Canadian preferred shares have underperformed most asset classes this year, but opportunities still remain

Since the beginning of 2019, Canadian preferred shares have materially underperformed most asset classes. While this isn’t isolated to just Canadian preferred shares – the entire North American ETF preferred share market is down – weak performance amid broader equity market gains have some Canadian investors worried.

Amid the greater preferred shares market turmoil, Fiera Capital’s Integrated Fixed Income team, one of Canada’s largest preferred shares managers, and the sub-advisor of the Horizons Active Preferred Share ETF, the largest actively managed preferred share ETF in Canada, remains optimistic. Fiera believes that highly-rated issuers have been unfairly punished and sees the following opportunities in the sector:

1. The fiscal treatment for dividend income versus interest income is still “preferred”

In Canada, dividend income is taxed more favourably than interest income. For investors in the highest tax bracket, they can expect to pay 50% on interest income, compared to only 29% for dividend income. 1 This is possible through the dividend tax credit, which is only for Canadian stocks and is applicable for securities held in non-registered accounts. Preferred share income falls under this more preferable tax treatment.

2. Credit markets remain relatively healthy

According to Fiera Capital’s Integrated Fixed Income team, the global consensus for central bank stimulus will help support credit markets over the next six to twelve months. While there might be some volatility in the short term given geopolitical trade war tensions, Fiera Capital remains optimistic about the future.

3. Highly-rated issuers are likely trading at a discount

The Integrated Fixed Income team cites several examples of highly-rated issuers and their current preferred share offerings – insurance company Great-West Lifeco and energy producer Pembina Pipeline Corporation – a sample of the potentially attractive investment opportunities under the current lower interest rate environment.

[1] Source: TSI Network. Based on 2018 tax information. Horizons ETFs Management (Canada) Inc. (Horizons) makes no guarantee that the information above is current or accurate, although we have sourced this information from sources we believe to be reliable. Nothing herein constitutes tax or investment advice from Horizons and the information herein is general in nature only. Investors should review all information with their investment and tax advisors before making any investment decisions.

Additionally, given the low interest rate environment here at home and across the world, rate reset/floating rate preferred shares could be an attractive option if interest rates decrease further. If the Canada 5-year interest rate decreases to ~1.0% and stays there, approximately 80% of rate reset/floating rate preferred shares would reset with a higher coupon.

There’s also the possibility of a bottleneck developing: preferred share issuance from Canadian banks could be “somewhat limited”, going forward, given cheaper funding alternatives in the USD market. The Bank of Montreal and the Bank of Nova Scotia have already been active on this front. Given that development, Fiera Capital expects supply risk to be contained going forward.

While preferred share performance in 2019 has disappointed some investors, there may still be opportunity going forward. For investors looking for an alternative, pivoting to a fixed income ETF that holds investment grade corporate credit could provide some of the same advantages.

Have we bottomed on Preferred Shares?

The yield spread on preferred shares relative to the Canadian five-year has not been this low, since the last bottom of the asset class in 2016.

Some key reasons why it’s possible preferred shares could be close to near-term lows:

-

We are in a declining interest rate environment, which means that investors are invariably going to search for yield, this includes institutions and retail investors. The current yield spread on HPR vs. the five year GOC rate is near 4.00%. That is a relatively high yield spread and close to high yield spreads on quasi-investment grade credit.

-

Institutions might come back. Back in 2016, when we saw spreads on preferred shares hit this level it’s really signaled the bottom and we saw noticeable inflows. Once again, institutions and retail investors may look into preferred share ETFs.

Take a look at the table below, you can see we are very close to the spread levels from 2016, and look what happened to the NAV (which doesn’t include the dividend yield) from that point onwards. Spreads are near to their decade-wide highs. This chart also includes the iShares Canadian Corporate Bond Index ETF (XCB) as a comparison, showing the difference in spreads of preferred shares relative to the investment grade corporate bond market.

(Source: Bloomberg 2014/09/01 to 2019/08/27)

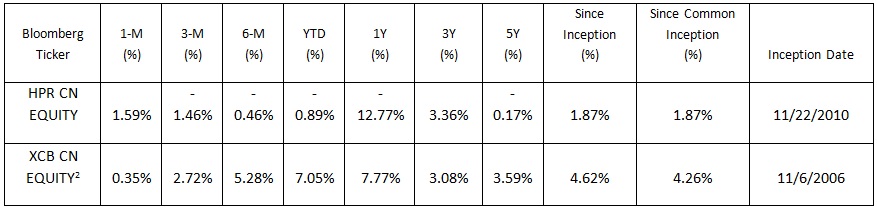

XCB vs. HPR Performance*:

(Source: Bloomberg, as at July 31, 2019)

*The indicated rates of return are the historical annual compounded total returns, including changes in unit value and reinvestment of all distributions and do not take into account sales, redemption, distribution or optional charges or income taxes payable by any securityholder that would have reduced returns. Additionally, index returns do not take into account management, operating or trading expenses that may be incurred in replicating the index. The rates of return above are not indicative of future returns. ETFs are not guaranteed, their values change frequently, and past performance may not be repeated. The index is (indices are) not directly investible.

Fiera has positioned HPR’s portfolio to take advantage of the spread conditions on rate-reset preferred shares. Fiera believes that reset/floating rate preferred shares from highly-rated issuers that are trading at discount with a reset spread between ~275 bps and ~400 bps offer attractive yield compensation while providing protection under a lower interest rate environment.

[2] XCB Investment Strategy: Seeks to provide income by replicating the performance of the FTSE Canada All Corporate Bond Index™, net of expenses. (https://www.blackrock.com/ca/individual/en/products/239485/ishares-canadian-corporate-bond-index-etf)

Regardless of declining interest rates, Canadian preferred shares now provide an attractive source of yield that even in worst-case declining interest rate scenarios provide a yield much higher than most investment grade corporate bond strategies. How long before investors start to come back in to take advantage of this environment?

*The indicated rates of return are the historical annual compounded total returns including changes in per unit value and reinvestment of all dividends or distributions and do not take into account sales, redemption, distribution or optional charges or income taxes payable by any securityholder that would have reduced returns. The rates of return shown in the table are not intended to reflect future values of the Horizons Exchange Traded Products or returns on investment in the Horizons Exchange Traded Products.

Certain statements may constitute a forward-looking statement, including those identified by the expression “expect” and similar expressions (including grammatical variations thereof). The forward-looking statements are not historical facts but reflect the author’s current expectations regarding future results or events. These forward-looking statements are subject to a number of risks and uncertainties that could cause actual results or events to differ materially from current expectations. These and other factors should be considered carefully and readers should not place undue reliance on such forward looking statements. These forward-looking statements are made as of the date hereof and the authors do not undertake to update any forward-looking statement

that is contained herein, whether as a result of new information, future events or otherwise, unless required by applicable law.