Managing director for institutional clients at YTM capital looks at a fixed income universe in a state of rapid change

Kevin Foley is a Managing Director, Institutional Clients at YTM Capital. YTM Capital is a Canadian asset management company focused on “better fixed income solutions” specializing in Credit and Mortgage funds. Kevin is the former Head of Credit Trading, Syndication, Sales and Research at a major Canadian bank, and he sits on three Canadian Foundation Boards and Investment Committees.

In today's investment landscape, fixed income strategies are undergoing a significant evolution in response to recent disappointments and shifting market dynamics. As equities surge and interest rates fluctuate, many investors are reevaluating their fixed income allocations, seeking strategies that offer both stability and robust returns.

Too many investors have been lured into fading the fixed income compliment these days. Equities are running, the rise in interest rates have hurt returns, and traditional fixed income investments have been very disappointing. Nevertheless, one might argue that an effective fixed income portfolio is as important now as it ever has been.

The very good news is that there are effective fixed income investments, with compelling expected returns.

The rationale behind the renewed importance of fixed income lies in the current economic uncertainties and market complexities. Valuations detached from fundamentals, concerns over interest rates, and varied geopolitical factors underscore the need for diversified fixed income portfolios that offer resilience and enhanced risk-adjusted returns. Stretched P/E multiples, office real estate, gated private debt funds, concerns surrounding private equity valuations, and the ongoing uncertain path for interest rates are but a few of the reasons for this unease.

Unfortunately, bonds - the traditional fixed income solution, are highly dependent upon interest rates, yet the 3-4% expected total return from Canadian government bonds does not support most portfolio target returns. The blue-chip bond funds have generated losses so far in 2024, and over the past 5+ years, with returns barely positive over the past 10 year period. Therefore, investors are excused for their frustration with fixed income and the move toward alternatives to traditional bonds and bond funds to optimize portfolios.

The right fixed income portfolio can generate 6-8% on its own, along with the diversification and portfolio enhancing benefits that improve total portfolio risk and return metrics.

The consultants and investment professionals will confirm that the ideal make-up of the fixed income portfolio has evolved. It is no longer dominated by direct exposure to interest rates through traditional bonds and bond funds, and now includes investments in corporate credit, real estate, mortgages, infrastructure, and private debt, along with a much smaller complement of bonds or bond funds. They will also confirm that many combinations of these exposures, through funds, ETF’s and the right investment partners has saved portfolios and has thankfully massively outperformed traditional fixed income.

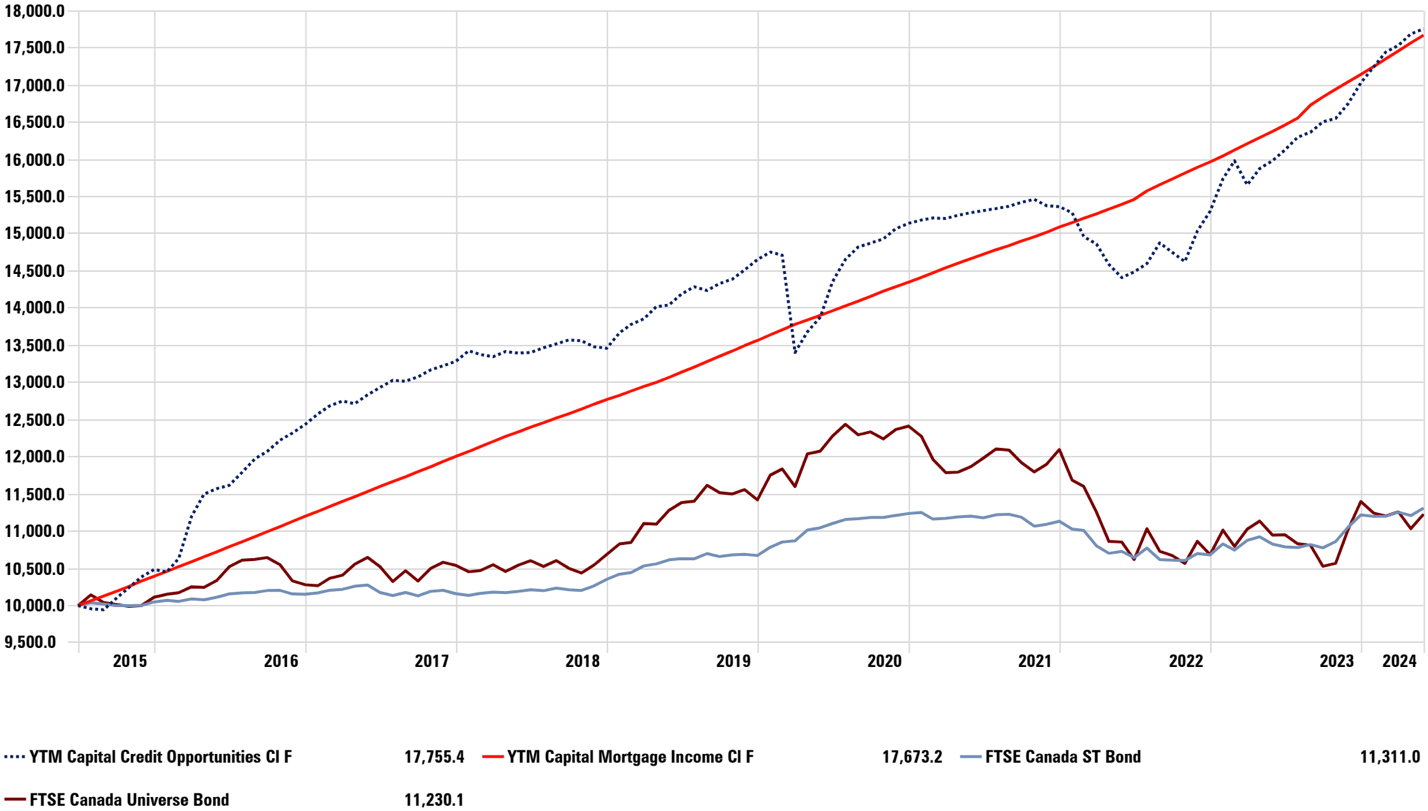

For example, my firm, YTM Capital is a Canadian asset manager with a track record focused solely on better fixed income solutions. The flagship YTM Capital Credit and Mortgage Funds have well-outperformed traditional bond funds and fixed income indices, helping investors achieve a protective fixed income portfolio, while meeting target returns. After delivering 11.3% and 7.37% returns in 2023, YTM Credit and Mortgage Funds have returned 4.2% and 3% YTD, and 6.67% and 6.7% since their 2015 and 2011 inception dates. They have delivered these net returns with lower volatility than the fixed income indices and most fixed income funds, in addition to the coveted metrics that improve total portfolio risk like; downside capture protection, high risk-adjusted returns, higher breakeven levels, with low correlation to bonds and stocks.

To produce these effective fixed income solutions, YTM Capital focuses on short term Canadian investment grade corporate credit, without exposure to interest rates, and select mortgages - including half of the mortgage portfolio supported by government or corporate guarantees.

(source: Morningstar)

For the rest of the important and refreshed fixed income bucket, investors should choose from a variety of proven exposures to real estate, which is notably an equity investment, through funds, REITS, or direct ownership. Investors can select from established infrastructure funds, also technically an equity investment, through managers that have demonstrated an expertise in the space. These real estate and infrastructure exposure should provide inflation protection to portfolios. Private debt has seen massive growth in the past many years, offering 7-10% expected returns in return for accepting a degree of illiquidity. Some unfortunate recent private debt headlines should encourage investors to find the right structure and fund manager. The addition of a small amount of high yield will suit some fixed income investors, although stretched current valuations and manager track record are important considerations.

Another promising area within the evolving fixed income landscape is liquid alternative credit strategies. These strategies now have meaningful track records and can offer several advantages over traditional fixed income solutions, including enhanced yields (meeting income goals, with capacity to cushion in adverse markets), lower interest rate sensitivity, diversification (low correlation to stocks and bonds), flexible / active portfolios, liquidity, alpha generation potential, and risk management (tools and portfolio benefits). The YTM Capital Fixed Income Alternative Fund is an example of a widely available, prospectus-based fixed income liquid-alt, with subscription and redemption available daily.

Investors should still also select the appropriate interest rate exposure for their portfolio, just not the 40% portfolio weight that it used to be. Maybe it’s now 5-10%, from an expert rates manager, or by simply buying the index. The good news is that rates have risen and do offer a modest return again. Further, if the economy and equities turn, rates should fall which will cause bond prices to rise.

Fixed income investing doesn’t have to be challenging or disappointing. Modelling a selection of the exposures above will optimize the total expected return of a fixed income portfolio, and it will importantly demonstrate how an effective fixed income allocation will improve both the risk and return expectation of the entire portfolio.