Poll shows kids are managing money earlier than their parents

Canadian kids are starting to manage their own finances earlier than their parents did, although financial independence is slightly later.

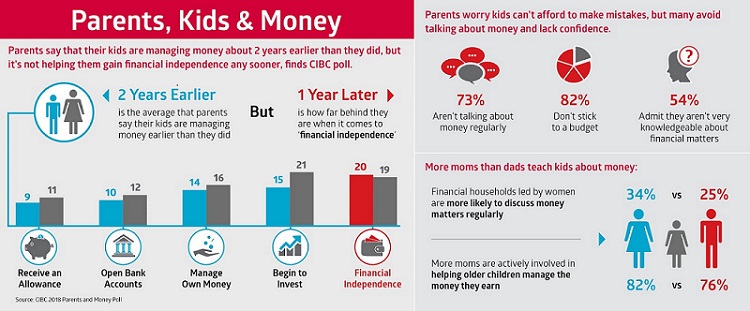

A poll from CIBC released Tuesday reveals that financial milestones such as opening a first bank account, getting an allowance, managing money, and getting a credit card, are all happening about two years earlier than it did for their parents.

But the survey of more than 1,000 parents with children under 25 found that the age of financial independence is now 20, compared to 19 for the parents.

There might be an opportunity for financial advisors to start attracting new clients earlier as 73% of parents say they avoid talking about money regularly and worry they lack the know-how, leaving their kids at risk of being underprepared to manage their finances effectively.

"It's encouraging that parents are getting their kids on the right track early on but setting your kids up for financial success is more than just opening a bank account and giving them money to manage on their own," says David Nicholson, Vice-President, CIBC Imperial Service. "It's also about having frequent conversations about money matters, which can be tough to do if you don't feel comfortable with your own finances."

Parents lack knowledge on finances, investing

A key reason that parents are shunning money conversations with their kids is that 93% of respondents say they are struggling with their own finances.

More than two-thirds admit they're only 'somewhat' following a budget at best, while 14% don't have one at all. Almost half are currently carrying credit card debt.

Knowledge gaps are clear with just 46% of parents saying they are “very knowledgeable” about budgeting, 44% saying that about saving, and 39% about debt management.

The lowest share of very knowledgeable parents is for investing at just 17%.

"We all want what's best for our kids, but we may not always model the best financial habits and behaviours," adds Mr. Nicholson. "You don't have to have all the answers but seeking out expert advice together online or with your financial advisor can improve your family's financial literacy and confidence as a whole."

Moms in charge

Overall, moms take the lead in children’s finances, the poll found.

More financial households led by women than men say they regularly discuss money matters (34% vs 25%), and moms are more apt to discuss nearly every financial topic with their kids, including their own salary.

Moms are also more likely to be helping older children manage the money they earn (82% vs. 76%).

When it comes to allowances, 80% of parents believe it's important with the average allowance of $91 each month. More than half say their kids 'need to earn it' or are compensated occasionally in exchange for chores with just 13% providing ‘no strings’ allowances.