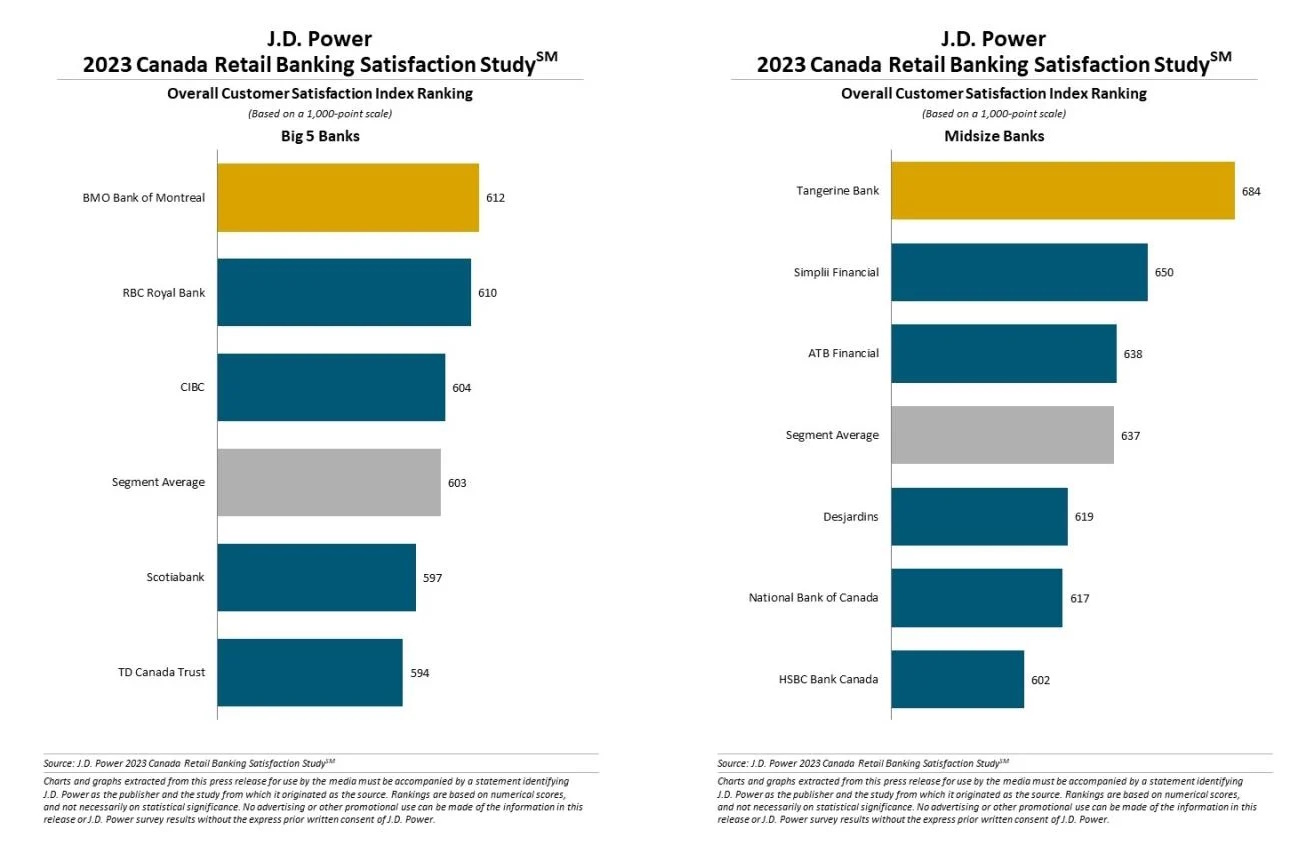

Overall satisfaction with the Big Five banks has dropped 10 points year-over-year in 2023 to a score of 603 out of 1000 and has fallen 7 points to 637 for mid-sized banks.

BMO Bank of Montreal ranks highest in satisfaction among Big 5 Banks with a score of 612. RBC Royal Bank (610) ranks second and CIBC (604) ranks third.

Find out the CIBC’s notable achievements in this article.

Tangerine Bank ranks highest among midsize banks for a 12th consecutive year, with a score of 684. Simplii Financial (650) ranks second and ATB Financial (638) ranks third.

Read more: What do I need to know about Tangerine Bank?