Mark Noble from Horizons ETFs outlines the reasons behind the pot sector’s explosive bounce back

.jpg)

By Mark Noble, Senior Vice-President, ETF Strategy, Horizons ETFs

It has been an exciting quarter for Marijuana-sector equity investors, with the Horizons Marijuana Life Sciences Index ETF (“HMMJ: TSX”), up almost 60% since its inception, as at March 31, 2019 (see performance chart below). This explosive rally came on the heels of a significant downturn in Q4 of 2018, where HMMJ declined by nearly 20%.

What explains this big bounce? Should we be concerned about how fast the sector has bounced back? Strong revenues and a generally optimistic outlook for equities have helped fuel this latest surge in prices. As to whether investors should be worried, that will depend on whether new drivers (needed to spur more performance growth) exist.

Strong revenue growth

On the first point, there seems to be two big catalysts for the comeback in Marijuana stocks. Firstly, the equity market is up in general, and for most investors, Q1 of 2019 (the first three months ending March 31, 2019) has been a "can’t miss" comeback for practically every equity market. Marijuana stocks have certainly ridden alongside the goodwill that has driven up most equity markets.

Still, the Canadian equity market, as represented by the S&P/TSX Composite Index, is up more than 12% this year, while HMMJ is up nearly 55% year-to-date (see chart below). A big reason for this is the strong revenue growth reported by most of the major Canadian licensed producers (“LPs”) of marijuana in the ETF and its index. Organigram, Aurora, Canopy and Tilray all reported revenue growth that met or exceeded analyst expectations.

Going into Q1, there was mounting concern that investors had placed lofty expectations on the sales potential of Canadian-domiciled LPs and that post-legalization recreational sales numbers could be disappointing. In fact, the opposite occurred as many LPs generally reported strong revenue numbers in their Q4 earnings versus the expectations.

There are still some more positive developments on the horizon for Canadian-domiciled LPs. Once the storefront retail sales start in Ontario later this year, we could potentially see another big leg-up in the revenue numbers of some of the providers. Again, this potentially provides more upside.

How much upside is priced-in after a nearly 60% rally in one quarter? This is where investors need to exercise some caution. Many of the leading Marijuana stocks are now trading near their late August/early September (of 2018) highs and are starting to have price-to-book values creeping back to extraordinary levels – with many of the leading stocks still exhibiting negative earnings.

Investors will need to be wary of potential disappointments from here on out. For example, any big revenue misses by any of the larger producers could see them punished relative to the broader sector. For example, Tilray, which was arguably the most widely-followed stock during the late-summer rally, has a negative return of approximately -11.19 % year-to-date*, whereas standouts like Cronos are up more than 70% year-to-date*. This level of dispersion highlights the crucial need for diversification in the sector, as HMMJ’s performance reflects more or less the aggregate performance of the sector, which is positive.

* Source: Bloomberg, as at April 1, 2019.

In the absence of big industry news, a potential near-term pullback in Marijuana is possible, and stocks that are exhibiting any relative weakness in the sector would likely be the most at risk for poor returns. For this reason, a concentrated approach in this sector can also be a dangerous one.

Click to enlarge

Further liberalization of the U.S. market is starting to work its way into valuations. Investors are excited by what they see as potential increasing flexibility in the U.S. federal government on marijuana restrictions.

The U.S. Market is Ramping-up.

Indeed, many of the Democratic presidential candidates are vowing to look at legalizing recreational marijuana1. This provides a big sentiment floor on Marijuana stocks and increases excitement for the space with investors in the U.S. With many of the big Canadian names now with U.S. listings, including, Aphria, Aurora, Cronos, CannTrust and Tilray, there is a much larger pool of investors there to support these stocks.

Another big development is the legalization of the non-psychoactive hemp and CBD in the U.S. The federal legalization of these markets has opened up a brand new marketplace for hemp and hemp-related products. According to a study by the Brightfield Group, the CBD industry in the U.S. alone could be worth USD $22 billion within the next two years, which puts that single market by itself at roughly the same target market size of the entire Canadian Marijuana industry. The number of opportunities to use CBD in pharmaceuticals, alternative health products and even food and beverage is a very large investment opportunity.

We’ve seen established Marijuana producers jump on the CBD/hemp opportunity. For example, Canopy Growth announced earlier this year that it will be investing USD $150 million in a hemp production facility in upstate New York, with an eye to potentially expand its investment up to USD $500 million in legal state-level producers in the U.S.2

An even bigger development is the Secure and Fair Enforcement Banking Act (SAFE Banking Act), which passed the bi-partisan House Financial Services Committee in a 45-15 vote during the last week of March. If passed, this legislation would allow for large federal banks to provide banking and potentially investment services to Marijuana companies that operate in legal state jurisdictions. A big advantage that Canadian LPs have had over U.S.-domiciled producers is their access to capital markets and direct lending and investment from large Canadian financial institutions. This is a key reason why the vast majority of market capitalization of the Marijuana industry is located in Canada. The Canadian capital markets provide strong liquidity and financing for companies.

The passage of the SAFE Banking Act could have far-reaching impact on the type of direct investment and amount of capital that would be available to U.S. producers. It will be interesting to watch Canadian LPs try to take advantage of the liberalizing U.S. marketplace and to see the possible ascension of some homegrown champions in that market.

1 Source: Ready to inhale: Democratic 2020 contenders embrace marijuana legalization, Reuters, March 6, 2019.

2 Source: Canopy Growth to invest up to $150 million in New York hemp facility, MarketWatch.com, January 14, 2019.

Rebalances

The strong performance in marijuana equity market resulted in significant additions to HMMJ’s portfolio for its quarterly rebalance.

HMMJ is the world’s first ETF offering direct exposure to North American-listed securities that are involved with marijuana bioengineering and production.

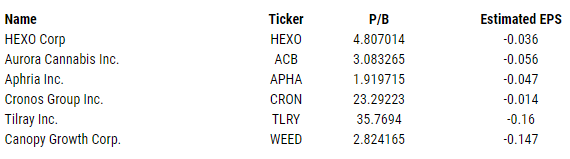

The HMMJ portfolio recently expanded to include the following constituents:

Click to enlarge

The most noticeable development from this rebalance was the inclusion of Charlotte’s Web Holdings, Inc. – a leading producer of legal CBD products in the United States, which is listed on the Canadian Securities Exchange (“CWEB:CSE”). U.S.-domiciled companies in the Marijuana equity sector that produce non-THC hemp and CBD are now eligible for inclusion in HMMJ’s portfolio. This comes after changes to a U.S. federal law at the end of 2018, which we highlighted above, legalizing the cultivation and distribution of non-THC hemp-based products.

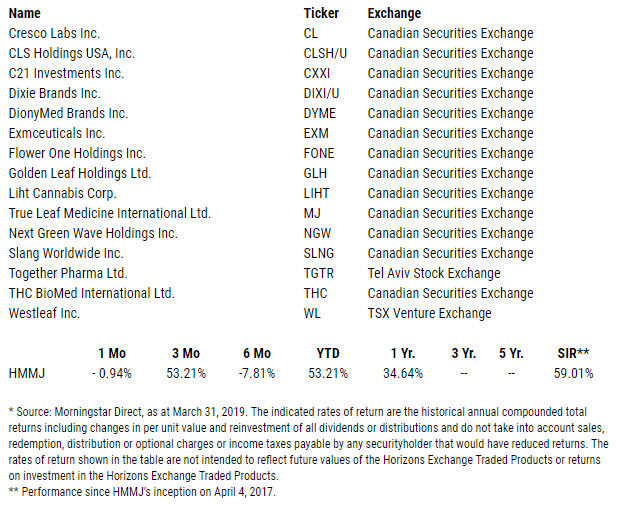

Horizons ETFs also completed the quarterly rebalance of the constituent holdings of the Horizons Emerging Marijuana Growers Index ETF (“HMJR:NEO”).

HMJR invests in small-market-capitalization companies with market capitalizations generally between CAD $50 million and CAD $500 million. The ETF’s portfolio is 100% invested in marijuana producers and distributors, and it can have exposure to companies outside of North America.

Globally, there has been increased legalization for medical marijuana in particular. This has expanded the universe of securities that HMJR can invest in, since the mandate is global in nature. Key markets that have fully legalized medical marijuana cultivation outside of Canada include Australia, Germany and Israel.

One of the most notable additions to HMJR’s portfolio this quarter was, Together Pharma Ltd., an Israeli-listed cultivator. Together Pharma is the first Israeli stock to be added to HMJR’s portfolio. As we see capital markets expansion in non-North American markets, we would expect more international stocks to be added to HMJR’s portfolio.

It’s also important to note, that because HMJR is listed on the Aequitas NEO Exchange it has the ability to invest in U.S.-domiciled names which are listed in Canada. Most of the new additions in the portfolio are CSE-listed names. We would anticipate that HMJR would participate in meaningful exposure to any growth in the U.S. producer market.

The HMJR portfolio recently expanded to include the following constituents:

Click to enlarge

This article is a special promotional feature produced by Horizons ETFs.