Leaders from Dynamic Funds explain why ESG ratings don't always tell the full story – and why an active approach matters in this space

This article was provided by Dynamic Funds.

How can advisors and investors confidently determine company performance on environmental, social and governance (ESG) criteria?

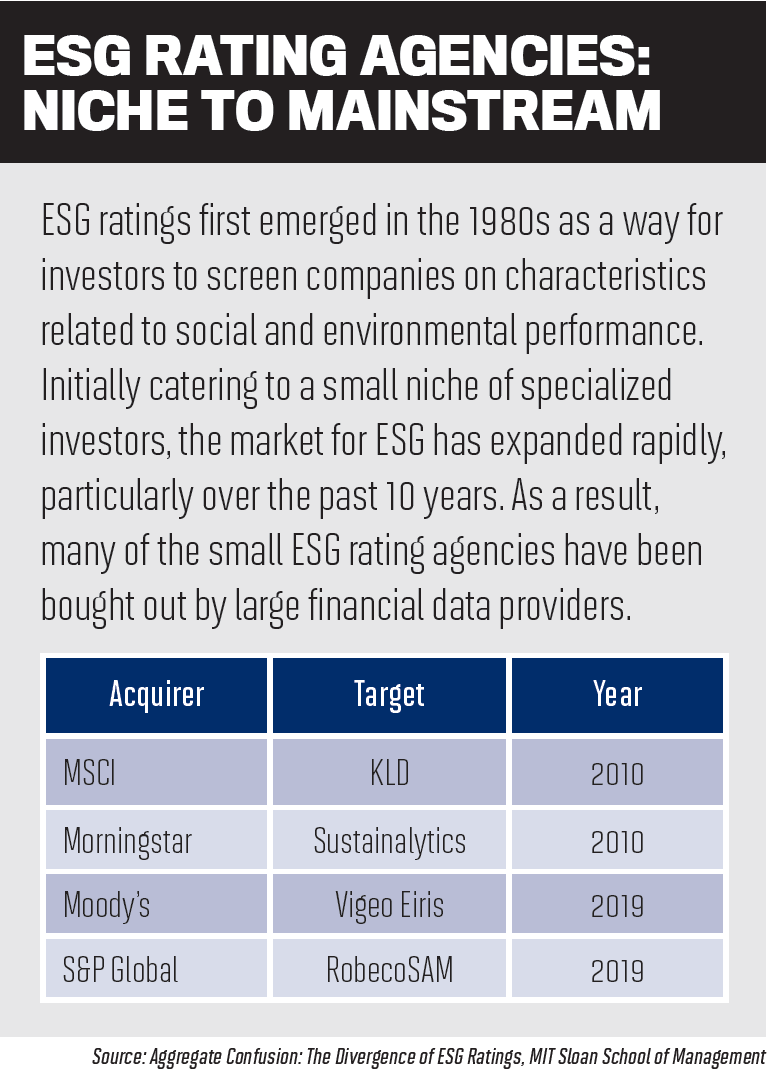

The answer is, it’s complicated – in fact, it depends on who you ask. In the same way that credit rating agencies using varied criteria might assign different scores to the same firm, there is ambiguity among the rating agencies that assess individual companies when it comes to ranking them on ESG factors, and firms may achieve very different scores.

Electric vehicle manufacturer Tesla is a great example – Sustainalytics has given Tesla a 30.5 rating, putting it in the ‘high risk’ category1, while MSCI’s A rating suggests average ESG performance2, and S&P has placed Tesla in the top quartile for ESG performance3.

Low correlations

Low correlations

Low correlations across ESG rating agencies are not surprising. Rating agencies may have long histories when it comes to their bread-and-butter financial data businesses, but ESG factors are less numbers-based and more values-based. How, for instance, do you accurately measure and grade a firm’s treatment of workers? It can be more art than science.

One thing is clear – the stakes are high. If a firm gets a favourable rating from S&P, as Tesla did in May, that ranking may be included in the firm’s S&P 500 ESG Index, which is, in turn, used by passive ETFs, index funds and some mutual funds as they assemble portfolios, posing a challenge for investors trying to contribute to an environmentally sustainable and socially just world. A passive approach that relies exclusively on ratings can include investments that may have underlying ESG-related risk and exclude hidden gems with strong performance metrics and emerging ESG strength.

“Effective measurement of ESG performance requires a multifaceted and complex approach that can be highly subjective,” says Jim Morris, COO at 1832 Investment Management, which manages Dynamic Funds. That’s why, says Morris, Dynamic Funds conducts its own active ESG assessments on individual companies and leaves it up to the investment team to make the final determination.

“ESG factors have long been a critical component of our research process,” says Morris, who is constantly evolving in-house ESG infrastructure and risk-reporting for Dynamic Funds.

Proprietary active ESG analysis

Dan Yungblut, head of research at 1832, is a key figure spearheading company ESG initiatives. He’s also chair of 1832’s ESG Investment Committee, which oversees the integration of ESG factors into the investment process. Yungblut stresses that Dynamic Funds, as a dedicated active manager, relies on proprietary active fundamental ESG analysis.

“If you passively rely on ESG scores, I don’t think you get as full an understanding of material ESG factors,” he says. The reasons for this are twofold, according to Yungblut. The first relies on the nature of ESG assessments, which, by their nature, are backward-looking and capture a single moment in time.

“ESG scores tend to be static snapshots, less focused on future performance,” Yungblut explains. “Active investment managers spend most of their time looking ahead, not behind, when assessing companies’ futures, and that includes ESG criteria.”

As a result, Yungblut believes active managers can derive a much more nuanced understanding of a company’s ESG profile – both now and into the future.

“In many cases, we’ve known the businesses for years and can determine which ESG-related factors are material and where the business is headed,” he says. “Quite simply put, when it comes to ESG investing, experience matters.”

Part of the solution

Another benefit of a legitimately active approach is that it often yields not just a better understanding of companies and how they fare in terms of ESG factors, but also the opportunity to be part of the solution to enhance their ESG performance. By undertaking rigorous fundamental research to iden-tify the greatest potential long-term reward to investors, Dynamic is better positioned to find companies that might not lead on ESG criteria today, but are progressing to become the leaders of tomorrow.

Critical to this process is the ongoing engagement of Dynamic’s portfolio managers, who regularly meet with company management, suppliers, employers and other stakeholders. Dynamic’s dialogue with company leadership can help firms identify ESG strengths and weaknesses, and the team is uniquely positioned to influence decisions through their specialized understanding of the direction and growth potential of the firm. That may, in turn, enable Dynamic to invest earlier in a transformative firm, potentially yielding unrecognized investment opportunities.

To illustrate his point, Yungblut points to Dynamic’s first ESG-related thematic fund, the Dynamic Energy Evolution Fund, which is committed to finding global opportunities related to the transition to more sustainable energy sources. When constructing the portfolio, the fund’s managers identified an opportunity in a solar power-related company that has a low ESG score due to lack of reporting on employee development initiatives. Dynamic’s independent analysis uncovered a strong company, but not any material issues of concern that impacted the investment decision.

To illustrate his point, Yungblut points to Dynamic’s first ESG-related thematic fund, the Dynamic Energy Evolution Fund, which is committed to finding global opportunities related to the transition to more sustainable energy sources. When constructing the portfolio, the fund’s managers identified an opportunity in a solar power-related company that has a low ESG score due to lack of reporting on employee development initiatives. Dynamic’s independent analysis uncovered a strong company, but not any material issues of concern that impacted the investment decision.

“At Dynamic, we want to make our own independent assessment, determine what we think is going to drive a company forward and then decide whether or not we invest,” Yungblut says. “We never want to outsource our decision-making to an external ratings company.”ESG investing can be complicated, and relying strictly on rating agencies may not tell the whole story. Advisors are an essential resource to help clients chart an ESG journey to meet their unique goals.

Jim J. Morris (B.Comm., MBA) is Chief Operating Officer at 1832 Investment Management, which manages Dynamic Fund, while Daniel Yungblut (MA, LLM, CAIA, CFA) is VP and Head of Research.