Chief Options Strategist outlines how his outlook for fixed income volatility can justify 10% yield target on bond ETF

The recent spate of covered call fixed income ETFs launched in Canada share one underlying premise: a historic high in bond volatility. These ETFs sell covered call options on their bond ETF holdings, namely the iShares 20 Plus Year Treasury Bond ETF (TLT). High volatility means higher premiums on options, so as bond markets get more volatile these ETFs can generate more yield without having to write as many options.

Right now, these strategies can benefit from historically high levels of volatility on the bond market. That’s due to one of the fastest central bank rate tightening cycles in living memory and a subsequent significant bond sell-off that has driven yields near or past their pre-GFC levels. Fixed income, however, is not an asset class known for its volatility. So while these strategies may look advantageous now, what happens to their high yields when volatility drops back to normal levels?

“We see a more volatile environment [going forward] than the low volatility environments we had perhaps gotten used to over the past 10 years,” says Nick Piquard, chief options strategist at Hamilton ETFs. “More volatile doesn’t mean that yields are going to keep going higher, or yields are going to keep going lower…I would just say that fixed income markets aren’t going to be {as stable] over the next many years.”

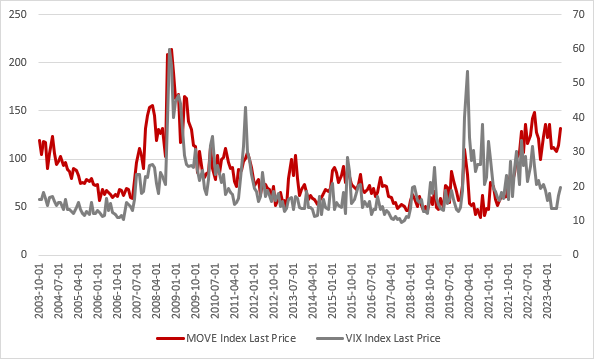

Piquard is part of the management team behind the Hamilton U.S. Bond Yield Maximizer ETF (HBND) which was the first of these fixed income covered call strategies launched this year. He justified his outlook with a comparison of the Merrill Lynch Option Volatility Estimate (MOVE) index — which shows levels of fixed income volatility — and the CBOE Volatility Index (VIX) — which shows equity volatility.

Source: Hamilton ETFs, Bloomberg

As the above graph shows, between roughly the great financial crisis and the aftermath of the COVID-19 pandemic, MOVE volatility was extremely low. Piquard explains that this compressed level of volatility was purchased at the cost of huge central bank quantitative easing schemes, pumping billions into the bond market to keep yields down.

However in more ‘normal’ rate environments, such as between 2003 and 2008, we see periods where MOVE volatility matches or even exceeds equity volatility. Piquard believes that while bond volatility may normalize somewhat, it won’t normalize to the levels seen in the post GFC decade. Central banks are unlikely to pursue quantitative easing on the same scale again and the simple scale of their balance sheets means widespread QE is unlikely. Bond volatility, therefore, could remain at somewhat elevated levels along with a ‘higher for longer’ interest rate consensus.

Piquard argues that his ETF can hold up its 10% yield target in this sort of environment. Hamilton is targeting a 50% option write level on the ETF’s holdings, but at today’s elevated level of volatility Piquard says they can achieve their target yields writing at around 33%. When volatility falls, they can ratchet up that write level and deliver the same target yield, albeit by trading off more opportunity for capital appreciation.

Patrick Sommerville, Senior Partner and Head of Business Development at Hamilton ETFs, noted that it’s unlikely his firm will write at levels higher than 50% on this ETF, though they are empowered to do so. That’s because they want to provide some degree of upside potential in their ETF. The written portion of their holdings will not be able to participate in any potential market upside when bonds begin to recover their value. Nevertheless, Sommerville believes that by keeping at least half of HBND’s portfolio exposed to upside, the fund can fit in long-term plans, and serve as more than an income play for current bond volatility levels.

“HBND should really be viewed as a yield enhancement vehicle, says Sommerville. The tax efficiency is worth noting as well, as the premiums generated by the covered calls are generally taxed as capital gains. As with all covered call ETFs though, there is an inherent trade-off, where you are capping your upside potential in favour of higher monthly income. With HBND, we want to provide a target yield of 10%, but keep the option writing to a level where we can still provide some long-term upside potential should rates fall at some point. A yield-first ETF with growth as a secondary feature.”