It’s time to reframe how we talk about retirement, NIA report suggests

Talk of retirement frequently centres on building up enough savings to provide an adequate income in post-work years. But is there a better way?

While financial advisors and their clients will inevitably discuss retirement income and prepare for the decumulation phase as it approaches, a new report calls for a reframing our retirement mindset, starting with a shift away from an approach used in Canada and most of the world.

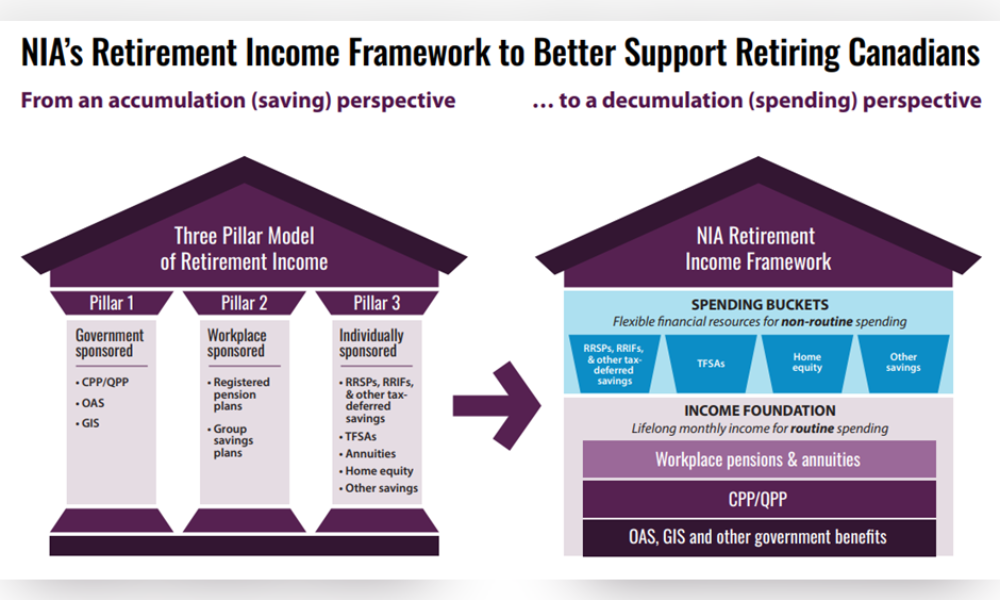

The National Institute on Ageing says that using the standard ‘three pillar’ visualization, which in Canada includes government-sponsored programs such as Old Age Security, the Guaranteed Income Supplement and the Canada Pension Plan/Quebec Pension Plan, along with workplace pension plans and personal savings (with equivalents used in other countries), is missing the chance to better prepare people for retirement.

“The most important question workers planning for retirement want to know is how will this system pay for my lifestyle for the rest of my life?” says report lead author Dr. Bonnie-Jeanne MacDonald, director of Financial Security Research for the NIA. “Without better support, research shows retirees will not make the decisions that protect them long after they retire — including when to start CPP/QPP benefits. With baby boomers retiring in droves, our system urgently needs to help them when making these once-in-a-lifetime, high stakes decisions.”

The report, (Re) Introducing the Retirement Income System: A New Framework Tailored to the Retiree’s Perspective, was written by MacDonald along with Doug Chandler and Alyssa Hodder, Associate Fellows for the NIA, and is the first of an eight-part paper series proposing how the retirement income system could be better communicated to Canadians.

Reframing retirement income

Chandler says that the three pillar visualization is seen from the perspective of those who provide the income sources, rather than retirees.

“It’s about where the money came from, not where it’s going. The traditional three pillar visual is used around the world, and yet nobody has pointed out this disconnect before. That’s a problem,” he said.

The report says that the current system is not conducive to helping those planning their retirement on how their income sources will work in providing a lifelong income and a better way is to help nudge them into a mindset shift from accumulation to decumulation.

Considering, for example, delaying benefits through working longer or using personal savings, could make a substantial difference to long-term retirement income. However, most Canadians choose to start receiving their CPP/QPP benefits when they are 65.

The authors highlight how using a new system, the NIA Retirement Income Framework, focus on retirement income can help retirees (and future retirees) realize how the three-pillar sources are best used for everyday expenses with non-routine expenses covered by investments.

“The ‘a-ha’ moment was realizing that lifelong monthly pension income is not a pillar of our retirement income system from the perspective of older Canadians — for them, it is the foundation and their other economic resources rest on it.” added MacDonald.

“Financial advisors, employers, federal and provincial governments, professional organizations, financial institutions and other agencies can all benefit from supporting a more productive framing of our retirement income system,” explained Hodder. “When it comes to communicating complex financial topics, a good picture isn’t just worth a thousand words; it can mean thousands of badly needed dollars for a vulnerable older adult.”