Reports from RBC and National Bank highlight the tough place Canadian households find themselves in

Canadian household debt levels are worrying analysts. Two reports released this week, one by RBC Economics and one by National Bank of Canada Financial Markets, highlighted the difficult place rising interest rates have left consumers in.

The National Bank report attributes Canada’s falling GDP in Q3 of 2023 to interest rate hikes. They note, as well, that stagnant consumption in the context of record population growth also points to a weakening consumer due to interest rates.

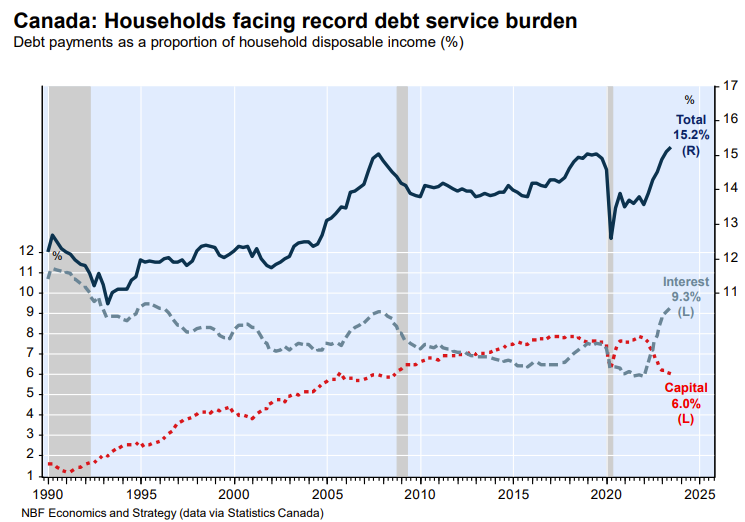

As confirmation of those outlooks, they cite data recently released by Statistics Canada showing that the household debt service ratio — the proportion of disposable income devoted to debt payments — has reached 15.2%. That is the highest level seen since data collection began in the early 1990s.

Over the past six quarters, the report states, interest payments on debt rose from 5.9% of disposable income to 9.3% — the highest level since 1995. Even as long-term rates declined somewhat as investors began pricing in rate cuts next year, many Canadians are facing mortgage renewals and mounting debt service costs which could be a significant headwind for the economy next year.

The RBC report also highlighted the rise in the debt servicing ratio but highlighted other challenging datapoints around the Canadian consumer. Notably, Canadian household net worth fell by around 1.8% in Q3 to a total of $301.2 billion. Some of that was due to losses on equity and fixed income markets through Q3. Some of it was due to deterioration in home equity, which has now fallen to 10.3% below Q2 2022 levels, though it remains 57% above pre-pandemic levels.

Read more: Canadian consumer debt balloons by over $80 billion | Wealth Professional

While credit market debt accumulation moved up by 0.8%, household disposable income actually rose slightly faster at a rate of 1.0%. Credit card debt, however, rose by 2.6% in Q3 as Canadians relied on credit cards and lines of credit to cope with the cost of living.

“Canada’s household debt levels are high, and increases in interest rates continue to pass through to debt payments with a lag,” the RBC report reads. “The household debt service ratio is already at record levels and will move higher as debt payments continue to rise alongside wobbly looking labour markets. And the Canadian economy has already contracted for five straight quarters on a per-capita basis with consumer spending softening. Against that backdrop, further interest rate hikes from the Bank of Canada have become increasingly unlikely and we look for a pivot to gradual rate cuts by mid next year.”